Wells Fargo 2011 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

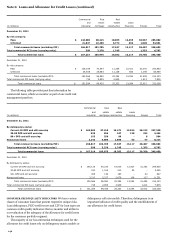

Note 6: Loans and Allowance for Credit Losses (continued)

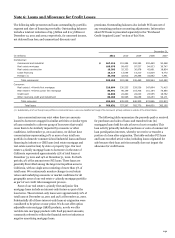

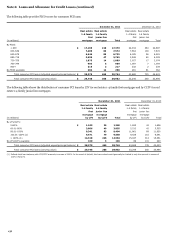

Real estate

Real estate

Other

1-4 family

1-4 family

revolving

first

junior lien

Credit

credit and

(in millions)

mortgage

mortgage

card

installment

Total

December 31, 2011

By updated FICO:

< 600

$

21,604

7,428

2,323

8,921

40,276

600-639

10,978

4,086

1,787

6,222

23,073

640-679

15,563

7,187

3,383

9,350

35,483

680-719

23,622

12,497

4,697

10,465

51,281

720-759

27,417

17,574

4,760

9,936

59,687

760-799

47,337

24,979

3,517

11,163

86,996

800+

21,381

10,247

1,969

5,674

39,271

No FICO available

4,691

1,787

400

4,393

11,271

FICO not required

-

-

-

4,990

4,990

Government insured/guaranteed loans (1)

26,555

-

-

15,346

41,901

Total consumer loans (excluding PCI)

199,148

85,785

22,836

86,460

394,229

Total consumer PCI loans (carrying value)

29,746

206

-

-

29,952

Total consumer loans

$

228,894

85,991

22,836

86,460

424,181

December 31, 2010 (2)

By updated FICO:

< 600

$

26,013

9,126

2,872

10,806

48,817

600-639

11,105

4,457

1,826

5,965

23,353

640-679

16,202

7,678

3,305

8,344

35,529

680-719

25,549

13,759

4,522

9,480

53,310

720-759

29,443

20,334

4,441

8,808

63,026

760-799

47,250

27,222

3,215

9,357

87,044

800+

19,719

10,607

1,794

4,692

36,812

No FICO available

6,195

2,716

285

7,528

16,724

FICO not required

-

-

-

4,132

4,132

Government insured/guaranteed loans (1)

15,514

-

-

17,453

32,967

Total consumer loans (excluding PCI)

196,990

95,899

22,260

86,565

401,714

Total consumer PCI loans (carrying value)

33,245

250

-

-

33,495

Total consumer loans

$

230,235

96,149

22,260

86,565

435,209

(1) Represents loans whose repayments are insured by the FHA or guaranteed by the VA and student loans whose repayments are predominantly guaranteed by agencies on

behalf of the U.S. Department of Education under FFELP. In 2011, we consolidated $5.6 billion of previously sold FHA insured real estate 1-4 family reverse mortgages.

(2) Amounts at December 31, 2010, have been revised to conform to the current separate presentation of government insured/guaranteed loans.

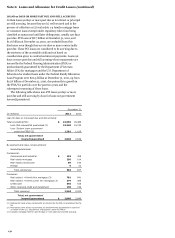

LTV refers to the ratio comparing the loan’s balance to the

property’s collateral value. CLTV refers to the combination of

first mortgage and junior lien mortgage (including unused line

amounts for credit line products) ratios. LTVs and CLTVs are

updated quarterly using a cascade approach which first uses

values provided by automated valuation models (AVMs) for the

property. If an AVM is not available, then the value is estimated

using the original appraised value adjusted by the change in

Home Price Index (HPI) for the property location. If an HPI is

not available, the original appraised value is used. The HPI value

is normally the only method considered for high value properties

as the AVM values have proven less accurate for these

properties.

The following table shows the most updated LTV and CLTV

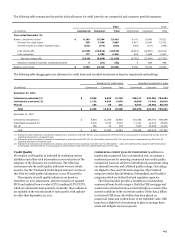

distribution of the real estate 1-4 family first and junior lien

mortgage loan portfolios. In recent years, the residential real

estate markets have experienced significant declines in property

values and several markets, particularly California and Florida

have experienced declines that turned out to be more significant

than the national decline. These trends are considered in the way

that we monitor credit risk and establish our allowance for credit

losses. LTV does not necessarily reflect the likelihood of

performance of a given loan, but does provide an indication of

collateral value. In the event of a default, any loss should be

limited to the portion of the loan amount in excess of the net

realizable value of the underlying real estate collateral value.

Certain loans do not have an LTV or CLTV primarily due to

industry data availability and portfolios acquired from or

serviced by other institutions.

148