Wells Fargo 2011 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

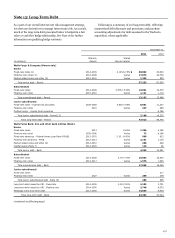

Cash Flow Hedges

We hedge floating-rate debt against future interest rate increases

by using interest rate swaps, caps, floors and futures to limit

variability of cash flows due to changes in the benchmark

interest rate. We also use interest rate swaps and floors to hedge

the variability in interest payments received on certain floating-

rate commercial loans, due to changes in the benchmark interest

rate. Gains and losses on derivatives that are reclassified from

OCI to interest income and interest expense in the current

period are included in the line item in which the hedged item’s

effect on earnings is recorded. All parts of gain or loss on these

derivatives are included in the assessment of hedge effectiveness.

We assess hedge effectiveness using regression analysis, both at

inception of the hedging relationship and on an ongoing basis.

The regression analysis involves regressing the periodic changes

in cash flows of the hedging instrument against the periodic

changes in cash flows of the forecasted transaction being hedged

due to changes in the hedged risk(s). The assessment includes an

evaluation of the quantitative measures of the regression results

used to validate the conclusion of high effectiveness.

Based upon current interest rates, we estimate that

$440 million (pre-tax) of deferred net gains on derivatives in

OCI at December 31, 2011, will be reclassified into interest

income and interest expense during the next twelve months.

Future changes to interest rates may significantly change actual

amounts reclassified to earnings. We are hedging our exposure

to the variability of future cash flows for all forecasted

transactions for a maximum of 6 years for both hedges of

floating-rate debt and floating-rate commercial loans.

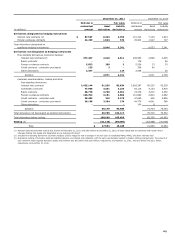

The following table shows the net gains (losses) recognized

related to derivatives in cash flow hedging relationships.

Year ended

December 31,

(in millions)

2011

2010

Gains (after tax) recognized in OCI on derivatives

$

105

468

Gains (pre tax) reclassified from cumulative OCI into net interest income

571

613

Gains (losses) (pre tax) recognized in noninterest income on derivatives (1)

(5)

6

(1) None of the change in value of the derivatives was excluded from the assessment of hedge effectiveness.

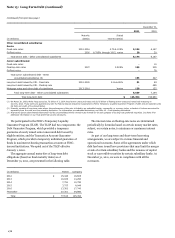

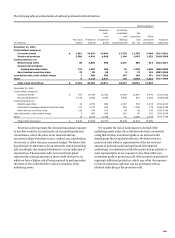

Free-Standing Derivatives

We use free-standing derivatives (economic hedges), in addition

to debt securities available for sale, to hedge the risk of changes

in the fair value of residential MSRs measured at fair value,

certain residential MHFS, derivative loan commitments and

other interests held. The resulting gain or loss on these economic

hedges is reflected in other income.

The derivatives used to hedge these MSRs measured at fair

value, which include swaps, swaptions, constant maturity

mortgages, forwards, Eurodollar and Treasury futures and

options contracts, resulted in net derivative gains of $5.2 billion

in 2011 and net derivative gains of $4.5 billion in of 2010, which

are included in mortgage banking noninterest income. The

aggregate fair value of these derivatives was a net asset of

$1.4 billion at December 31, 2011, and a net liability of

$943 million at December 31, 2010. Changes in fair value of debt

securities available for sale (unrealized gains and losses) are not

included in servicing income, but are reported in cumulative OCI

(net of tax) or, upon sale, are reported in net gains (losses) on

debt securities available for sale.

Interest rate lock commitments for residential mortgage

loans that we intend to sell are considered free-standing

derivatives. Our interest rate exposure on these derivative loan

commitments, as well as substantially all residential MHFS, is

hedged with free-standing derivatives (economic hedges) such as

swaps, forwards and options, Eurodollar futures and options,

and Treasury futures, forwards and options contracts. The

commitments, free-standing derivatives and residential MHFS

are carried at fair value with changes in fair value included in

mortgage banking noninterest income. For the fair value

measurement of interest rate lock commitments we include, at

inception and during the life of the loan commitment, the

expected net future cash flows related to the associated servicing

of the loan. Fair value changes subsequent to inception are based

on changes in fair value of the underlying loan resulting from the

exercise of the commitment and changes in the probability that

the loan will not fund within the terms of the commitment

(referred to as a fall-out factor). The value of the underlying loan

is affected primarily by changes in interest rates and the passage

of time. However, changes in investor demand can also cause

changes in the value of the underlying loan value that cannot be

hedged. The aggregate fair value of derivative loan commitments

in the balance sheet was a net asset of $478 million at

December 31, 2011, and a net liability of $271 million at

December 31, 2010, and is included in the caption “Interest rate

contracts” under “Customer accommodation, trading and other

free-standing derivatives” in the first table in this Note.

We also enter into various derivatives primarily to provide

derivative products to customers. To a lesser extent, we take

positions based on market expectations or to benefit from price

differentials between financial instruments and markets. These

derivatives are not linked to specific assets and liabilities in the

balance sheet or to forecasted transactions in an accounting

hedge relationship and, therefore, do not qualify for hedge

accounting. We also enter into free-standing derivatives for risk

management that do not otherwise qualify for hedge accounting.

They are carried at fair value with changes in fair value recorded

as other noninterest income.

Free-standing derivatives also include embedded derivatives

that are required to be accounted for separately from their host

contract. We periodically issue hybrid long-term notes and CDs

where the performance of the hybrid instrument notes is linked

to an equity, commodity or currency index, or basket of such

indices. These notes contain explicit terms that affect some or all

187