PNC Bank 2014 Annual Report Download - page 183

Download and view the complete annual report

Please find page 183 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

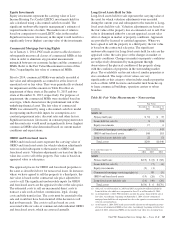

Equity Investments

Equity investments represent the carrying value of Low

Income Housing Tax Credit (LIHTC) investments held for

sale calculated using a discounted cash flow model. The

significant unobservable input is management’s estimate of

required market rate of return. The market rate of return is

based on comparison to recent LIHTC sales in the market.

Significant increases (decreases) in this input would result in a

significantly lower (higher) carrying value of the investments.

Commercial Mortgage Servicing Rights

As of January 1, 2014, PNC made an irrevocable election to

subsequently measure all classes of commercial MSRs at fair

value in order to eliminate any potential measurement

mismatch between our economic hedges and the commercial

MSRs. Refer to the Fair Value Measurement section of this

Note 7 regarding the fair value of commercial MSRs.

Prior to 2014, commercial MSRs were initially recorded at

fair value and subsequently accounted for at the lower of

amortized cost or fair value. They were periodically evaluated

for impairment and the amounts in Table 86 reflect an

impairment of three strata at December 31, 2013 and two

strata at December 31, 2012, respectively. For purposes of

impairment, the commercial MSRs were stratified based on

asset type, which characterizes the predominant risk of the

underlying financial asset. The fair value of commercial

MSRs was estimated by using a discounted cash flow model

incorporating unobservable inputs for assumptions as to

constant prepayment rates, discount rates and other factors.

Significant increases (decreases) in constant prepayment rates

and discount rates would result in significantly lower (higher)

commercial MSR value determined based on current market

conditions and expectations.

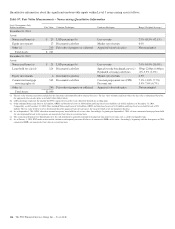

OREO and Foreclosed Assets

OREO and foreclosed assets represent the carrying value of

OREO and foreclosed assets for which valuation adjustments

were recorded subsequent to the transfer to OREO and

foreclosed assets. Valuation adjustments are based on the fair

value less cost to sell of the property. Fair value is based on

appraised value or sales price.

The appraisal process for OREO and foreclosed properties is

the same as described above for nonaccrual loans. In instances

where we have agreed to sell the property to a third party, the

fair value is based on the contractual sale price adjusted for

costs to sell. The significant unobservable inputs for OREO

and foreclosed assets are the appraised value or the sales price.

The estimated costs to sell are incremental direct costs to

transact a sale such as broker commissions, legal, closing

costs and title transfer fees. The costs must be essential to the

sale and would not have been incurred if the decision to sell

had not been made. The costs to sell are based on costs

associated with our sales of commercial and residential OREO

and foreclosed assets, which are assessed annually.

Long-Lived Assets Held for Sale

Long-lived assets held for sale represent the carrying value of

the asset for which valuation adjustments were recorded

during the current year and subsequent to the transfer to Long-

lived assets held for sale. Valuation adjustments are based on

the fair value of the property less an estimated cost to sell. Fair

value is determined either by a recent appraisal, recent sales

offer or changes in market or property conditions. Appraisals

are provided by licensed or certified appraisers. Where we

have agreed to sell the property to a third party, the fair value

is based on the contractual sale price. The significant

unobservable inputs for Long-lived assets held for sale are the

appraised value, the sales price or the changes in market or

property conditions. Changes in market or property conditions

are subjectively determined by management through

observation of the physical condition of the property along

with the condition of properties in the surrounding market

place. The availability and recent sales of similar properties is

also considered. The range of fair values can vary

significantly as this category often includes smaller properties

such as offsite ATM locations and smaller rural branches up

to large commercial buildings, operation centers or urban

branches.

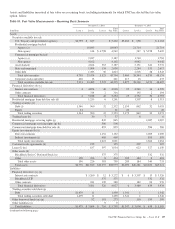

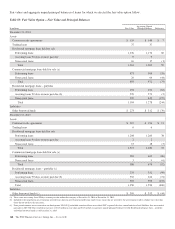

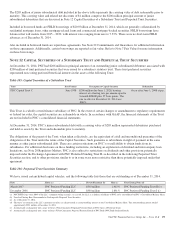

Table 86: Fair Value Measurements – Nonrecurring

Fair Value

In millions

December 31

2014

December 31

2013

Assets (a)

Nonaccrual loans $ 54 $ 35

Loans held for sale (b) 8 224

Equity investments 17 6

Commercial mortgage servicing rights (c) 543

OREO and foreclosed assets 168 181

Long-lived assets held for sale 22 51

Total assets $269 $1,040

Year ended December 31

In millions

Gains (Losses)

2014 2013 2012

Assets

Nonaccrual loans $(19) $ (8) $ (68)

Loans held for sale (b) (7) (4)

Equity investments (2) (1)

Commercial mortgage servicing rights (c) 88 (5)

OREO and foreclosed assets (19) (26) (73)

Long-lived assets held for sale (14) (40) (20)

Total assets $(54) $ 6 $(170)

(a) All Level 3 as of December 31, 2014 and 2013 except for $8 million included in

Loans held for sale which was categorized as Level 2 as of December 31, 2014.

(b) As of September 1, 2014, PNC elected to account for agency loans held for sale at

fair value. Accordingly, beginning on September 1, 2014, all new commercial

mortgage loans held for sale originated for sale to the agencies are measured at fair

value on a recurring basis.

(c) As of January 1, 2014, PNC made an irrevocable election to subsequently measure

all classes of commercial MSRs at fair value. Accordingly, beginning with the first

quarter of 2014, commercial MSRs are measured at fair value on a recurring basis.

The PNC Financial Services Group, Inc. – Form 10-K 165