Capital One 2014 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

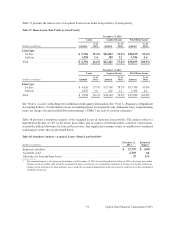

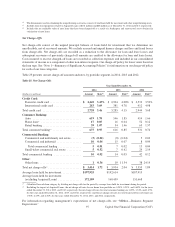

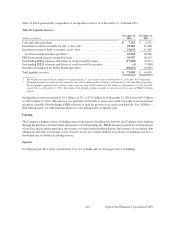

Loan Maturity Profile

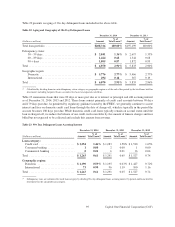

Table 19 presents the maturities of loans in our held-for-investment portfolio as of December 31, 2014.

Table 19: Loan Maturity Schedule

December 31, 2014

Due up to >1 Year

(Dollars in millions) 1 Year to 5 Years >5 Years Total

Fixed rate:

Credit card(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 4,865 $13,871 $ — $ 18,736

Consumer banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 812 26,598 17,558 44,968

Commercial banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,121 5,303 6,969 13,393

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —— 7 7

Total fixed-rate loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,798 45,772 24,534 77,104

Variable rate:

Credit card(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67,131 9 — 67,140

Consumer banking(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,698 12,455 318 26,471

Commercial banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34,981 2,345 171 37,497

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68 7 29 104

Total variable-rate loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115,878 14,816 518 131,212

Total loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $122,676 $60,588 $25,052 $208,316

(1) Due to the revolving nature of credit card loans, we report the majority of our variable-rate credit card loans as due in one year or less. We

report fixed-rate credit card loans with introductory rates that expire after a certain period of time as due in one year or less. We assume that

the rest of our remaining fixed-rate credit card loans will mature within one to three years.

(2) We report the maturity period for the home loans portfolio included in the Consumer Banking business based on the earlier of the next re-

pricing or contractual maturity date of the loan.

Credit Risk Measurement

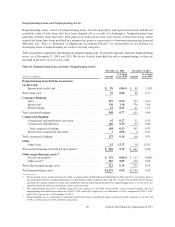

We closely monitor economic conditions and loan performance trends to assess and manage our exposure to credit

risk. Key metrics we track in evaluating the credit quality of our loan portfolio include delinquency and

nonperforming asset rates, as well as net charge-off rates and our internal risk ratings of larger balance commercial

loans. Trends in delinquency rates are a primary indicator of credit risk within our consumer loan portfolios, as

changes in delinquency rates provide an early warning of changes in credit losses. The primary indicator of credit

risk in our commercial loan portfolios is our internal risk ratings. Because we generally classify loans that have

been delinquent for an extended period of time and other loans with significant risk of loss as nonperforming, the

level of nonperforming assets represents another indicator of the potential for future credit losses. In addition to

delinquency rates, the geographic distribution of our loans provides insight as to the credit quality of the portfolio

based on regional economic conditions.

We underwrite most consumer loans using proprietary models, which are typically based on credit bureau data,

including borrower credit scores, along with application information and, where applicable, collateral, and deal

structure data. We continuously adjust our management of credit lines and collection strategies based on customer

behavior and risk profile changes. We use borrower credit scores for subprime classification, for competitive

benchmarking, and in some cases to drive product segmentation decisions.

92 Capital One Financial Corporation (COF)