Capital One 2014 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

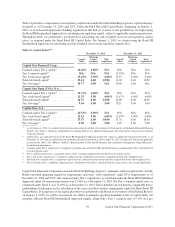

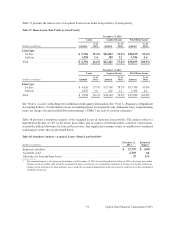

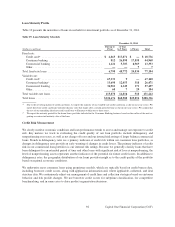

Dividend Policy and Stock Purchases

We paid common stock dividends of $0.30 per share in each quarter of 2014. We paid preferred stock dividends of

$15.00 per share on the outstanding shares of our 6.00% fixed-rate non-cumulative perpetual preferred stock, Series

B (the “Series B Preferred Stock”) in each quarter of 2014. We also paid preferred stock dividends of $13.7153 per

share and $15.625 per share in the third and fourth quarters of 2014, respectively, on the outstanding shares of Series

C Preferred Stock.

On January 29, 2015, our Board of Directors declared a quarterly dividend of $0.30 per share, payable on

February 20, 2015 and quarterly dividends on our Series B Preferred Stock, Series C Preferred Stock, and Series D

Preferred Stock payable on March 2, 2015. Based on these declarations, the Company will pay approximately $166

million in common equity dividends and approximately $32 million in total preferred dividends in the first quarter

of 2015.

The declaration and payment of dividends to our stockholders, as well as the amount thereof, are subject to the

discretion of our Board of Directors and depend upon our results of operations, financial condition, capital levels,

cash requirements, future prospects and other factors deemed relevant by the Board of Directors. As a bank holding

company, our ability to pay dividends is largely dependent upon the receipt of dividends or other payments from our

subsidiaries. Regulatory restrictions exist that limit the ability of the Banks to transfer funds to our bank holding

company. Funds available for dividend payments from COBNA and CONA were $1.6 billion and $281 million,

respectively, as of December 31, 2014. There can be no assurance that we will declare and pay any dividends to

stockholders.

The timing and exact amount of any future common stock repurchases will depend on various factors, including

market conditions, our capital position and amount of retained earnings. Our stock repurchase program does not

include specific price targets, may be executed through open market purchases or privately negotiated transactions,

including utilizing Rule 10b5-1 programs, and may be suspended at any time.

For additional information on dividends and stock repurchases, see “Part I—Item 1. Business—Supervision and

Regulation—Dividends, Stock Repurchases and Transfer of Funds.”

RISK MANAGEMENT

Risk Framework

We use a risk framework to provide an overall enterprise-wide approach for effectively managing risk. We execute

against our risk framework with the “Three Lines of Defense” risk management model to demonstrate and structure

the roles, responsibilities and accountabilities in the organization for taking and managing risk.

The “First Line of Defense” is comprised of the business areas that through their day-to-day business activities take

risk on our behalf. As the business owner, the first line is responsible for identifying, assessing, managing and

controlling that risk, and for mitigating our overall risk exposure. The first line formulates strategy and operates

within the risk appetite and framework. The “Second Line of Defense” provides oversight of first line risk taking

and management, and is comprised primarily of our Risk Management organization. The second line assists in

determining risk capacity, risk appetite, and the strategies, policies and structure for managing risks. The second

line owns the risk framework. The second line is both an ‘expert advisor’ to the first line and an ‘effective challenger’

of first line risk activities. The “Third Line of Defense” is comprised of our Internal Audit and Credit Review

functions. The third line provides independent and objective assurance to senior management and to the Board of

Directors that first and second line risk management and internal control systems and its governance processes are

well-designed and working as intended.

82 Capital One Financial Corporation (COF)