Wells Fargo 2011 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

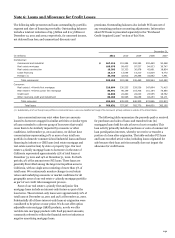

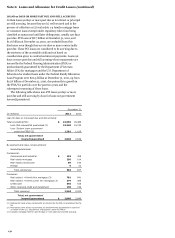

Allowance for Credit Losses (ACL)

The ACL is management’s estimate of credit losses inherent in

the loan portfolio, including unfunded credit commitments, at

the balance sheet date. We have an established process to

determine the adequacy of the allowance for credit losses that

assesses the losses inherent in our portfolio and related

unfunded credit commitments. While we attribute portions of

the allowance to specific portfolio segments, the entire allowance

is available to absorb credit losses inherent in the total loan

portfolio and unfunded credit commitments.

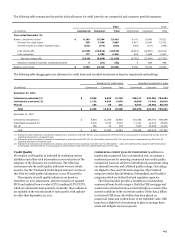

Our process involves procedures to appropriately consider

the unique risk characteristics of our commercial and consumer

loan portfolio segments. For each portfolio segment, losses are

estimated collectively for groups of loans with similar

characteristics, individually or pooled for impaired loans or, for

PCI loans, based on the changes in cash flows expected to be

collected.

Our allowance levels are influenced by loan volumes, loan

grade migration or delinquency status, historic loss experience

influencing loss factors, and other conditions influencing loss

expectations, such as economic conditions.

COMMERCIAL PORTFOLIO SEGMENT ACL METHODOLOGY

Generally, commercial loans are assessed for estimated losses by

grading each loan using various risk factors as identified through

periodic reviews. We apply historic grade-specific loss factors to

the aggregation of each funded grade pool. These historic loss

factors are also used to estimate losses for unfunded credit

commitments. In the development of our statistically derived

loan grade loss factors, we observe historical losses over a

relevant period for each loan grade. These loss estimates are

adjusted as appropriate based on additional analysis of long-

term average loss experience compared to previously forecasted

losses, external loss data or other risks identified from current

economic conditions and credit quality trends.

The allowance also includes an amount for the estimated

impairment on nonaccrual commercial loans and commercial

loans modified in a TDR, whether on accrual or nonaccrual

status.

CONSUMER PORTFOLIO SEGMENT ACL METHODOLOGY

For

consumer loans, not identified as a TDR, we determine the

allowance predominantly on a collective basis utilizing

forecasted losses to represent our best estimate of inherent loss.

We pool loans, generally by product types with similar risk

characteristics, such as residential real estate mortgages and

credit cards. As appropriate and to achieve greater accuracy, we

may further stratify selected portfolios by sub-product,

origination channel, vintage, loss type, geographic location and

other predictive characteristics. Models designed for each pool

are utilized to develop the loss estimates. We use assumptions

for these pools in our forecast models, such as historic

delinquency and default, loss severity, home price trends,

unemployment trends, and other key economic variables that

may influence the frequency and severity of losses in the pool.

In determining the appropriate allowance attributable to our

residential mortgage portfolio, we incorporate the default rates

and high severity of loss for junior lien mortgages behind

delinquent first lien mortgages into our loss forecasting

calculations. In addition, the loss rates we use in determining

our allowance include the impact of our established loan

modification programs. When modifications occur or are

probable to occur, our allowance considers the impact of these

modifications, taking into consideration the associated credit

cost, including re-defaults of modified loans and projected loss

severity. Accordingly, the loss content associated with the effects

of existing and probable loan modifications and junior lien

mortgages behind delinquent first lien mortgages has been

captured in our allowance methodology.

We separately estimate impairment for consumer loans that

have been modified in a TDR (including trial modifications),

whether on accrual or nonaccrual status.

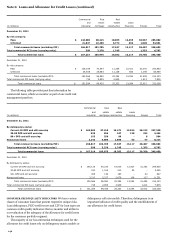

OTHER ACL MATTERS

The allowance for credit losses for both

portfolio segments includes an amount for imprecision or

uncertainty that may change from period to period. This amount

represents management’s judgment of risks inherent in the

processes and assumptions used in establishing the allowance.

This imprecision considers economic environmental factors,

modeling assumptions and performance, process risk, and other

subjective factors, including industry trends and ongoing

discussions with regulatory and government agencies regarding

mortgage foreclosure-related matters.

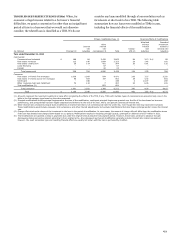

Impaired loans, which predominantly include nonaccrual

commercial loans and any loans that have been modified in a

TDR, have an estimated allowance calculated as the difference, if

any, between the impaired value of the loan and the recorded

investment in the loan. The impaired value of the loan is

generally calculated as the present value of expected future cash

flows from principal and interest which incorporates expected

lifetime losses, discounted at the loan’s effective interest rate.

The allowance for a non-impaired loan is based solely on

principal losses without consideration for timing of those losses.

The allowance for an impaired loan that was modified in a TDR

may be lower than the previously established allowance for that

loan due to benefits received through modification, such as lower

probability of default and/or severity of loss, and the impact of

prior charge-offs or charge-offs at the time of the modification

that may reduce or eliminate the need for an allowance.

Commercial and consumer PCI loans may require an

allowance subsequent to their acquisition. This allowance

requirement is due to probable decreases in expected principal

and interest cash flows (other than due to decreases in interest

rate indices and changes in prepayment assumptions).

143