Wells Fargo 2011 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

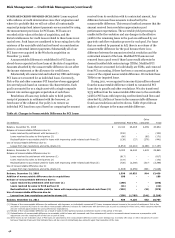

Risk Management — Credit Risk Management (continued)

PURCHASED CREDIT-IMPAIRED (PCI) LOANS

Loans acquired

with evidence of credit deterioration since their origination and

where it is probable that we will not collect all contractually

required principal and interest payments are accounted for using

the measurement provisions for PCI loans. PCI loans are

recorded at fair value at the date of acquisition, and the

historical allowance for credit losses related to these loans is not

carried over. Such loans are considered to be accruing due to the

existence of the accretable yield and not based on consideration

given to contractual interest payments. Substantially all of our

PCI loans were acquired in the Wachovia acquisition on

December 31, 2008.

A nonaccretable difference is established for PCI loans to

absorb losses expected on those loans at the date of acquisition.

Amounts absorbed by the nonaccretable difference do not affect

the income statement or the allowance for credit losses.

Substantially all commercial and industrial, CRE and foreign

PCI loans are accounted for as individual loans. Conversely,

Pick-a-Pay and other consumer PCI loans have been aggregated

into several pools based on common risk characteristics. Each

pool is accounted for as a single asset with a single composite

interest rate and an aggregate expectation of cash flows.

Resolutions of loans may include sales to third parties,

receipt of payments in settlement with the borrower, or

foreclosure of the collateral. Our policy is to remove an

individual PCI loan from a pool based on comparing the amount

received from its resolution with its contractual amount. Any

difference between these amounts is absorbed by the

nonaccretable difference. This removal method assumes that the

amount received from resolution approximates pool

performance expectations. The accretable yield percentage is

unaffected by the resolution and any changes in the effective

yield for the remaining loans in the pool are addressed by our

quarterly cash flow evaluation process for each pool. For loans

that are resolved by payment in full, there is no release of the

nonaccretable difference for the pool because there is no

difference between the amount received at resolution and the

contractual amount of the loan. Modified PCI loans are not

removed from a pool even if those loans would otherwise be

deemed troubled debt restructurings (TDRs). Modified PCI

loans that are accounted for individually are TDRs, and removed

from PCI accounting, if there has been a concession granted in

excess of the original nonaccretable difference. We include these

TDRs in our impaired loans.

During 2011, we recognized in income $239 million released

from the nonaccretable difference related to commercial PCI

loans due to payoffs and other resolutions. We also transferred

$373 million from the nonaccretable difference to the accretable

yield for PCI loans with improving credit-related cash flows and

absorbed $2.3 billion of losses in the nonaccretable difference

from loan resolutions and write-downs. Table 18 provides an

analysis of changes in the nonaccretable difference.

Table 18: Changes in Nonaccretable Difference for PCI Loans

Other

(in millions)

Commercial

Pick-a-Pay

consumer

Total

Balance, December 31, 2008

$

10,410

26,485

4,069

40,964

Release of nonaccretable difference due to:

Loans resolved by settlement with borrower (1)

(330)

-

-

(330)

Loans resolved by sales to third parties (2)

(86)

-

(85)

(171)

Reclassification to accretable yield for loans with improving credit-related cash flows (3)

(138)

(27)

(276)

(441)

Use of nonaccretable difference due to:

Losses from loan resolutions and write-downs (4)

(4,853)

(10,218)

(2,086)

(17,157)

Balance, December 31, 2009

5,003

16,240

1,622

22,865

Release of nonaccretable difference due to:

Loans resolved by settlement with borrower (1)

(817)

-

-

(817)

Loans resolved by sales to third parties (2)

(172)

-

-

(172)

Reclassification to accretable yield for loans with improving credit-related cash flows (3)

(726)

(2,356)

(317)

(3,399)

Use of nonaccretable difference due to:

Losses from loan resolutions and write-downs (4)

(1,698)

(2,959)

(391)

(5,048)

Balance, December 31, 2010

1,590

10,925

914

13,429

Addition of nonaccretable difference due to acquisitions

188

-

-

188

Release of nonaccretable difference due to:

Loans resolved by settlement with borrower (1)

(198)

-

-

(198)

Loans resolved by sales to third parties (2)

(41)

-

-

(41)

Reclassification to accretable yield for loans with improving credit-related cash flows (3)

(352)

-

(21)

(373)

Use of nonaccretable difference due to:

Losses from loan resolutions and write-downs (4)

(258)

(1,799)

(241)

(2,298)

Balance, December 31, 2011

$

929

9,126

652

10,707

(1)

Release of the nonaccretable difference for settlement with borrower, on individually accounted PCI loans, increases interest income in the period of settlement. Pick-a-Pay

and Other co

nsumer PCI loans do not reflect nonaccretable difference releases for settlements with borrowers due to pool accounting for t

hose loans, which assumes that the

amount received approximates the pool performance expectations.

(2)

Release of the nonaccretable difference as a result of sales to third parties increases noninterest income in the period of the sale.

(3)

Reclassification of nonaccretable difference to accretable yield for loans with increased cash flow estimates will result in increased interest income as a prospective yield

adjustment over the remaining life of the loan or pool of loans.

(4)

Write-downs to net realizable value of PCI loans are absorbed by the nonaccretable difference when severe delinquency (normally 180 days) or other indications of severe

borrower financial stress exist that indicate there will be a loss of contractually due amounts upon final resolution of the loan.

48