Wells Fargo 2011 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

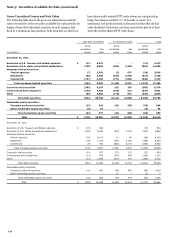

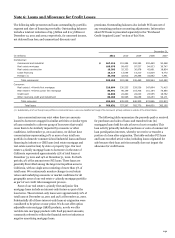

We do not have the intent to sell any securities included in the

previous table. For debt securities included in the table, we have

concluded it is more likely than not that we will not be required

to sell prior to recovery of the amortized cost basis. We have

assessed each security with gross unrealized losses for credit

impairment. For debt securities, we evaluate, where necessary,

whether credit impairment exists by comparing the present

value of the expected cash flows to the securities’ amortized cost

basis. For equity securities, we consider numerous factors in

determining whether impairment exists, including our intent

and ability to hold the securities for a period of time sufficient to

recover the cost basis of the securities.

See Note 1 – “Securities” for the factors that we consider in

our analysis of OTTI for debt and equity securities available for

sale.

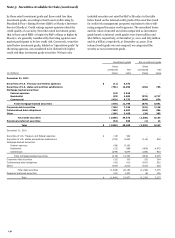

SECURITIES OF U.S. TREASURY AND FEDERAL AGENCIES AND

FEDERAL AGENCY MORTGAGE-BACKED SECURITIES (MBS)

The unrealized losses associated with U.S. Treasury and federal

agency securities and federal agency MBS are primarily driven

by changes in interest rates and not due to credit losses given the

explicit or implicit guarantees provided by the U.S. government.

SECURITIES OF U.S. STATES AND POLITICAL SUBDIVISIONS

The unrealized losses associated with securities of U.S. states

and political subdivisions are primarily driven by changes in

interest rates and not due to the credit quality of the securities.

Substantially all of these investments are investment grade. The

securities were generally underwritten in accordance with our

own investment standards prior to the decision to purchase.

Some of these securities are guaranteed by a bond insurer, but

we did not rely on this guarantee in making our investment

decision. These investments will continue to be monitored as

part of our ongoing impairment analysis, but are expected to

perform, even if the rating agencies reduce the credit rating of

the bond insurers. As a result, we expect to recover the entire

amortized cost basis of these securities.

RESIDENTIAL AND COMMERCIAL MBS

The unrealized losses

associated with private residential MBS and commercial MBS

are primarily driven by changes in projected collateral losses,

credit spreads and interest rates. We assess for credit

impairment by estimating the present value of expected cash

flows. The key assumptions for determining expected cash flows

include default rates, loss severities and prepayment rates. We

estimate losses to a security by forecasting the underlying

mortgage loans in each transaction. We use forecasted loan

performance to project cash flows to the various tranches in the

structure. We also consider cash flow forecasts and, as

applicable, independent industry analyst reports and forecasts,

sector credit ratings, and other independent market data. Based

upon our assessment of the expected credit losses and the credit

enhancement level of the securities, we expect to recover the

entire amortized cost basis of these securities.

CORPORATE DEBT SECURITIES

The unrealized losses

associated with corporate debt securities are primarily related to

unsecured debt obligations issued by various corporations. We

evaluate the financial performance of each issuer on a quarterly

basis to determine that the issuer can make all contractual

principal and interest payments. Based upon this assessment, we

expect to recover the entire amortized cost basis of these

securities.

COLLATERALIZED DEBT OBLIGATIONS (CDOs)

The unrealized

losses associated with CDOs relate to securities primarily backed

by commercial, residential or other consumer collateral. The

unrealized losses are primarily driven by changes in projected

collateral losses, credit spreads and interest rates. We assess for

credit impairment by estimating the present value of expected

cash flows. The key assumptions for determining expected cash

flows include default rates, loss severities and prepayment rates.

We also consider cash flow forecasts and, as applicable,

independent industry analyst reports and forecasts, sector credit

ratings, and other independent market data. Based upon our

assessment of the expected credit losses and the credit

enhancement level of the securities, we expect to recover the

entire amortized cost basis of these securities.

OTHER DEBT SECURITIES

The unrealized losses associated with

other debt securities primarily relate to other asset-backed

securities. The losses are primarily driven by changes in

projected collateral losses, credit spreads and interest rates. We

assess for credit impairment by estimating the present value of

expected cash flows. The key assumptions for determining

expected cash flows include default rates, loss severities and

prepayment rates. Based upon our assessment of the expected

credit losses and the credit enhancement level of the securities,

we expect to recover the entire amortized cost basis of these

securities.

MARKETABLE EQUITY SECURITIES

Our marketable equity

securities include investments in perpetual preferred securities,

which provide very attractive tax-equivalent yields. We evaluated

these hybrid financial instruments with investment-grade

ratings for impairment using an evaluation methodology similar

to that used for debt securities. Perpetual preferred securities are

not considered to be other-than-temporarily impaired if there is

no evidence of credit deterioration or investment rating

downgrades of any issuers to below investment grade, and we

expect to continue to receive full contractual payments. We will

continue to evaluate the prospects for these securities for

recovery in their market value in accordance with our policy for

estimating OTTI. We have recorded impairment write-downs on

perpetual preferred securities where there was evidence of credit

deterioration.

OTHER SECURITIES AVAILABLE FOR SALE MATTERS

The fair

values of our investment securities could decline in the future if

the underlying performance of the collateral for the residential

and commercial MBS or other securities deteriorate and our

credit enhancement levels do not provide sufficient protection to

our contractual principal and interest. As a result, there is a risk

that significant OTTI may occur in the future.

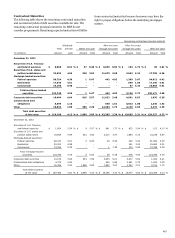

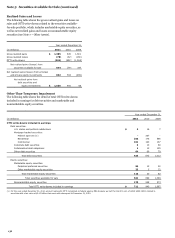

The following table shows the gross unrealized losses and fair

value of debt and perpetual preferred securities available for sale

135