Wells Fargo 2011 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

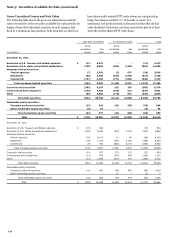

income is recognized as a constant percentage of outstanding

lease financing balances over the lease terms in interest income.

NONACCRUAL AND PAST DUE LOANS

We generally place loans

on nonaccrual status when:

the full and timely collection of interest or principal

becomes uncertain;

they are 90 days (120 days with respect to real estate 1-4

family first and junior lien mortgages) past due for interest

or principal, unless both well-secured and in the process of

collection; or

part of the principal balance has been charged off and no

restructuring has occurred.

PCI loans are written down at acquisition to fair value using

an estimate of cash flows deemed to be collectible. Accordingly,

such loans are no longer classified as nonaccrual even though

they may be contractually past due because we expect to fully

collect the new carrying values of such loans (that is, the new

cost basis arising out of purchase accounting).

When we place a loan on nonaccrual status, we reverse the

accrued unpaid interest receivable against interest income and

amortization of any net deferred fees is suspended. A loan will

remain in accruing status provided it is both well-secured and in

the process of collection. If the ultimate collectability of a loan is

in doubt and the loan is on nonaccrual, the cost recovery method

is used and cash collected is applied to first reduce the principal

outstanding. Generally, we return a loan to accrual status when

all delinquent interest and principal become current under the

terms of the loan agreement and collectability of remaining

principal and interest is no longer doubtful.

For modified loans, we underwrite at the time of a

restructuring to determine if there is sufficient evidence of

sustained repayment capacity based on the borrower’s financial

strength, including documented income, debt to income ratios

and other factors. If the borrower has demonstrated

performance under the previous terms and the underwriting

process shows the capacity to continue to perform under the

restructured terms, the loan will remain in accruing status.

When a loan classified as a TDR performs in accordance with its

modified terms, the loan either continues to accrue interest (for

performing loans) or will return to accrual status after the

borrower demonstrates a sustained period of performance

(generally six consecutive months of payments, or equivalent,

inclusive of consecutive payments made prior to the

modification). Loans will be placed on nonaccrual status and a

corresponding charge-off is recorded if we believe it is probable

that principal and interest contractually due under the modified

terms of the agreement will not be collectible.

Generally, consumer loans not secured by real estate or autos

are placed on nonaccrual status only when part of the principal

has been charged off. Loans are fully charged off or charged

down to net realizable value (fair value of collateral less

estimated costs to sell) when deemed uncollectible due to

bankruptcy or other factors, or when they reach a defined

number of days past due based on loan product, industry

practice, country, terms and other factors.

Our loans are considered past due when contractually

required principal or interest payments have not been made on

the due dates.

LOAN CHARGE-OFF POLICIES

For commercial loans, we

generally fully charge off or charge down to net realizable value

for loans secured by collateral when:

management judges the loan to be uncollectible;

repayment is deemed to be protracted beyond reasonable

time frames;

the loan has been classified as a loss by either our internal

loan review process or our banking regulatory agencies;

the customer has filed bankruptcy and the loss becomes

evident owing to a lack of assets; or

the loan is 180 days past due unless both well-secured and

in the process of collection.

For consumer loans, our charge-off policies are as follows:

1-4 family first and junior lien mortgages – We generally

charge down to net realizable value when the loan is 180

days past due.

Auto loans – We generally fully charge off when the loan is

120 days past due.

Credit card loans – We generally fully charge off when the

loan is 180 days past due.

Unsecured loans (closed end) – We generally charge off

when the loan is 120 days past due.

Unsecured loans (open end) – We generally charge off when

the loan is 180 days past due.

Other secured loans – We generally fully or partially charge

down to net realizable value when the loan is 120 days past

due.

IMPAIRED LOANS

We consider a loan to be impaired when,

based on current information and events, we determine that we

will not be able to collect all amounts due according to the loan

contract, including scheduled interest payments. This evaluation

is generally based on delinquency information, an assessment of

the borrower’s financial condition and the adequacy of collateral,

if any. Our impaired loans predominantly include loans on

nonaccrual status for commercial and industrial, commercial

real estate (CRE), foreign loans and any loans modified in a

TDR, on both accrual and nonaccrual status.

When we identify a loan as impaired, we measure the

impairment based on the present value of expected future cash

flows, discounted at the loan’s effective interest rate. When

collateral is the sole source of repayment for the loan, we may

measure impairment based on the fair value of the collateral. If

foreclosure is probable, we use the current fair value of the

collateral less estimated selling costs, instead of discounted cash

flows.

If we determine that the value of an impaired loan is less than

the recorded investment in the loan (net of previous charge-offs,

deferred loan fees or costs and unamortized premium or

discount), we recognize impairment. When the value of an

impaired loan is calculated by discounting expected cash flows,

interest income is recognized using the loan’s effective interest

rate over the remaining life of the loan.

125