PNC Bank 2014 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

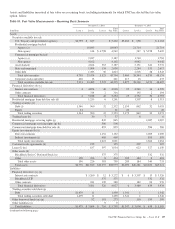

|

|

for these securities is primarily estimated using pricing

obtained from third-party vendors. In some cases, fair value is

estimated using a dealer quote, by reference to prices of

securities of a similar vintage and collateral type or by

reference to recent sales of similar securities. Market activity

for these security types is limited with little price

transparency. As a result, these securities are generally valued

by the third-party vendor using a discounted cash flow

approach that incorporates observable market activity where

available. Significant inputs to the valuation include

prepayment projections and credit loss assumptions (default

rate and loss severity) and discount rates that are deemed

representative of current market conditions. The discount rates

used incorporate a spread over the benchmark curve that takes

into consideration liquidity risk and potential credit risk not

already included in the credit loss assumptions. Significant

increases (decreases) in any of those assumptions in isolation

would result in a significantly lower (higher) fair value

measurement. Prepayment estimates generally increase when

market interest rates decline and decrease when market

interest rates rise. Credit loss estimates are driven by the

ability of borrowers to pay their loans and housing market

prices and are impacted by changes in overall macroeconomic

conditions, typically increasing when economic conditions

worsen and decreasing when conditions improve. An increase

in the estimated prepayment rate typically results in a decrease

in estimated credit losses and vice versa. Discount rates

typically increase when market interest rates increase and/or

credit and liquidity risks increase. Similarly, discount rates

typically decrease when market interest rates decline and/or

credit and liquidity conditions improve. Price validation

procedures performed for these securities include comparing

current prices to historical pricing trends by collateral type and

vintage, and by obtaining corroborating prices from another

third-party source.

Certain infrequently traded debt securities within the State and

municipal and Other debt securities available-for-sale and

Trading securities categories are also classified in Level 3.

The significant unobservable inputs used to estimate the fair

value of these securities include an estimate of expected credit

losses and a discount for liquidity risk. These inputs are

incorporated into the fair value measurement by either

increasing the spread over the benchmark curve or by

applying a credit and liquidity discount to the par value of the

security. Significant increases (decreases) in credit and/or

liquidity risk could result in a significantly lower (higher) fair

value estimate.

Financial Derivatives

Exchange-traded derivatives are valued using quoted market

prices and are classified as Level 1. However, the majority of

derivatives that we enter into are executed over-the-counter

and are valued using internal models. These derivatives are

primarily classified as Level 2 as the readily observable

market inputs to these models are validated to external

sources. The external sources for these inputs include industry

pricing services, or are corroborated through recent trades,

dealer quotes, yield curves, implied volatility or other market-

related data. Level 2 financial derivatives are primarily

estimated using a combination of Eurodollar future prices and

observable benchmark interest rate swaps to construct

projected discounted cash flows. Financial derivatives that are

priced using significant management judgment or assumptions

are classified as Level 3.

Fair value information for Level 3 financial derivatives is

presented separately for interest rate contracts and other

contracts. Interest rate contracts include residential and

commercial mortgage interest rate lock commitments and

certain interest rate options. Other contracts include risk

participation agreements, swaps related to the sale of certain

Visa Class B common shares and other types of contracts.

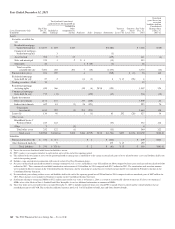

The fair values of residential mortgage loan commitment

assets as of December 31, 2014 and 2013 are included in the

Insignificant Level 3 assets, net of liabilities line item in Table

85 in this Note 7. Significant unobservable inputs for these

commitments include the probability of funding and

embedded servicing. The probability of funding for residential

mortgage loan commitments represents the expected

proportion of loan commitments in the pipeline that will fund.

Additionally, embedded in the market price of the underlying

loan is a value for retaining servicing of the loan once it is

sold. Significant increases (decreases) in the fair value of a

residential mortgage loan commitment asset (liability) result

when the probability of funding increases (decreases) and

when the embedded servicing value increases (decreases).

The fair values of commercial mortgage loan commitment

assets and liabilities as of December 31, 2014 and 2013 are

included in the Insignificant Level 3 assets, net of liabilities

line item in Table 85 in this Note 7. Significant unobservable

inputs for these commitments include spread over the

benchmark interest rate and the estimated servicing cash flows

for loans sold to the agencies with servicing retained. The

spread over the benchmark curve reflects management

assumptions regarding credit and liquidity risks. Significant

increases (decreases) in the fair value of commercial mortgage

loan commitments result when the spread over the benchmark

curve decreases (increases) or the estimated servicing cash

flows for loans sold to the agencies with servicing retained

increases (decreases).

The fair values of interest rate option assets and liabilities as

of December 31, 2014 and 2013 are included in the

Insignificant Level 3 assets, net of liabilities line item in Table

85 in this Note 7. The significant unobservable input used in

the fair value measurement of the interest rate options is

expected interest rate volatility. Significant increases

(decreases) in interest rate volatility would result in a

significantly higher (lower) fair value measurement.

The PNC Financial Services Group, Inc. – Form 10-K 153