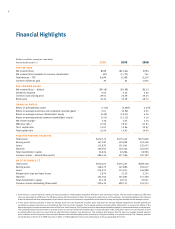

SunTrust 2010 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2010 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

Oa minimum ratio of Tier 1 capital to risk-weighted assets of at least 6.0%, plus the capital conservation

buffer (which is added to the 6.0% Tier 1 capital ratio as that buffer is phased in, effectively resulting in a

minimum Tier 1 capital ratio of 8.5% upon full implementation);

Oa minimum ratio of Total (that is, Tier 1 plus Tier 2) capital to risk-weighted assets of at least 8.0%, plus

the capital conservation buffer (which is added to the 8.0% total capital ratio as that buffer is phased in,

effectively resulting in a minimum total capital ratio of 10.5% upon full implementation); and

Oas a newly adopted international standard, a minimum leverage ratio of 3%, calculated as the ratio of Tier

1 capital to balance sheet exposures plus certain off-balance sheet exposures (as the average for each

quarter of the month-end ratios for the quarter); and

•provides for a “countercyclical capital buffer,” generally to be imposed when national regulators determine

that excess aggregate credit growth becomes associated with a buildup of systemic risk, that would be a Tier 1

Common Equity add-on to the capital conservation buffer in the range of 0% to 2.5% when fully implemented

(potentially resulting in total buffers of between 2.5% and 5%).

The capital conservation buffer is designed to absorb losses during periods of economic stress. Banking institutions with a

ratio of Tier 1 Common Equity to risk-weighted assets above the minimum but below the conservation buffer (or below the

combined capital conservation buffer and countercyclical capital buffer, when the latter is applied) may face constraints on

dividends, equity repurchases and compensation.

The implementation of the Basel III final framework will commence January 1, 2013. On that date, banking institutions will

be required to meet the following minimum capital ratios before the application of any buffer:

•3.5% Tier 1 Common Equity to risk-weighted assets;

•4.5% Tier 1 capital to risk-weighted assets; and

•8.0% Total capital to risk-weighted assets.

The Basel III final framework provides for a number of new deductions from and adjustments to Tier 1 Common Equity.

These include, for example, the requirement that MSRs, deferred tax assets dependent upon future taxable income and

significant investments in non-consolidated financial entities be deducted from Tier 1 Common Equity to the extent that any

one such category exceeds 10% of Tier 1 Common Equity or all such categories in the aggregate exceed 15% of Tier 1

Common Equity.

Implementation of the deductions and other adjustments to Tier 1 Common Equity will begin on January 1, 2014 and will be

phased in over a five-year period (20% per year). The implementation of the capital conservation buffer will begin on

January 1, 2016 at 0.625% and be phased in over a four-year period (increasing by that amount on each subsequent

January 1, until it reaches 2.5% on January 1, 2019).

The U.S. banking agencies have indicated informally that they expect to propose regulations implementing Basel III in mid

2011 with final adoption of implementing regulations in mid 2012. Notwithstanding its release of the Basel III framework as

a final framework, the Basel Committee is considering further amendments to Basel III, including the imposition of

additional capital surcharges on “globally systemically important financial institutions,” which we expect will apply to us. In

addition to Basel III, the Dodd-Frank Act requires or permits the Federal banking agencies to adopt regulations affecting

banking institutions’ capital requirements in a number of respects, including potentially more stringent capital requirements

for systemically important financial institutions. We believe our current capital levels already exceed the Basel III capital

requirement, including the capital conservation buffer. The BCBS has also stated that from time to time it may require an

additional, counter-cyclical capital buffer on top of Basel III standards. We intend to comply with those requirements when

announced as they may apply to us.

Liquidity Ratios under Basel III

Historically, regulation and monitoring of bank and bank holding company liquidity has been addressed as a supervisory

matter, both in the U.S. and internationally, without required formulaic measures. The Basel III final framework requires

banks and bank holding companies to measure their liquidity against specific liquidity tests that, although similar in some

respects to liquidity measures historically applied by banks and regulators for management and supervisory purposes, going

forward will be required by regulation. One test, referred to as the LCR, is designed to ensure that the banking entity

maintains a level of unencumbered high-quality liquid assets greater than or equal to the entity’s expected net cash outflow

4