Wells Fargo 2011 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

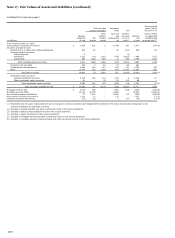

Note 16: Derivatives (continued)

Credit-Risk Contingent Features

Certain of our derivative contracts contain provisions whereby if

the credit rating of our debt, based on certain major credit rating

agencies indicated in the relevant contracts, were to fall below

investment grade, the counterparty could demand additional

collateral or require termination or replacement of derivative

instruments in a net liability position. The aggregate fair value of

all derivative instruments with such credit-risk-related

contingent features that are in a net liability position was

$17.1 billion and $12.6 billion at December 31, 2011 and 2010,

respectively, for which we had posted $15.0 billion and

$12.0 billion, respectively, in collateral in the normal course of

business. If the credit-risk-related contingent features

underlying these agreements had been triggered on December

31, 2011 or 2010, we would have been required to post additional

collateral of $2.1 billion, or $1.0 billion, respectively, or

potentially settle the contract in an amount equal to its fair

value.

Counterparty Credit Risk

By using derivatives, we are exposed to counterparty credit risk

if counterparties to the derivative contracts do not perform as

expected. If a counterparty fails to perform, our counterparty

credit risk is equal to the amount reported as a derivative asset

on our balance sheet. The amounts reported as a derivative asset

are derivative contracts in a gain position, and to the extent

subject to master netting arrangements, net of derivatives in a

loss position with the same counterparty and cash collateral

received. We minimize counterparty credit risk through credit

approvals, limits, monitoring procedures, executing master

netting arrangements and obtaining collateral, where

appropriate. To the extent the master netting arrangements and

other criteria meet the applicable requirements, derivatives

balances and related cash collateral amounts are shown net in

the balance sheet. Counterparty credit risk related to derivatives

is considered in determining fair value and our assessment of

hedge effectiveness.

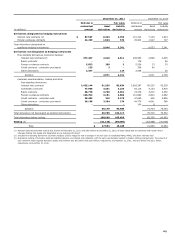

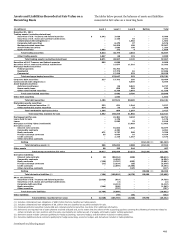

Note 17: Fair Values of Assets and Liabilities

We use fair value measurements to record fair value adjustments

to certain assets and liabilities and to determine fair value

disclosures. Trading assets, securities available for sale,

derivatives, substantially all prime residential MHFS, certain

commercial LHFS, certain loans held for investment, fair value

MSRs, principal investments and securities sold but not yet

purchased (short sale liabilities) are recorded at fair value on a

recurring basis. We generally do not record our issued debt at

fair value. Additionally, from time to time, we may be required to

record at fair value other assets on a nonrecurring basis, such as

certain residential and commercial MHFS, certain LHFS, loans

held for investment and certain other assets. These nonrecurring

fair value adjustments typically involve application of lower-of-

cost-or-market accounting or write-downs of individual assets.

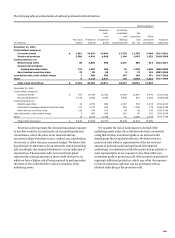

We adopted new guidance on fair value measurements

effective January 1, 2009, which addresses measuring fair value

in situations where markets are inactive and transactions are not

orderly. This guidance states transaction or quoted prices for

assets or liabilities in inactive markets may require adjustment

due to the uncertainty of whether the underlying transactions

are orderly. Prior to our adoption of the new provisions for

measuring fair value, we primarily used unadjusted independent

vendor or broker quoted prices to measure fair value for

substantially all securities available for sale.

In connection with the change in guidance for fair value

measurement, we developed policies and procedures to

determine when the level and volume of activity for our assets

and liabilities requiring fair value measurements has

significantly declined relative to normal conditions. For such

items that use price quotes, such as certain security classes

within securities available for sale, the degree of market

inactivity and distressed transactions was analyzed to determine

the appropriate adjustment to the price quotes.

The security classes where we consider the market to be less

orderly include primarily non-agency residential MBS. The

methodology used to adjust the quotes involved weighting the

price quotes and results of internal pricing techniques such as

the net present value of future expected cash flows (with

observable inputs, where available) discounted at a rate of return

market participants require. The significant inputs utilized in the

internal pricing techniques, which were estimated by type of

underlying collateral, included credit loss assumptions,

estimated prepayment speeds and appropriate discount rates.

The more active and orderly markets for particular security

classes were determined to be, the more weighting we assigned

to price quotes. The less active and orderly markets were

determined to be, the less weighting we assigned to price quotes.

We continually assess the level and volume of market activity in

our investment security classes in determining adjustments, if

any, to price quotes. Given market conditions can change over

time, determination of which securities markets are considered

active or inactive, and if inactive, the degree to which price

quotes require adjustment, can also change.

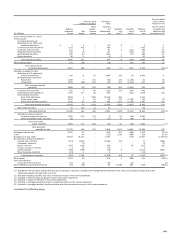

Fair Value Hierarchy

We group our assets and liabilities measured at fair value in

three levels, based on the markets in which the assets and

liabilities are traded and the reliability of the assumptions used

to determine fair value. These levels are:

Level 1 – Valuation is based upon quoted prices for identical

instruments traded in active markets.

Level 2 – Valuation is based upon quoted prices for similar

instruments in active markets, quoted prices for identical or

similar instruments in markets that are not active, and

model-based valuation techniques for which all significant

assumptions are observable in the market.

Level 3 – Valuation is generated from model-based

techniques that use significant assumptions not observable

in the market. These unobservable assumptions reflect

estimates of assumptions that market participants would

use in pricing the asset or liability. Valuation techniques

190