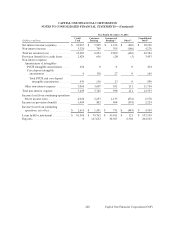

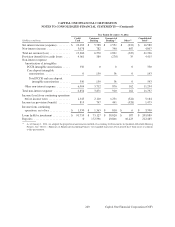

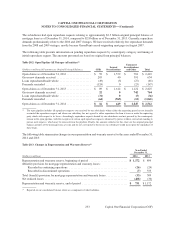

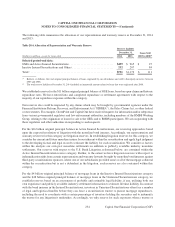

Capital One 2014 Annual Report Download - page 279

Download and view the complete annual report

Please find page 279 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

member banks, including Capital One (collectively “the Opt-Out Plaintiffs”). Relatedly, in December 2013,

individual consumer plaintiffs also filed a proposed national class action against a number of banks, including

Capital One, alleging that because the banks conspired to fix interchange fees, consumers were forced to pay

more for the fees than appropriate. The consumer case and virtually all of the opt-out cases were consolidated

before the U.S. District Court for the Eastern District of New York for certain purposes, including discovery. In

November 2014, the court dismissed the proposed consumer class action. The remaining consolidated cases are

in their preliminary stages, and Visa and MasterCard have settled a number of individual opt-out cases, requiring

non-material payments from all banks, including Capital One.

As members of Visa, our subsidiary banks have indemnification obligations to Visa with respect to final judgments

and settlements, including the Interchange Lawsuits. In the first quarter of 2008, Visa completed an IPO of its

stock. With IPO proceeds, Visa established an escrow account for the benefit of member banks to fund certain

litigation settlements and claims, including the Interchange Lawsuits. As a result, in the first quarter of 2008, we

reduced our Visa-related indemnification liabilities of $91 million recorded in other liabilities with a corresponding

reduction of other non-interest expense. We made an election in accordance with the accounting guidance for

fair value option for financial assets and liabilities on the indemnification guarantee to Visa, and the fair value of

the guarantee as of December 31, 2014 was zero. Separately, in January 2011, we entered into a MasterCard

Settlement and Judgment Sharing Agreement, along with other defendant banks, which apportions between

MasterCard and its member banks the costs and liabilities of any judgment or settlement arising from the

Interchange Lawsuits.

In March 2011, a furniture store owner named Mary Watson filed a proposed class action in the Supreme Court of

British Columbia against Visa, MasterCard, and several banks, including Capital One (the “Watson Litigation”).

The lawsuit asserts, among other things, that the defendants conspired to fix the merchant discount fees that

merchants pay on credit card transactions in violation of Section 45 of the Competition Act and seeks unspecified

damages and injunctive relief. In addition, Capital One has been named as a defendant in similar proposed class

action claims filed in other jurisdictions in Canada. In March 2014, the court granted a partial motion for class

certification. Both parties appealed the decision to the Court of Appeal for British Columbia, which heard oral

argument in December 2014.

Credit Card Interest Rate Litigation

The Capital One Bank Credit Card Interest Rate Multi-district Litigation matter was created as a result of a

June 2010 transfer order issued by the United States Judicial Panel on Multi-district Litigation (“MDL”), which

consolidated for pretrial proceedings in the U.S. District Court for the Northern District of Georgia two pending

putative class actions against COBNA-Nancy Mancuso, et al. v. Capital One Bank (USA), N.A., et al., (E.D.

Virginia); and Kevin S. Barker, et al. v. Capital One Bank (USA), N.A., (N.D. Georgia). A third action, Jennifer

L. Kolkowski v. Capital One Bank (USA), N.A., (C.D. California) was subsequently transferred into the MDL.

In August 2010, the plaintiffs in the MDL filed a Consolidated Amended Complaint alleging that COBNA

breached its contractual obligations, and violated the Truth in Lending Act (“TILA”), the California Consumers

Legal Remedies Act, the UCL, the California False Advertising Act, the New Jersey Consumer Fraud Act, and

the Kansas Consumer Protection Act when it raised interest rates on certain credit card accounts. As a result of a

settlement in another matter, the California-based UCL and TILA claims in the MDL are extinguished. The MDL

plaintiffs seek statutory damages, restitution, attorney’s fees and an injunction against future rate increases. In

August 2011, after the completion of fact discovery, Capital One filed a motion for summary judgment, which

was granted in September 2014. Plaintiffs filed a Notice of Appeal to the Eleventh Circuit Court of Appeals in

October 2014.

257

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Capital One Financial Corporation (COF)