Capital One 2014 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

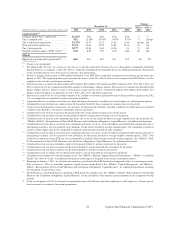

2014. In addition to seasonality, we continue to expect that loan growth will impact the charge-off rate. As new

loan balances season, we expect them to put upward pressure on losses. While this impact on the charge-off

rate will likely be modest at first, we expect that the impact will grow throughout 2015 and beyond. In addition

to rising charge-offs, we expect loan growth to drive allowance additions. We continue to believe that our

Domestic Card business continues to be well-positioned.

•Consumer Banking: In our Consumer Banking business, we continue to experience a change in product mix

as a result of continued growth in auto originations and loans offset by the planned run-off of our acquired

home loan portfolio. While our auto business remains well-positioned, we remain cautious and continue to

closely monitor pricing, underwriting practices, used vehicle prices and other competitor and market factors.

Returns on new auto originations are lower than returns in the overall auto loan portfolio, but remain resilient

and within ranges that support an attractive business. In addition, in our retail banking business, we expect

the impact of the prolonged low interest rate environment will continue to pressure returns, even if rates rise

in 2015.

•Commercial Banking: Our Commercial Banking business is well-positioned to navigate current market

conditions. Competition in the Commercial Banking business remains intense, pressuring margin and returns.

Although we expect the pace of our commercial loan portfolio growth to be slower in 2015, we expect our

Commercial Banking business to continue to deliver solid results.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in accordance with U.S. GAAP requires management to make a number of

judgments, estimates and assumptions that affect the amount of assets, liabilities, income and expenses on the

consolidated financial statements. Understanding our accounting policies and the extent to which we use management

judgment and estimates in applying these policies is integral to understanding our financial statements. We provide a

summary of our significant accounting policies under “Note 1—Summary of Significant Accounting Policies.”

We have identified the following accounting policies as critical because they require significant judgments and

assumptions about highly complex and inherently uncertain matters and the use of reasonably different estimates

and assumptions could have a material impact on our results of operations or financial condition. These critical

accounting policies govern:

• Loan loss reserves

• Asset impairment

• Fair value of financial instruments

• Representation and warranty reserves

• Customer rewards reserves

We evaluate our critical accounting estimates and judgments on an ongoing basis and update them, as necessary,

based on changing conditions. Management has discussed our critical accounting policies and estimates with the

Audit Committee of the Board of Directors.

Loan Loss Reserves

We maintain an allowance for loan and lease losses that represents management’s estimate of incurred loan and

lease losses inherent in our held-for-investment credit card, consumer banking and commercial banking loan

portfolios as of each balance sheet date. We also separately reserve for binding unfunded lending commitments,

letters of credit and financial guarantees.

43 Capital One Financial Corporation (COF)