Wells Fargo 2011 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

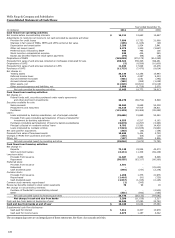

Note 1: Summary of Significant Accounting Policies (continued)

ASU 2011-08 provides entities with the option to perform a

qualitative assessment of goodwill to test for impairment. If,

based on qualitative reviews, a company concludes that more

likely than not a reporting unit’s fair value is less than its

carrying amount, then the company must complete quantitative

steps to determine if there is goodwill impairment. If a company

concludes otherwise, quantitative tests are not required. Our

adoption of this Update did not affect our consolidated financial

statements.

Accounting Standards with Retrospective Application

The following accounting pronouncements have been issued by

the FASB but are not yet effective:

Accounting Standards Update (ASU or Update) 2011-11,

Disclosures about Offsetting Assets and Liabilities;

ASU 2011-05, Presentation of Comprehensive Income; and

ASU 2011-12, Deferral of the Effective Date for

Amendments to the Presentation of Reclassifications of

Items Out of Accumulated Other Comprehensive Income in

Accounting Standards Update No. 2011-05.

ASU 2011-11 expands the disclosure requirements for financial

instruments and derivatives that may be offset in accordance

with enforceable master netting agreements or similar

arrangements. The disclosures are required regardless of

whether the instruments have been offset (or netted) in the

statement of financial position. Under ASU 2011-11, companies

must describe the nature of offsetting arrangements and provide

quantitative information about those agreements, including the

gross and net amounts of financial instruments that are

recognized in the statement of financial position. These changes

are effective for us in first quarter 2013 with retrospective

application. This Update will not affect our consolidated

financial results since it amends only the disclosure

requirements for offsetting financial instruments.

ASU 2011-05 eliminates the option for companies to include

the components of other comprehensive income in the statement

of changes in stockholders’ equity. This Update requires entities

to present the components of comprehensive income in either a

single statement or in two separate statements, with the

statement of other comprehensive income (OCI) immediately

following the statement of income. This Update also requires

companies to present amounts reclassified out of OCI and into

net income on the face of the statement of income. In December

2011, the FASB issued ASU 2011-12, which defers indefinitely

the requirement to present reclassification adjustments on the

statement of income. The remaining provisions are effective for

us in first quarter 2012 with retrospective application. Early

adoption is permitted. This Update will not affect our

consolidated financial results as it amends only the presentation

of comprehensive income.

Consolidation

Our consolidated financial statements include the accounts of

the Parent and our majority-owned subsidiaries and VIEs

(defined below) in which we are the primary beneficiary.

Significant intercompany accounts and transactions are

eliminated in consolidation. If we own at least 20% of an entity,

we generally account for the investment using the equity

method. If we own less than 20% of an entity, we generally carry

the investment at cost, except marketable equity securities,

which we carry at fair value with changes in fair value included

in OCI. Investments accounted for under the equity or cost

method are included in other assets.

We are a variable interest holder in certain special-purpose

entities (SPEs) in which equity investors do not have the

characteristics of a controlling financial interest or where the

entity does not have enough equity at risk to finance its activities

without additional subordinated financial support from other

parties (referred to as VIEs). Our variable interest arises from

contractual, ownership or other monetary interests in the entity,

which change with fluctuations in the fair value of the entity's

assets. We consolidate a VIE if we are the primary beneficiary,

defined as the party that that has both the power to direct the

activities that most significantly impact the VIE and a variable

interest that could potentially be significant to the VIE. A

variable interest is a contractual, ownership or other interest

that changes with changes in the fair value of the VIE’s net

assets. To determine whether or not a variable interest we hold

could potentially be significant to the VIE, we consider both

qualitative and quantitative factors regarding the nature, size

and form of our involvement with the VIE. We assess whether or

not we are the primary beneficiary of a VIE on an on-going basis.

Cash and Due From Banks

Cash and cash equivalents include cash on hand, cash items in

transit, and amounts due from the Federal Reserve Bank and

other depository institutions.

Trading Assets

Trading assets are primarily securities, including corporate debt,

U.S. government agency obligations and other securities that we

acquire for short-term appreciation or other trading purposes,

and the fair value of derivatives held for customer

accommodation purposes or risk mitigation and hedging.

Interest-only strips and other retained interests in

securitizations that can be contractually prepaid or otherwise

settled in a way that the holder would not recover substantially

all of its recorded investment are classified as trading assets.

Trading assets are carried at fair value, with realized and

unrealized gains and losses recorded in noninterest income.

Securities

SECURITIES AVAILABLE FOR SALE

Debt securities that we might

not hold until maturity and marketable equity securities are

classified as securities available for sale and reported at fair

value. Unrealized gains and losses, after applicable taxes, are

reported in cumulative OCI. Fair value measurement is based

upon quoted prices in active markets, if available. If quoted

prices in active markets are not available, fair values are

measured using independent pricing models or other model-

based valuation techniques such as the present value of future

cash flows, adjusted for the security's credit rating, prepayment

assumptions and other factors such as credit loss assumptions

122