Wells Fargo 2011 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

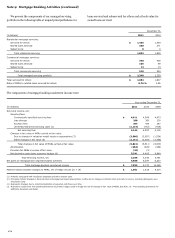

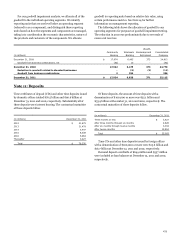

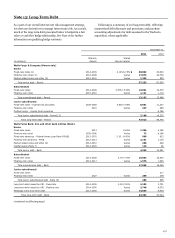

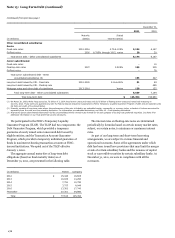

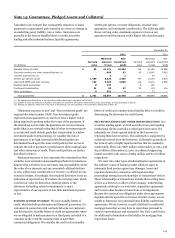

Note 15: Legal Actions (continued)

Securities Corp., et al., were filed in the Superior Court for the

State of California, San Francisco County against a number of

defendants, including Wells Fargo Bank, N.A. and Wells Fargo

Asset Securities Corporation. As against the Wells Fargo entities,

the new cases assert opt out claims relating to the claims alleged

in the Mortgage-Backed Certificates Litigation.

On October 15, 2010, three actions, captioned Federal Home

Loan Bank of Chicago v. Banc of America Funding

Corporation, et al. (filed in the Cook County Circuit Court, State

of Illinois); Federal Home Loan Bank of Chicago v. Banc of

America Securities LLC, et al. (filed in the Superior Court of the

State of California for the County of Los Angeles); and Federal

Home Loan Bank of Indianapolis v. Banc of America Mortgage

America Securities, Inc., et al. (filed in the Superior Court of the

State of Indiana for the County of Marion), named multiple

defendants, described as issuers/depositors, and

underwriters/dealers of private label mortgage-backed

securities, in an action asserting claims that defendants used

false and misleading statements in offering documents for the

sale of such securities. The Bank of Chicago asserts that it

purchased approximately $4.2 billion and the Bank of

Indianapolis asserts that it purchased nearly $3 billion of such

securities from the defendants. Plaintiffs seek rescission of the

sales and damages under state securities and other laws and

Section 11 of the Securities Act of 1933. Wells Fargo Asset

Securities Corporation, Wells Fargo Bank, N.A. and Wells Fargo

& Company were named among the defendants.

On April 20, 2011, a case captioned Federal Home Loan of

Boston v. Ally Financial, Inc., et al., was filed in the Superior

Court of the Commonwealth of Massachusetts for the County of

Suffolk. The case names, among a large number of parties,

Wells Fargo & Company, Wells Fargo Asset Securitization

Corporation and Wells Fargo Bank, N.A. as parties and contains

allegations substantially similar to the cases filed by the other

Federal Home Loan Banks.

On April 28, 2011, a case captioned The Union Central Life

Insurance Company, et al. v. Credit Suisse First Boston

Securities Corp., et al., was filed in the U.S. District Court for the

Southern District of New York. Among other defendants, it

names Wells Fargo Asset Securitization Corporation and

Wells Fargo Bank, N.A. The case asserts various state law fraud

claims and claims for violations of Sections 10(b) and 20(a) of

the Securities Exchange Act of 1934 on behalf of three insurance

companies, relating to offerings of mortgage-backed securities

from 2005 through 2007.

In addition, there are other mortgage-related threatened or

asserted claims by entities or investors where Wells Fargo may

have indemnity or repurchase obligations, or as to which it has

entered into agreements to toll the relevant statutes of

limitations.

MORTGAGE FORECLOSURE DOCUMENT

LITIGATION

Eight

purported class actions and several individual borrower actions

related to foreclosure document practices were filed in late 2010

and in early 2011 against Wells Fargo Bank, N.A. in its status as

mortgage servicer or corporate trustee of mortgage trusts. The

cases have been brought in state and federal courts. Five of the

class actions have been dismissed or otherwise resolved. Of the

individual borrower cases, the majority are filed in state courts

in California and Ohio. The actions generally claim that Wells

Fargo submitted "fraudulent" or "untruthful" affidavits or other

foreclosure documents to courts to support foreclosures filed in

the state. Specifically, plaintiffs allege that Wells Fargo signers

did not have personal knowledge of the facts alleged in the

documents and did not verify the information in the documents

ultimately filed with courts to foreclose. Plaintiffs attempt to

state legal claims ranging from wrongful foreclosure to deceptive

practices or fraud and seek relief ranging from cancellation of

notes and mortgages to money damages.

MORTGAGE RELATED REGULATORY INVESTIGATIONS

On

April 13, 2011, Wells Fargo Bank, N.A. entered into a Consent

Order with the OCC and Wells Fargo & Company entered into a

Consent Order with the Board of Governors of the Federal

Reserve System in connection with Wells Fargo’s mortgage

foreclosure practices. The Consent Orders require Wells Fargo to

develop and implement certain compliance programs and to take

other remedial steps, which Wells Fargo is doing. On

February 9, 2012, the OCC and Federal Reserve announced that

they had also imposed civil money penalties of $83 million and

$85 million, respectively, related to the Consent Orders. These

penalties will be satisfied through payments made under a

separate simultaneous settlement in principle, announced on the

same day, among the Department of Justice (DOJ), a task force

of Attorneys General from 49 states, other government entities,

Wells Fargo and four other mortgage servicers related to

mortgage servicing and foreclosure practices. Under the

settlement in principle, Wells Fargo agreed to the following

commitments, comprised of three components totaling

$5.3 billion:

Consumer Relief Program For qualified borrowers with

financial hardship and a loan owned and serviced by Wells

Fargo, a commitment to provide $3.4 billion in aggregate

consumer relief and assistance programs, including

expanded first and second mortgage modifications that

broaden the use of principal reduction to help customers

achieve affordability, an expanded short sale program that

includes waivers of deficiency balances, forgiveness of

arrearages for unemployed borrowers, cash-for-keys

payments to borrowers who voluntarily vacate properties,

and “anti-blight” provisions designed to reduce the impact

on communities of vacant properties. As of

December 31, 2011, the expected impact of the Consumer

Relief Program was covered in our allowance for credit

losses and in the nonaccretable difference relating to our

purchased credit-impaired residential mortgage portfolio.

Refinance Program For qualified borrowers with little or

negative equity in their home and a loan owned and serviced

by Wells Fargo, an expanded first-lien refinance program

commitment estimated to provide $900 million of aggregate

payment relief over the life of the refinanced loans. The

Refinance Program will not result in any current-period

charge as its impact will be recognized over a period of years

in the form of lower interest income as qualified borrowers

benefit from reduced interest rates on loans refinanced

under the program.

182