Wells Fargo 2011 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

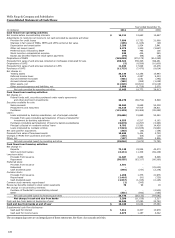

See the Glossary of Acronyms at the end of this Report for terms used throughout the Financial Statements and related Notes of this

Form 10-K.

Note 1: Summary of Significant Accounting Policies

Wells Fargo & Company is a diversified financial services

company. We provide banking, insurance, trust and

investments, mortgage banking, investment banking, retail

banking, brokerage, and consumer and commercial finance

through banking stores, the internet and other distribution

channels to consumers, businesses and institutions in all 50

states, the District of Columbia, and in other countries. When we

refer to “Wells Fargo,” “the Company,” “we,” “our” or “us,” we

mean Wells Fargo & Company and Subsidiaries (consolidated).

Wells Fargo & Company (the Parent) is a financial holding

company and a bank holding company. We also hold a majority

interest in a real estate investment trust, which has publicly

traded preferred stock outstanding.

Our accounting and reporting policies conform with U.S.

generally accepted accounting principles (GAAP) and practices

in the financial services industry. To prepare the financial

statements in conformity with GAAP, management must make

estimates based on assumptions about future economic and

market conditions (for example, unemployment, market

liquidity, real estate prices, etc.) that affect the reported amounts

of assets and liabilities at the date of the financial statements and

income and expenses during the reporting period and the related

disclosures. Although our estimates contemplate current

conditions and how we expect them to change in the future, it is

reasonably possible that actual conditions could be worse than

anticipated in those estimates, which could materially affect our

results of operations and financial condition. Management has

made significant estimates in several areas, including allowance

for credit losses and purchased credit-impaired (PCI) loans

(Note 6), valuations of residential mortgage servicing rights

(MSRs) (Notes 8 and 9) and financial instruments (Note 17),

liability for mortgage loan repurchase losses (Note 9) and

income taxes (Note 21). Actual results could differ from those

estimates.

Accounting Standards Adopted in 2011

In first quarter 2011, we adopted certain provisions of

Accounting Standards Update (ASU or Update) 2010-6,

Improving Disclosures about Fair Value Measurements.

ASU 2010-06 amends the disclosure requirements for fair

value measurements. Companies are required to disclose

significant transfers in and out of Levels 1 and 2 of the fair value

hierarchy. This Update also clarifies that fair value measurement

disclosures should be presented for each asset and liability class,

which is generally a subset of a line item in the statement of

financial position. In the rollforward of Level 3 activity,

companies must present information on purchases, sales,

issuances, and settlements on a gross basis rather than on a net

basis. Companies should also provide information about the

valuation techniques and inputs used to measure fair value for

both recurring and nonrecurring instruments classified as either

Level 2 or Level 3. In first quarter 2011, we adopted the

requirement for gross presentation in the Level 3 rollforward

with prospective application. The remaining provisions were

effective for us in first quarter 2010. Our adoption of this Update

did not affect our consolidated financial statement results since

it amends only the disclosure requirements for fair value

measurements.

In third quarter 2011, we adopted the following new

accounting guidance:

Certain provisions of ASU 2010-20, Disclosures about the

Credit Quality of Financing Receivables and the Allowance

for Credit Losses; and

ASU 2011-02, A Creditor’s Determination of Whether a

Restructuring is a Troubled Debt Restructuring.

ASU 2010-20 requires enhanced disclosures for the allowance

for credit losses and financing receivables, which include certain

loans and long-term accounts receivables. Companies are

required to disaggregate credit quality information and roll

forward the allowance for credit losses by portfolio segment.

Companies must also provide supplemental information on the

nature and extent of troubled debt restructurings (TDRs) and

their effect on the allowance for credit losses. We adopted the

new disclosure requirements for TDRs in third quarter 2011 with

retrospective application to January 1, 2011. The remaining

provisions were effective for us in fourth quarter 2010.

Our

adoption of this Update did not affect our consolidated financial

statement results since it amends only the disclosure

requirements for financing receivables and the allowance for

credit losses.

ASU 2011-02 provides guidance clarifying under what

circumstances a creditor should classify a restructured receivable

as a TDR. A receivable is a TDR if both of the following exist: 1) a

creditor has granted a concession to the debtor, and 2) the

debtor is experiencing financial difficulties. This Update clarifies

that a creditor should consider all aspects of a restructuring

when evaluating whether it has granted a concession, which

include determining whether a debtor can obtain funds from

another source at market rates and assessing the value of

additional collateral and guarantees obtained at the time of

restructuring. This Update also provides factors a creditor

should consider when determining if a debtor is experiencing

financial difficulties, such as probability of payment default and

bankruptcy declarations. This guidance was effective for us in

third quarter 2011 with retrospective application to

January 1, 2011. Our adoption of this Update did not have a

material effect on our consolidated financial statements.

In fourth quarter 2011, we early adopted ASU 2011-08,

Testing Goodwill for Impairment.

121