PNC Bank 2014 Annual Report Download - page 237

Download and view the complete annual report

Please find page 237 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

Table 158: Parent Company – Statement of Cash Flows

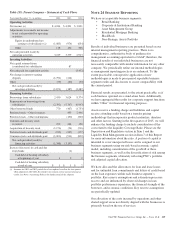

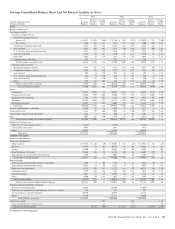

Year ended December 31 – in millions 2014 2013 2012

Operating Activities

Net income (a) $ 4,184 $ 4,201 $ 3,001

Adjustments to reconcile net income

to net cash provided by operating

activities:

Equity in undistributed net

earnings of subsidiaries (a) (1,083) (974) (654)

Other 118 152 566

Net cash provided (used) by

operating activities 3,219 3,379 2,913

Investing Activities

Net capital returned from

(contributed to) subsidiaries 87

Net cash paid for acquisition activity (3,432)

Net change in interest-earning

deposits (1,792) (214)

Other (79) (60) (50)

Net cash provided (used) by

investing activities (1,871) (187) (3,482)

Financing Activities

Borrowings from subsidiaries 2,430 3,624 8,374

Repayments on borrowings from

subsidiaries (2,392) (5,767) (6,943)

Other borrowed funds 770 (467) (1,753)

Preferred stock – Other issuances 495 2,446

Preferred stock – Other redemptions (150) (500)

Common and treasury stock

issuances 252 244 158

Acquisition of treasury stock (1,176) (24) (216)

Preferred stock cash dividends paid (232) (237) (177)

Common stock cash dividends paid (1,000) (911) (820)

Net cash provided (used) by

financing activities (1,348) (3,193) 569

Increase (decrease) in cash and due

from banks (1)

Cash held at banking subsidiary

at beginning of year 122

Cash held at banking subsidiary

at end of year $1$1$2

(a) Amounts for 2013 and 2012 periods have been updated to reflect the first quarter

2014 adoption of ASU 2014-01 related to investments in low income housing tax

credits. See Note 1 Accounting Policies for further detail of the adoption.

N

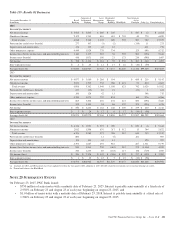

OTE

24 S

EGMENT

R

EPORTING

We have six reportable business segments:

• Retail Banking

• Corporate & Institutional Banking

• Asset Management Group

• Residential Mortgage Banking

• BlackRock

• Non-Strategic Assets Portfolio

Results of individual businesses are presented based on our

internal management reporting practices. There is no

comprehensive, authoritative body of guidance for

management accounting equivalent to GAAP; therefore, the

financial results of our individual businesses are not

necessarily comparable with similar information for any other

company. We periodically refine our internal methodologies

as management reporting practices are enhanced. To the

extent practicable, retrospective application of new

methodologies is made to prior period reportable business

segment results and disclosures to create comparability with

the current period.

Financial results are presented, to the extent practicable, as if

each business operated on a stand-alone basis. Additionally,

we have aggregated the results for corporate support functions

within “Other” for financial reporting purposes.

Assets receive a funding charge and liabilities and capital

receive a funding credit based on a transfer pricing

methodology that incorporates product maturities, duration

and other factors. Starting in the first quarter of 2015, we will

enhance the funding charge to include consideration of the

cost related to the Liquidity Coverage Ratio. Please see the

Supervision and Regulation section in Item 1 and the

Liquidity Risk Management section in Item 7 of this Report

for more information about the ratio. A portion of capital is

intended to cover unexpected losses and is assigned to our

business segments using our risk-based economic capital

model, including consideration of the goodwill at those

business segments, as well as the diversification of risk among

the business segments, ultimately reflecting PNC’s portfolio

risk adjusted capital allocation.

We have allocated the allowances for loan and lease losses

and for unfunded loan commitments and letters of credit based

on the loan exposures within each business segment’s

portfolio. Key reserve assumptions and estimation processes

react to and are influenced by observed changes in loan

portfolio performance experience, the financial strength of the

borrower, and economic conditions. Key reserve assumptions

are periodically updated.

Our allocation of the costs incurred by operations and other

shared support areas not directly aligned with the businesses is

primarily based on the use of services.

The PNC Financial Services Group, Inc. – Form 10-K 219