Wells Fargo 2011 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

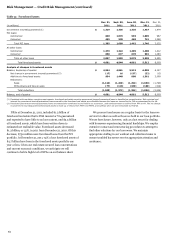

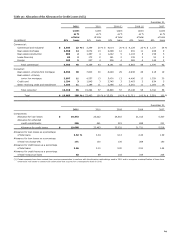

Risk Management — Credit Risk Management (continued)

Table 38: Changes in Mortgage Repurchase Liability

Quarter ended

Dec. 31,

Sept. 30,

June 30,

Mar. 31,

Year ended Dec. 31,

(in millions)

2011

2011

2011

2011

2011

2010

Balance, beginning of period

$

1,194

1,188

1,207

1,289

1,289

1,033

Provision for repurchase losses:

Loan sales

27

19

20

35

101

144

Change in estimate (1)

377

371

222

214

1,184

1,474

Total additions

404

390

242

249

1,285

1,618

Losses

(272)

(384)

(261)

(331)

(1,248)

(1,362)

Balance, end of period

$

1,326

1,194

1,188

1,207

1,326

1,289

(1)

Results from such factors as credit deterioration, changes in investor demand and mortgage insurer practices, and changes in the financial stability of correspondent lenders.

The mortgage repurchase liability of $1.3 billion at

December 31, 2011, represents our best estimate of the probable

loss that we may incur for various representations and

warranties in the contractual provisions of our sales of mortgage

loans. Because the level of mortgage loan repurchase losses

depends upon economic factors, investor demand strategies and

other external conditions that may change over the life of the

underlying loans, the level of the liability for mortgage loan

repurchase losses is difficult to estimate and requires

considerable management judgment. We maintain regular

contact with the GSEs and other significant investors to monitor

and address their repurchase demand practices and concerns.

Because of the uncertainty in the various estimates underlying

the mortgage repurchase liability, there is a range of losses in

excess of the recorded mortgage repurchase liability that are

reasonably possible. The estimate of the range of possible loss

for representations and warranties does not represent a probable

loss, and is based on currently available information, significant

judgment, and a number of assumptions that are subject to

change. The high end of this range of reasonably possible losses

in excess of our recorded liability was $2.1 billion at

December 31, 2011, and was determined based upon modifying

the assumptions utilized in our best estimate of probable loss to

reflect what we believe to be the high end of reasonably possible

adverse assumptions. For additional information on our

repurchase liability, see the “Critical Accounting Policies –

Liability for Mortgage Loan Repurchase Losses” section and

Note 9 (Mortgage Banking Activities) to Financial Statements in

this Report.

The repurchase liability is predominantly applicable to loans

we originated and sold with representations and warranties.

Most of these loans are included in our servicing portfolio. Our

repurchase liability estimate involves consideration of many

factors that influence the key assumptions of what our

repurchase volume may be and what loss on average we may

incur. Those key assumptions and the sensitivity of the liability

to immediate adverse changes in them at December 31, 2011, are

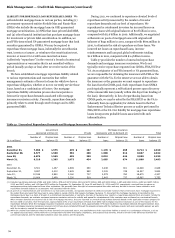

presented in Table 39. For additional information about the

range of loss that is reasonably possible in excess of the recorded

mortgage repurchase liability, see Note 9 (Mortgage Banking

Activities) to Financial Statements in this Report.

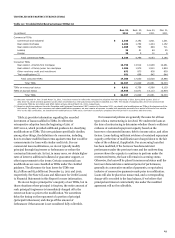

Table

39: Mortgage Repurchase Liability –

Sensitivity/Assumptions

Mortgage

repurchase

(in millions)

liability

Balance at December 31, 2011

$

1,326

Loss on repurchases (1)

40.0

%

Increase in liability from:

10% higher losses

$

133

25% higher losses

333

Repurchase rate assumption

0.3

%

Increase in liability from:

10% higher repurchase rates

$

122

25% higher repurchase rates

304

(1)

Represents total estimated average loss rate on repurchased loans, net of

recovery from third party originators, based on historical experience and

current economic conditions.

The average loss rate includes the impact of

repurchased loans for which no loss is expected to be realized.

To the extent that economic conditions and the housing

market do not improve or future investor repurchase demands

and appeals success rates differ from past experience, we could

continue to have increased demands and increased loss severity

on repurchases, causing future additions to the repurchase

liability. However, some of the underwriting standards that were

permitted by the GSEs for conforming loans in the 2006 through

2008 vintages, which significantly contributed to recent levels of

repurchase demands, were tightened starting in mid to late

2008. Accordingly, we do not expect a similar rate of repurchase

requests from the 2009 and prospective vintages, absent

deterioration in economic conditions or changes in investor

behavior.

In October 2011, the Arizona Department of Insurance

assumed full and exclusive power of management and control of

PMI Mortgage Insurance Co. (PMI) and announced that PMI

will pay 50% of claim amounts in cash, with the rest deferred. In

November 2011, PMI’s parent company, PMI Group Inc., filed

for Chapter 11 bankruptcy. Wells Fargo has previously utilized

PMI to provide mortgage insurance on certain loans originated

and held in our portfolio. Additionally, PMI has provided

mortgage insurance on loans originated and sold to third-party

investors. For loans sold to third-party investors, there is no

additional risk of repurchase loss to Wells Fargo associated with

the deferred insurance claim amounts from PMI since this credit

72