Wells Fargo 2011 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

COLLATERALIZED LOAN OBLIGATIONS (CLOs)

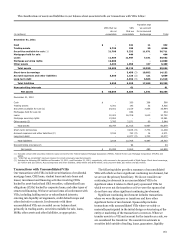

A CLO is a

securitization where an SPE purchases a pool of assets consisting

of loans and issues multiple tranches of equity or notes to

investors. Generally, CLOs are structured on behalf of a third

party asset manager that typically selects and manages the assets

for the term of the CLO. Typically, the asset manager has the

power over the significant decisions of the VIE through its

discretion to manage the assets of the CLO. We assess whether

we are the primary beneficiary of CLOs based on our role in the

transaction and the variable interests we hold. In most cases, we

are not the primary beneficiary of these transactions because we

do not have the power to manage the collateral in the VIE.

In addition to our role as arranger, we may have other forms

of involvement with these transactions. Such involvement may

include acting as underwriter, derivative counterparty,

secondary market maker or investor. For certain transactions,

we may also act as the servicer, for which we receive fees in

connection with that role. We also earn fees for arranging these

transactions and distributing the securities.

ASSET-BASED FINANCE STRUCTURES

We engage in various

forms of structured finance arrangements with VIEs that are

collateralized by various asset classes including energy contracts,

auto and other transportation leases, intellectual property,

equipment and general corporate credit. We typically provide

senior financing, and may act as an interest rate swap or

commodity derivative counterparty when necessary. In most

cases, we are not the primary beneficiary of these structures

because we do not have power over the significant activities of

the VIEs involved in these transactions.

For example, we have investments in asset-backed securities

that are collateralized by auto leases or loans and cash reserves.

These fixed-rate and variable-rate securities have been

structured as single-tranche, fully amortizing, unrated bonds

that are equivalent to investment-grade securities due to their

significant overcollateralization. The securities are issued by

VIEs that have been formed by third party auto financing

institutions primarily because they require a source of liquidity

to fund ongoing vehicle sales operations. The third party auto

financing institutions manage the collateral in the VIEs, which is

indicative of power in these transactions and we therefore do not

consolidate these VIEs.

TAX CREDIT STRUCTURES

We co-sponsor and make

investments in affordable housing and sustainable energy

projects that are designed to generate a return primarily through

the realization of federal tax credits. In some instances, our

investments in these structures may require that we fund future

capital commitments at the discretion of the project sponsors.

While the size of our investment in a single entity may at times

exceed 50% of the outstanding equity interests, we do not

consolidate these structures due to the project sponsor’s ability

to manage the projects, which is indicative of power in these

transactions.

INVESTMENT FUNDS

We do not consolidate the investment

funds because we do not absorb the majority of the expected

future variability associated with the funds’ assets, including

variability associated with credit, interest rate and liquidity risks.

During 2011, we redeemed a $1.4 billion interest in an

unconsolidated investment fund managed by one of our majority

owned subsidiaries. Upon redemption we placed the assets

received into new investment fund VIEs. We consolidated these

new VIEs because we have discretion over the management of

the assets and are the sole investor in these funds. At

December 31, 2010, we had investments of $1.4 billion and

lending arrangements of $14 million with this fund.

OTHER TRANSACTIONS WITH VIEs

In 2008, legacy Wachovia

reached an agreement to purchase at par auction rate securities

(ARS) that were sold to third-party investors by certain of its

subsidiaries. ARS are debt instruments with long-term

maturities, but which re-price more frequently, and preferred

equities with no maturity. We purchased all outstanding ARS

that were issued by VIEs and subject to the agreement. At

December 31, 2011, we held in our securities available-for-sale

portfolio $643 million of ARS issued by VIEs redeemed pursuant

to this agreement, compared with $1.6 billion at

December 31, 2010.

In 2009, we reached agreements to purchase additional ARS

from eligible investors who bought ARS through one of our

broker-dealer subsidiaries. We purchased all outstanding ARS

that were issued by VIEs and subject to the agreement. As of

December 31, 2011, we held in our securities available-for-sale

portfolio $624 million of ARS issued by VIEs redeemed pursuant

to this agreement, compared with $901 million at

December 31, 2010.

We do not consolidate the VIEs that issued the ARS because

we do not have power over the activities of the VIEs.

TRUST PREFERRED SECURITIES

In addition to the

involvements disclosed in the preceding table, through the

issuance of trust preferred securities we had junior subordinated

debt financing with a carrying value of $7.6 billion at

December 31, 2011, and $19.3 billion at December 31, 2010, and

$2.5 billion of preferred stock at December 31, 2011. In these

transactions, VIEs that we wholly own issue debt securities or

preferred equity to third party investors. All of the proceeds of

the issuance are invested in debt securities or preferred equity

that we issue to the VIEs. The VIEs’ operations and cash flows

relate only to the issuance, administration and repayment of the

securities held by third parties. We do not consolidate these VIEs

because the sole assets of the VIEs are receivables from us. This

is the case even though we own all of the voting equity shares of

the VIEs, have fully guaranteed the obligations of the VIEs and

may have the right to redeem the third party securities under

certain circumstances. We report the debt securities issued to

the VIEs as long-term junior subordinated debt and the

preferred equity securities issued to the VIEs as preferred stock

in our consolidated balance sheet.

In 2011, we redeemed $9.2 billion of trust preferred securities

that will no longer count as Tier 1 capital under the Dodd-Frank

Act and the Basel Committee guidelines known as the Basel III

standards.

165