PNC Bank 2014 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

represented 60% of the loan portfolio at December 31, 2013

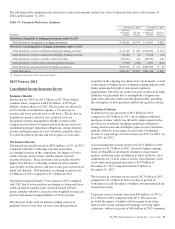

and 59% at December 31, 2012. Consumer lending

represented 40% of the loan portfolio at December 31, 2013

and 41% at December 31, 2012. Commercial real estate loans

represented 11% of total loans at December 31, 2013 and 10%

at December 31, 2012 and represented 7% of total assets at

December 31, 2013 and 6% at December 31, 2012.

The total loan balances above included purchased impaired loans

of $6.1 billion, or 3% of total loans, at December 31, 2013, and

$7.4 billion, or 4% of total loans, at December 31, 2012.

Investment Securities

As of December 31, 2013, the amortized cost and fair value of

available for sale securities totaled $48.0 billion and $48.6

billion, respectively, compared to an amortized cost and fair

value as of December 31, 2012 of $49.4 billion and $51.1

billion, respectively. The amortized cost and fair value of held

to maturity securities were $11.7 billion and $11.8 billion,

respectively, at December 31, 2013, compared to $10.4 billion

and $10.9 billion, respectively, at December 31, 2012.

Investment securities represented 19% of total assets at

December 31, 2013 and 20% at December 31, 2012. Average

investment securities decreased to $57.3 billion during 2013

compared to $60.8 billion during 2012.

The fair value of investment securities is impacted by interest

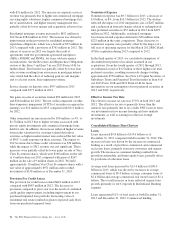

rates, credit spreads, market volatility and liquidity conditions.

The fair value of investment securities generally decreases

when interest rates increase and vice versa. In addition, the

fair value generally decreases when credit spreads widen and

vice versa. Net unrealized gains in the total investment

securities portfolio decreased to $.7 billion at December 31,

2013 from $2.1 billion at December 31, 2012 due primarily to

an increase in market interest rates. The comparable amounts

for the securities available for sale portfolio were $.6 billion

and $1.6 billion, respectively.

During 2013, we transferred securities with a fair value of

$1.9 billion from available for sale to held to maturity. We

changed our intent and committed to hold these high-quality

securities to maturity in order to reduce the impact of price

volatility on Accumulated other comprehensive income and

certain capital measures, taking into consideration market

conditions and changes to regulatory capital requirements

under Basel III capital standards.

The weighted-average expected maturity of the investment

securities portfolio (excluding corporate stocks and other) was

4.9 years at December 31, 2013 and 4.0 years at December 31,

2012.

Loans Held For Sale

Loans held for sale totaled $2.3 billion at December 31, 2013

compared with $3.7 billion at December 31, 2012.

For commercial mortgages held for sale designated at fair

value, the balance relating to these loans was $586 million at

December 31, 2013 compared to $772 million at

December 31, 2012. For commercial mortgages held for sale

carried at lower of cost or fair value, we sold $2.8 billion in

2013 compared to $2.2 billion in 2012. All of these loan sales

were to government agencies. Total gains of $79 million were

recognized on the valuation and sale of commercial mortgage

loans held for sale, net of hedges, in 2013, and $41 million in

2012.

Residential mortgage loan origination volume was $15.1

billion in 2013 compared to $15.2 billion in 2012.

Substantially all such loans were originated under agency or

Federal Housing Administration (FHA) standards. We sold

$14.7 billion of loans and recognized related gains of $568

million in 2013. The comparable amounts for 2012 were $13.8

billion and $747 million, respectively.

Asset Quality

Overall credit quality continued to improve during 2013.

Nonperforming assets decreased $.3 billion, or 9%, to $3.5

billion at December 31, 2013 compared to December 31,

2012. Nonperforming assets to total assets were 1.08% at

December 31, 2013, compared to 1.24% at December 31,

2012. Overall delinquencies of $2.5 billion decreased $1.3

billion, or 33%, compared with December 31, 2012. Net

charge-offs of $1.1 billion in 2013 were down 16% compared

to net charge-offs of $1.3 billion in 2012. Net charge-offs

were 0.57% of average loans in 2013 and 0.73% of average

loans in 2012.

The ALLL was $3.6 billion, or 1.84% of total loans and 117%

of nonperforming loans, as of December 31, 2013, compared

to $4.0 billion, or 2.17% of total loans and 124% of

nonperforming loans, as of December 31, 2012.

At December 31, 2013, our largest nonperforming asset was

$36 million in the Real Estate, Rental and Leasing Industry

and our average nonperforming loans associated with

commercial lending were under $1 million.

Goodwill and Other Intangible Assets

Goodwill and other intangible assets totaled $11.3 billion at

December 31, 2013 and $10.9 billion at December 31, 2012.

The increase of $.4 billion was primarily due to additions to

and changes in value of mortgage and other loan servicing

rights.

The PNC Financial Services Group, Inc. – Form 10-K 97