Capital One 2014 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

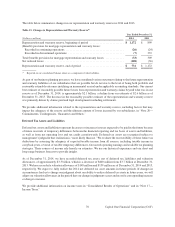

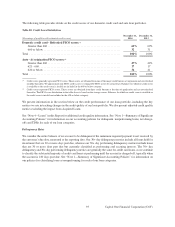

for evaluating the risk implications of credit strategy and for oversight of credit for both the existing portfolio and

any new credit investments. The Chief Consumer Credit Officer and the Chief Commercial Credit Officer have

formal approval authority for various types and levels of credit decisions, including individual commercial loan

transactions. Division Presidents within each segment are responsible for managing the credit risk within their

divisions and maintaining processes to control credit risk and comply with credit policies and guidelines. In addition,

the Chief Risk Officer establishes policies, delegates approval authority and monitors performance for non-loan

credit exposure entered into with financial counterparties or through the purchase of credit sensitive securities in

our investment portfolio.

Our credit policies establish standards in five areas: customer selection, underwriting, monitoring, remediation, and

portfolio management. The standards in each area provide a framework comprising specific objectives and control

processes. These standards are supported by detailed policies and procedures for each component of the credit

process. Starting with customer selection, our goal is to generally provide credit on terms that generate above hurdle

returns. We use a number of quantitative and qualitative factors to manage credit risk, including setting credit risk

limits and guidelines for each of our lines of business. We monitor performance relative to these guidelines and

report results and any required mitigating actions to appropriate senior management committees and our Board of

Directors.

Legal Risk Management

The General Counsel provides legal evaluation and guidance to the enterprise and business areas and partners with

other risk management functions such as Compliance and Internal Audit. This evaluation and guidance is based on

an assessment of the type and degree of legal risk associated with the internal business area practices and activities

and of the controls the business has in place to mitigate legal risks.

Liquidity Risk Management

We seek to mitigate liquidity risk strategically and tactically. From a strategic perspective, we have acquired and

built deposit gathering businesses and significantly reduced our loan to deposit ratio. From a tactical perspective,

we have accumulated a sizable liquidity reserve comprised of cash, high-quality, unencumbered securities, and

committed collateralized credit lines. We also continue to maintain access to the secured and unsecured markets

through ongoing issuance. This combination of stable and diversified funding sources and our stockpile of liquidity

reserves enables us to maintain confidence in our liquidity position.

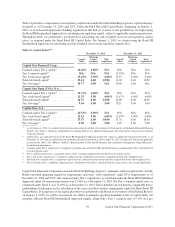

The Chief Risk Officer, in conjunction with the Chief Market and Liquidity Risk Officer, is responsible for the

establishment of liquidity risk management policies and standards for governance and monitoring of liquidity

risk at a corporate level. The Chief Financial Officer is accountable for the management of liquidity risk. We

assess liquidity strength by evaluating several different balance sheet metrics under severe stress scenarios to

ensure we can withstand significant funding degradation in both idiosyncratic, and market wide and combined

liquidity stress scenarios. Management reports liquidity metrics to appropriate senior management committees

and our Board of Directors no less than quarterly. We continuously monitor market and economic conditions to

evaluate emerging stress conditions with assessment and appropriate action plans in accordance with our

Contingency Funding Plan.

Market Risk Management

We recognize that interest rate and foreign exchange risk is inherent in the business of banking due to the nature of

the assets and liabilities of banks. Banks typically manage the trade-off between near-term earnings volatility and

market value volatility by targeting moderate levels of each. In addition to using industry accepted techniques to

analyze and measure interest rate and foreign exchange risk, we perform sensitivity analysis to identify our risk

86 Capital One Financial Corporation (COF)