PNC Bank 2014 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

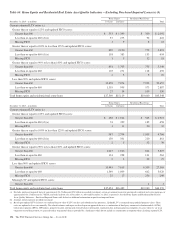

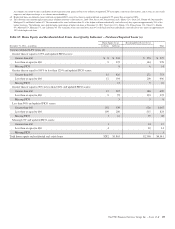

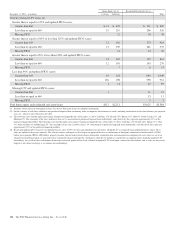

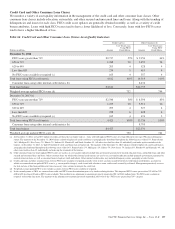

Nonperforming loans also include certain loans whose terms

have been restructured in a manner that grants a concession to

a borrower experiencing financial difficulties. In accordance

with applicable accounting guidance, these loans are

considered TDRs. See Note 1 Accounting Policies and the

TDR section of this Note 3 for additional information. For the

twelve months ended December 31, 2014, $1.2 billion of

Consumer loans held for sale, loans accounted for under the

fair value option, pooled purchased impaired loans, as well as

certain government insured or guaranteed loans which were

evaluated for TDR consideration, are not classified as TDRs.

The comparable amount for the twelve months ended

December 31, 2013 was $2.3 billion.

Total nonperforming loans in the nonperforming assets table

above include TDRs of $1.4 billion at December 31, 2014 and

$1.5 billion at December 31, 2013. TDRs that are performing,

including all credit card TDR loans, totaled $1.2 billion at

December 31, 2014 and December 31, 2013, respectively, and

are excluded from nonperforming loans. These performing

TDR loans, excluding credit cards which are not placed on

nonaccrual status as permitted by regulatory guidance, have

demonstrated a period of at least six months of consecutive

performance under the restructured terms. Loans where

borrowers have been discharged from personal liability

through Chapter 7 bankruptcy and have not formally

reaffirmed their loan obligations to PNC and loans to

borrowers not currently obligated to make both principal and

interest payments under the restructured terms are not returned

to accrual status.

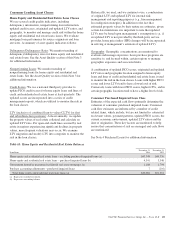

Additional Asset Quality Indicators

We have two overall portfolio segments – Commercial

Lending and Consumer Lending. Each of these two segments

is comprised of multiple loan classes. Classes are

characterized by similarities in initial measurement, risk

attributes and the manner in which we monitor and assess

credit risk. The Commercial Lending segment is comprised of

the commercial, commercial real estate, equipment lease

financing, and commercial purchased impaired loan classes.

The Consumer Lending segment is comprised of the home

equity, residential real estate, credit card, other consumer, and

consumer purchased impaired loan classes. Asset quality

indicators for each of these loan classes are discussed in more

detail below.

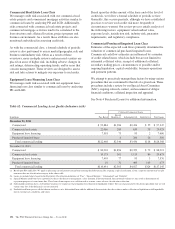

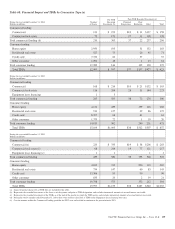

Commercial Lending Asset Classes

Commercial Loan Class

For commercial loans, we monitor the performance of the

borrower in a disciplined and regular manner based upon the

level of credit risk inherent in the loan. To evaluate the level

of credit risk, we assign an internal risk rating reflecting the

borrower’s PD and LGD. This two-dimensional credit risk

rating methodology provides granularity in the risk monitoring

process on an ongoing basis. These ratings are reviewed and

updated on a risk-adjusted basis, generally at least once per

year. Additionally, no less frequently than on an annual basis,

we review PD rates related to each rating grade based upon

internal historical data. These rates are updated as needed and

augmented by market data as deemed necessary. For small

balance homogenous pools of commercial loans, mortgages

and leases, we apply statistical modeling to assist in

determining the probability of default within these pools.

Further, on a periodic basis, we update our LGD estimates

associated with each rating grade based upon historical data.

The combination of the PD and LGD ratings assigned to a

commercial loan, capturing both the combination of

expectations of default and loss severity in event of default,

reflects the relative estimated likelihood of loss for that loan at

the reporting date. In general, loans with better PD and LGD

tend to have a lower likelihood of loss compared to loans with

worse PD and LGD. The loss amount also considers exposure

at date of default, which we also periodically update based

upon historical data.

Based upon the amount of the lending arrangement and our

risk rating assessment, we follow a formal schedule of written

periodic review. Quarterly, we conduct formal reviews of a

market’s or business unit’s entire loan portfolio, focusing on

those loans which we perceive to be of higher risk, based upon

PDs and LGDs, or loans for which credit quality is weakening.

If circumstances warrant, it is our practice to review any

customer obligation and its level of credit risk more

frequently. We attempt to proactively manage our loans by

using various procedures that are customized to the risk of a

given loan, including ongoing outreach, contact, and

assessment of obligor financial conditions, collateral

inspection and appraisal.

The PNC Financial Services Group, Inc. – Form 10-K 131