Wells Fargo 2011 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2011 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

Note 1: Summary of Significant Accounting Policies (continued)

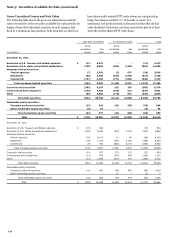

a reporting unit fair value is not less than its carrying amount,

quantitative tests are not required. We have determined that our

reporting units are one level below the operating segments. We

assess goodwill for impairment on a reporting unit level and

apply various quantitative valuation methodologies when

required to compare the estimated fair value to the carrying

value of each reporting unit. Valuation methodologies include

discounted cash flow and earnings multiple approaches. If the

fair value is less than the carrying amount, an additional test is

required to measure the amount of impairment. We recognize

impairment losses as a charge to noninterest expense (unless

related to discontinued operations) and an adjustment to the

carrying value of the goodwill asset. Subsequent reversals of

goodwill impairment are prohibited.

We amortize core deposit and other customer relationship

intangibles on an accelerated basis over useful lives not

exceeding 10 years. We review such intangibles for impairment

whenever events or changes in circumstances indicate that their

carrying amounts may not be recoverable. Impairment is

indicated if the sum of undiscounted estimated future net cash

flows is less than the carrying value of the asset. Impairment is

permanently recognized by writing down the asset to the extent

that the carrying value exceeds the estimated fair value.

Operating Lease Assets

Operating lease rental income for leased assets is recognized in

other income on a straight-line basis over the lease term. Related

depreciation expense is recorded on a straight-line basis over the

estimated useful life, considering the estimated residual value of

the leased asset. The useful life may be adjusted to the term of

the lease depending on our plans for the asset after the lease

term. On a periodic basis, leased assets are reviewed for

impairment. Impairment loss is recognized if the carrying

amount of leased assets exceeds fair value and is not recoverable.

The carrying amount of leased assets is not recoverable if it

exceeds the sum of the undiscounted cash flows expected to

result from the lease payments and the estimated residual value

upon the eventual disposition of the equipment.

Liability for Mortgage Loan Repurchase Losses

We sell residential mortgage loans to various parties, including

(1) Freddie Mac and Fannie Mae (government-sponsored

entities (GSEs)), which include the mortgage loans in GSE-

guaranteed mortgage securitizations, (2) special purpose entities

that issue private label MBS, and (3) other financial institutions

that purchase mortgage loans for investment or private label

securitization. In addition, we pool Federal Housing

Administration (FHA)-insured and Department of Veterans

Affairs (VA)-guaranteed mortgage loans, which back securities

guaranteed by the Government National Mortgage Association

(GNMA).

We may be required to repurchase mortgage loans,

indemnify the securitization trust, investor or insurer, or

reimburse the securitization trust, investor or insurer for credit

losses incurred on loans (collectively “repurchase”) in the event

of a breach of specified contractual representations or warranties

that are not remedied within a period (usually 90 days or less)

after we receive notice of the breach. Our loan sale contracts to

private investors (non-GSE) typically contain an additional

provision where we would only be required to repurchase

securitized loans if a breach is deemed to have a material and

adverse effect on the value of the mortgage loan or to the

investors or interests of security holders in the mortgage loan.

We establish mortgage repurchase liabilities related to

various representations and warranties that reflect

management’s estimate of losses for loans for which we could

have a repurchase obligation, whether or not we currently

service those loans, based on a combination of factors. Such

factors include default expectations, expected investor

repurchase demands (influenced by current and expected

mortgage loan file requests and mortgage insurance rescissions

notices, as well as estimated demand to default and file request

relationships) and appeals success rates (where the investor

rescinds the demand based on a cure of the defect or

acknowledges that the loan satisfies the investor’s applicable

representations and warranties), reimbursement by

correspondent and other third party originators, and projected

loss severity. We establish a liability at the time loans are sold

and continually update our liability estimate during their life.

Although investors may demand repurchase at any time and

there is often a lag from the date of default to the time we receive

a repurchase demand, the majority of repurchase demands occur

on loans that default in the first 24 to 36 months following

origination of the mortgage loan and can vary by investor.

The liability for mortgage loan repurchase losses is included

in other liabilities. For additional information on our repurchase

liability, see Note 9.

Pension Accounting

We account for our defined benefit pension plans using an

actuarial model as more fully discussed in Note 20.

Income Taxes

We file consolidated and separate company federal income tax

returns, foreign tax returns and various combined and separate

company state tax returns.

We evaluate two components of income tax expense: current

and deferred. Current income tax expense approximates taxes to

be paid or refunded for the current period and includes income

tax expense related to our uncertain tax positions. We determine

deferred income taxes using the balance sheet method. Under

this method, the net deferred tax asset or liability is based on the

tax effects of the differences between the book and tax bases of

assets and liabilities, and recognizes enacted changes in tax rates

and laws in the period in which they occur. Deferred income tax

expense results from changes in deferred tax assets and

liabilities between periods. Deferred tax assets are recognized

subject to management's judgment that realization is “more

likely than not.” Uncertain tax positions that meet the more

likely than not recognition threshold are measured to determine

the amount of benefit to recognize. An uncertain tax position is

measured at the largest amount of benefit that management

believes has a greater than 50% likelihood of realization upon

settlement. Foreign taxes paid are generally applied as credits to

reduce federal income taxes payable. We account for interest and

penalties as a component of income tax expense.

128