SunTrust 2010 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2010 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

SUNTRUST BANKS, INC.

Notes to Consolidated Financial Statements (Continued)

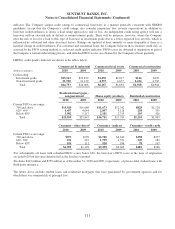

Below is a summary of transfers of financial assets to VIEs for which the Company has retained some level of continuing

involvement.

Residential Mortgage Loans

The Company typically transfers first lien residential mortgage loans in conjunction with Ginnie Mae, Fannie Mae, and

Freddie Mac securitization transactions whereby the loans are exchanged for cash or securities that are readily redeemed

for cash proceeds and servicing rights. The securities issued through these transactions are guaranteed by the issuer and,

as such, under seller/servicer agreements the Company is required to service the loans in accordance with the issuers’

servicing guidelines and standards. The Company sold residential mortgage loans to these entities, which resulted in

pre-tax gains of $588 million, $707 million, and $307 million, including servicing rights, for the years ended

December 31, 2010, 2009 and 2008, respectively. These gains are included within mortgage production related income

in the Consolidated Statements of Income/(Loss). These gains include the change in value of the loans as a result of

changes in interest rates from the time the related IRLCs were issued to the borrowers but do not include the results of

hedging activities initiated by the Company to mitigate this market risk. See Note 17, “Derivative Financial

Instruments,” to the Consolidated Financial Statements for further discussion of the Company’s hedging activities. As

seller, the Company has made certain representations and warranties with respect to the originally transferred loans,

including those transferred under Ginnie Mae, Fannie Mae, and Freddie Mac programs, which are discussed in Note 18,

“Reinsurance Arrangements and Guarantees,” to the Consolidated Financial Statements.

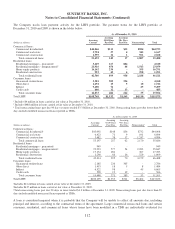

In a limited number of securitizations, the Company has transferred loans to trusts, which previously qualified as QSPEs,

sponsored by the Company. These trusts issue securities which are ultimately supported by the loans in the underlying

trusts. In these transactions, the Company has received securities representing retained interests in the transferred loans

in addition to cash and servicing rights in exchange for the transferred loans. The received securities are carried at fair

value as either trading assets or securities AFS. As of December 31, 2010 and 2009, the fair value of securities received

totaled $193 million and $217 million, respectively. At December 31, 2010, securities with a fair value of $175 million

were valued using a third party pricing service. The remaining $18 million in securities consist of subordinate interests

from a 2003 securitization of prime fixed and floating rate loans and were valued using a discounted cash flow model

that uses historically derived prepayment rates and credit loss assumptions along with estimates of current market

discount rates. The Company did not significantly modify the assumptions used to value these retained interests at

December 31, 2010 from the assumptions used to value the interests at December 31, 2009. For both periods, analyses of

the impact on the fair values of two adverse changes from the key assumptions were performed and the resulting

amounts were insignificant for each key assumption and in the aggregate.

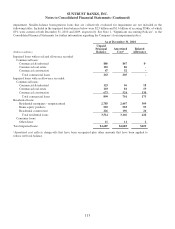

The Company evaluated these securitization transactions for consolidation under the newly adopted VIE consolidation

guidance. As servicer of the underlying loans, the Company is generally deemed to have power over the securitization.

However, if a single party, such as the issuer or the master servicer, effectively controls the servicing activities or has the

unilateral ability to terminate the Company as servicer without cause, then that party is deemed to have power. In almost all of

its securitization transactions, the Company does not retain power over the securitization as a result of these rights held by the

master servicer; therefore, an analysis of the economics of the securitization is not necessary. In certain transactions, the

Company does have power as the servicer; however, the Company does not also have an obligation to absorb losses or the

right to receive benefits that could potentially be significant to the securitization. The absorption of losses and the receipt of

benefits would generally manifest itself through the retention of senior or subordinated interests. As of January 1, 2010, the

Company determined that it was not the primary beneficiary of, and thus did not consolidate, any of these securitization

entities. No events occurred during year ended December 31, 2010 that would change the Company’s previous conclusion that

it is not the primary beneficiary of any of these securitization entities. Total assets as of December 31, 2010 and December 31,

2009 of the unconsolidated trusts in which the Company has a VI are $651 million and $780 million, respectively.

The Company’s maximum exposure to loss related to the unconsolidated VIEs in which it holds a VI is comprised of the

loss of value of any interests it retains and any repurchase obligations it incurs as a result of a breach of its

representations and warranties.

Separately, the Company has accrued $81 million and $36 million as of December 31, 2010 and 2009, respectively, for

expected losses related to certain of its representations and warranties made in connection with certain transfers of

120