Capital One 2014 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

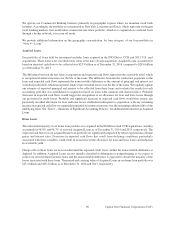

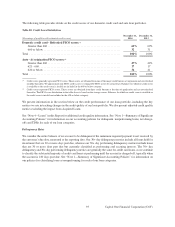

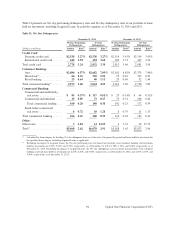

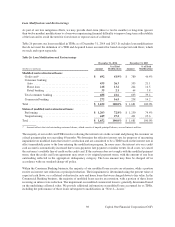

Impaired Loans

A loan is considered impaired when, based on current information and events, it is probable that we will be unable

to collect all amounts due from the borrower in accordance with the original contractual terms of the loan. Generally,

we report loans as impaired based on the method for measuring impairment in accordance with applicable accounting

guidance. Loans defined as individually impaired include larger balance commercial nonperforming loans and TDRs.

Loans held for sale are not reported as impaired, as these loans are recorded at lower of cost or fair value. Impaired

loans also exclude Acquired Loans accounted for based on expected cash flows because this accounting methodology

takes into consideration future credit losses expected to be incurred, as discussed above under “Summary of Selected

Financial Data.”

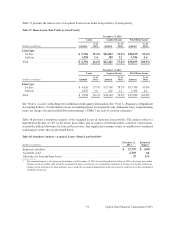

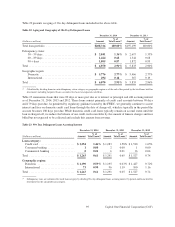

Impaired loans, including TDRs, totaled $1.9 billion as of both December 31, 2014 and 2013. TDRs accounted for

$1.7 billion of impaired loans as of both December 31, 2014 and 2013. We provide additional information on our

impaired loans, including the allowance for loan and lease losses established for these loans, in “Note 4—Loans”

and “Note 5—Allowance for Loan and Lease Losses.”

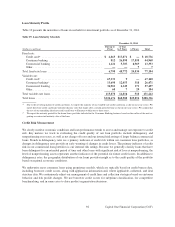

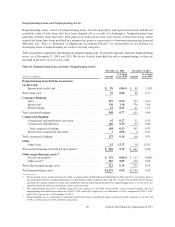

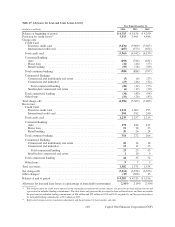

Allowance for Loan and Lease Losses

Our allowance for loan and lease losses represents management’s best estimate of incurred loan and lease credit

losses inherent in our held for investment portfolio as of each balance sheet date. The allowance for loan and lease

losses is increased through the provision for credit losses and reduced by net charge-offs. We provide additional

information on the methodologies and key assumptions used in determining our allowance for loan and lease losses

in “Note 1—Summary of Significant Accounting Policies.”

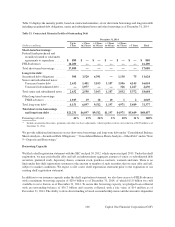

Our allowance for loan and lease losses increased by $68 million to $4.4 billion as of December 31, 2014, from

$4.3 billion as of December 31, 2013. The allowance coverage ratio declined to 2.10% as of December 31, 2014,

from 2.19% as of December 31, 2013. The increase in the allowance for loan and lease losses was primarily driven

by loan growth in our domestic card, auto and commercial loan portfolios, in addition to portfolio specific risks in

our commercial loan portfolio, offset by credit improvement driving allowance releases related to our international

card portfolio.

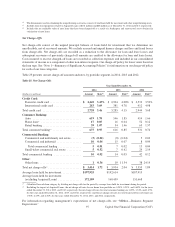

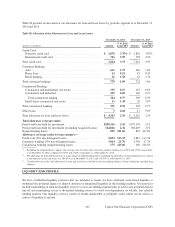

Table 27 presents changes in our allowance for loan and lease losses for 2014, 2013 and 2012, and details the

provision for credit losses recognized in our consolidated statements of income, and charge-offs and recoveries by

portfolio segment.

99 Capital One Financial Corporation (COF)