PNC Bank 2014 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

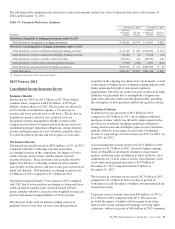

with $31 million for 2012. The increase in corporate services

revenue was primarily due to higher net commercial mortgage

servicing rights valuations, higher commercial mortgage fees,

net of amortization, and higher treasury management fees,

partially offset by lower merger and acquisition advisory fees.

Residential mortgage revenue increased to $871 million in

2013 from $284 million in 2012. The increase was driven by

improvement in the provision for residential mortgage

repurchase obligations, which was a benefit of $53 million in

2013 compared with a provision of $761 million in 2012. The

release of reserves in 2013 was largely the result of

agreements with two government-sponsored enterprises

(GSEs), FHLMC and FNMA, for loans sold into agency

securitizations. See the Recourse And Repurchase Obligations

section of this Item 7 and Item 7 in our 2013 Form 10-K for

further detail. This benefit was partially offset by lower loan

sales revenue resulting from an increase in mortgage interest

rates which had the effect of reducing gain on sale margins

and, to a lesser extent, loan origination volume.

Service charges on deposits were $597 million in 2013

compared with $573 million in 2012.

Net gains on sales of securities totaled $99 million for 2013

and $204 million for 2012. The net credit component of other-

than-temporary impairment (OTTI) of securities recognized in

earnings was $16 million in 2013 compared with $111 million

for 2012.

Other noninterest income increased by $58 million, or 4%, to

$1.5 billion in 2013 due to higher revenue associated with

private equity investments and commercial mortgage loans

held for sale. In addition, the increase reflected higher revenue

from credit valuations for customer-related derivatives

activities as higher market interest rates reduced the fair value

of PNC’s credit exposure on these activities. The impact to

2013 revenue due to these credit valuations was $56 million,

while the impact to 2012 revenue was not significant. These

increases were partially offset by lower gains on sale of Visa

Class B common shares, which were $168 million on the sale

of 4 million shares in 2013 compared with gains of $267

million on the sale of 9 million shares in 2012. We held

approximately 10 million Visa Class B common shares with a

fair value of approximately $971 million and recorded

investment of $158 million as of December 31, 2013.

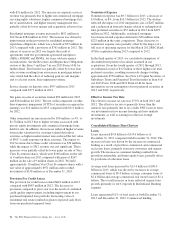

Provision For Credit Losses

The provision for credit losses totaled $643 million in 2013

compared with $987 million in 2012. The decrease in

provision compared to prior year was the result of continued

credit quality improvement, including improvement in our

purchased impaired loan portfolio. Increasing value of

residential real estate resulted in greater expected cash flows

from our purchased impaired loans.

Noninterest Expense

Noninterest expense was $9.7 billion for 2013, a decrease of

$.8 billion, or 8%, from $10.5 billion for 2012. The decline

reflected the impact of 2012 integration costs of $267 million

and a reduction in noncash charges related to redemption of

trust preferred securities to $57 million in 2013 from $295

million in 2012. Additionally, residential mortgage

foreclosure-related expenses declined to $56 million from

$225 million in the same comparison. These decreases to

noninterest expense were partially offset by the impact of a

full year of operating expense for the March 2012 RBC Bank

(USA) acquisition during 2013 compared to 2012.

In the third quarter of 2013, we concluded redemptions of

discounted trust preferred securities assumed in our

acquisitions. From the fourth quarter of 2011 through 2013,

we redeemed a total of $3.2 billion of these higher-rate trust

preferred securities, resulting in noncash charges totaling

approximately $550 million. See Note 14 Capital Securities of

Subsidiary Trusts and Perpetual Trust Securities in Item 8 of

our 2013 Form 10-K and 2012 Form 10-K for more

information on our redemption of trust preferred securities in

2013 and 2012, respectively.

Effective Income Tax Rate

The effective income tax rate was 25.9% in both 2013 and

2012. The effective tax rate is generally lower than the

statutory rate primarily due to tax credits PNC receives from

our investments in low income housing and new markets

investments, as well as earnings in other tax exempt

investments.

Consolidated Balance Sheet Review

Loans

Loans increased $9.8 billion to $195.6 billion as of

December 31, 2013 compared with December 31, 2012. The

increase in loans was driven by the increase in commercial

lending as a result of growth in commercial and commercial

real estate loans, primarily from new customers and organic

growth. The increase in consumer lending resulted from

growth in automobile and home equity loans, partially offset

by paydowns of education loans.

Average total loans increased by $13.4 billion to $190.0

billion in 2013, which was driven by increases in average

commercial loans of $9.4 billion, average consumer loans of

$2.4 billion and average commercial real estate loans of $1.4

billion. The overall increase in loans reflected organic loan

growth, primarily in our Corporate & Institutional Banking

segment.

Loans represented 61% of total assets at both December 31,

2013 and December 31, 2012. Commercial lending

96 The PNC Financial Services Group, Inc. – Form 10-K