Capital One 2014 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

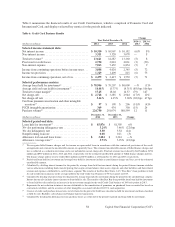

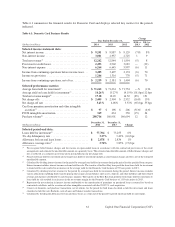

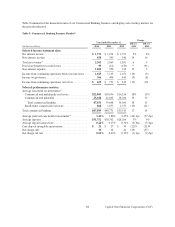

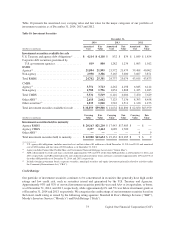

December 31, December 31,

(Dollars in millions) 2014 2013 Change

Selected period-end data:

Loans held for investment:

(3)

Auto . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 37,824 $ 31,857 19%

Home loan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30,035 35,282 (15)

Retail banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,580 3,623 (1)

Total consumer banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 71,439 $ 70,762 1

30+ day performing delinquency rate . . . . . . . . . . . . . . . . . . 3.60% 3.20% 40 bps

30+ day performing delinquency rate (excluding

Acquired Loans)

(4)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.34 5.32 2

30+ day delinquency rate . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.23 3.89 34

30+ day delinquency rate (excluding Acquired Loans)

(4)

. . . 6.28 6.47 (19)

Nonperforming loans rate . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.77 0.86 (9)

Nonperforming loans rate (excluding Acquired Loans)

(4)

. . 1.14 1.44 (30)

Nonperforming asset rate

(5)

. . . . . . . . . . . . . . . . . . . . . . . . . . 1.06 1.12 (6)

Nonperforming asset rate (excluding Acquired Loans)

(4)

. . . 1.57 1.86 (29)

Allowance for loan and lease losses . . . . . . . . . . . . . . . . . . . $ 779 $ 752 4%

Allowance coverage ratio

(6)

. . . . . . . . . . . . . . . . . . . . . . . . . 1.09% 1.06% 3 bps

Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 168,078 $ 167,652 —%

Loans serviced for others . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,701 7,665 (13)

(1) The average balance of Consumer Banking loans held for investment, excluding Acquired Loans, was $45.4 billion, $40.8 billion and $36.7

billion in 2014, 2013 and 2012, respectively.

(2) Calculated by dividing interest income for the period by average loans held for investment during the period. Interest income excludes

various allocations including funds transfer pricing that assigns certain balance sheet assets, deposits and other liabilities and their related

revenue and expenses attributable to each business segment.

(3) Includes Acquired Loans in our consumer banking loan portfolio with carrying values of $23.3 billion and $28.2 billion as of December 31,

2014 and 2013, respectively.

(4) Calculation of ratio adjusted to exclude the impact from Acquired Loans. See Credit Risk Profile and “Note 1—Summary of Significant

Accounting Policies” for additional information on the impact of Acquired Loans on our credit quality metrics.

(5) Calculated by dividing nonperforming assets as of the end of the period by the sum of period-end loans held for investment, foreclosed

properties, and other foreclosed assets.

(6) Calculated by dividing the allowance for loan and lease losses as of the end of the period by period-end loans held for investment.

Key factors affecting the results of our Consumer Banking business for 2014, compared to 2013, and changes in

financial condition and credit performance between December 31, 2014 and December 31, 2013 include the

following:

•Net Interest Income: Net interest income decreased by $157 million or 3%, to $5.7 billion in 2014, compared

to $5.9 billion in 2013. The decrease in net interest income was primarily attributable to compression in deposit

spreads in retail banking, declining home loan portfolio balances, and margin compression in our auto loan

portfolio. The decreases were partially offset by higher net interest income generated by growth in our auto

loan portfolio.

Consumer Banking yields increased to 6.3% in 2014, as compared to 6.1% in 2013. The increase in 2014 from

2013 was driven by changes in the product mix in Consumer Banking as a result of growth in our auto loan

portfolio and the run-off of the acquired home loan portfolio. The increase in our auto loans in relation to our

total consumer banking loan portfolio drove an increase in the total Consumer Banking yield, even as the average

yield on auto loans decreased to 8.7% in 2014 as compared to 9.8% in 2013. This decrease was primarily

attributable to a shift to a higher portion of prime auto loans and increased competition in the auto business.

The average yield on home loans was 3.8% and 3.4% in 2014 and 2013, respectively. The higher yield in the

home loan portfolio was driven by an increase in expected cash flows as a result of credit improvement on the

acquired home loan portfolio.

65 Capital One Financial Corporation (COF)