Capital One 2014 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

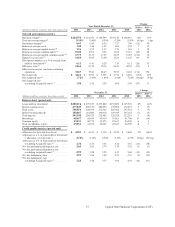

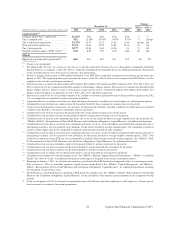

|

|

a level based on the lowest level of any input that is significant to the fair value measurement in its entirety. The three

levels of the fair value hierarchy are described below:

Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities

Level 2: Observable market-based inputs, other than quoted prices in active markets for identical assets or

liabilities

Level 3: Unobservable inputs

The degree of management judgment involved in determining the fair value of a financial instrument is dependent

upon the availability of quoted prices in active markets or observable market parameters. When quoted prices and

observable data in active markets are not fully available, management judgment is necessary to estimate fair value.

Changes in market conditions, such as reduced liquidity in the capital markets or changes in secondary market

activities, may reduce the availability and reliability of quoted prices or observable data used to determine fair value.

We have developed policies and procedures to determine when markets for our financial assets and liabilities are

inactive if the level and volume of activity has declined significantly relative to normal conditions. If markets are

determined to be inactive, it may be appropriate to adjust price quotes received. When significant adjustments are

required to price quotes or inputs, it may be appropriate to utilize an estimate based primarily on unobservable

inputs.

Significant judgment may be required to determine whether certain financial instruments measured at fair value are

classified as Level 2 or Level 3. In making this determination, we consider all available information that market

participants use to measure the fair value of the financial instrument, including observable market data, indications

of market liquidity and orderliness, and our understanding of the valuation techniques and significant inputs used.

Based upon the specific facts and circumstances of each instrument or instrument category, judgments are made

regarding the significance of the Level 3 inputs to the instruments’ fair value measurement in its entirety. If Level 3

inputs are considered significant, the instrument is classified as Level 3. The process for determining fair value using

unobservable inputs is generally more subjective and involves a high degree of management judgment and

assumptions.

Our financial instruments recorded at fair value on a recurring basis represented approximately 13% and 14% of

our total assets as of December 31, 2014 and 2013, respectively. Financial assets for which the fair value was

determined using significant Level 3 inputs represented approximately 4% and 8% of these financial instruments as

of December 31, 2014 and 2013, respectively.

We discuss changes in the valuation inputs and assumptions used in determining the fair value of our financial

instruments, including the extent to which we have relied on significant unobservable inputs to estimate fair value

and our process for corroborating these inputs, in “Note 18—Fair Value Measurement.”

Fair Value Measurement

We have a governance framework and a number of key controls that are intended to ensure that our fair value

measurements are appropriate and reliable. Our governance framework provides for independent oversight and

segregation of duties. Our control processes include review and approval of new transaction types, price verification and

review of valuation judgments, methods, models, process controls and results. Groups independent from our trading and

investing functions, including our Corporate Valuations Group (“CVG”), Fair Value Committee (“FVC”) and Model

Validation Group, participate in the review and validation process. The fair valuation governance process is set up in a

manner that allows the Chairperson of the FVC to escalate valuation disputes that cannot be resolved at the FVC to a

more senior committee called the Valuations Advisory Committee (“VAC”) for resolution. The VAC is chaired by the

Chief Financial Officer and includes other senior management. The VAC is only required to convene to review escalated

valuation disputes; however, it met once during 2014 for a general update on the valuation process.

47 Capital One Financial Corporation (COF)