Capital One 2014 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

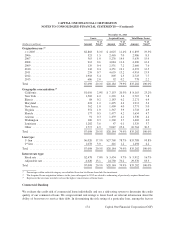

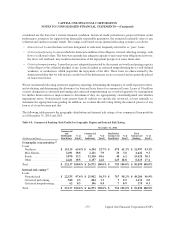

166

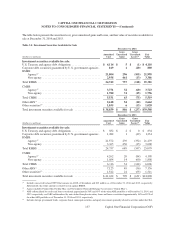

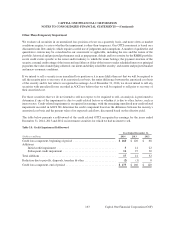

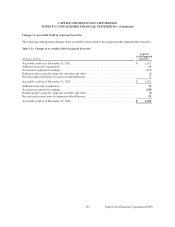

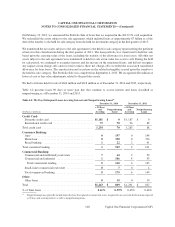

NOTE 4—LOANS

Loan Portfolio Composition

Our loan portfolio consists of loans held for investment, including restricted loans underlying our consolidated

securitization trusts, and loans held for sale, and is divided into three portfolio segments: credit card, consumer

banking and commercial banking loans. Credit card loans consist of domestic and international credit card loans.

Consumer banking loans consist of auto, home and retail banking loans. Commercial banking loans consist of

commercial and multifamily real estate, commercial and industrial and small-ticket commercial real estate loans.

Our portfolio of loans held for investment also includes loans acquired in the ING Direct, CCB and 2012 U.S. card

acquisitions. These loans were recorded at fair value at the date of each acquisition and are referred to as Acquired

Loans. The substantial majority of the loans purchased in the 2012 U.S. card acquisition had existing revolving

privileges; therefore, they were excluded from the Acquired Loans and accounted for based on contractual cash

flows at acquisition. See “Note 1—Summary of Significant Accounting Policies” for additional information on

accounting guidance for these loans.

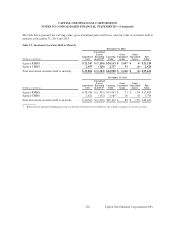

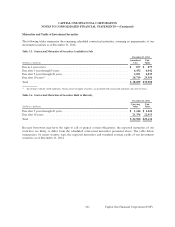

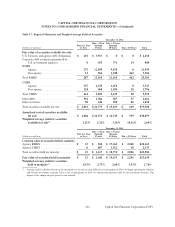

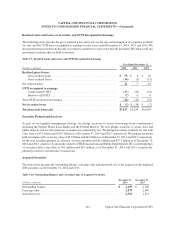

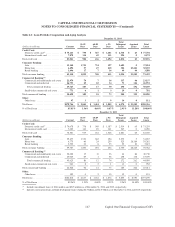

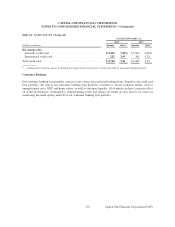

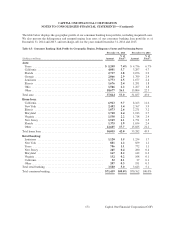

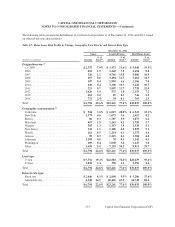

Credit Quality

We closely monitor economic conditions and loan performance trends to manage and evaluate our exposure to credit

risk. Trends in delinquency ratios are an indicator, among other considerations, of credit risk within our loan portfolio.

The level of nonperforming loans represents another indicator of the potential for future credit losses. Accordingly,

key metrics we track and use in evaluating the credit quality of our loan portfolio include delinquency and

nonperforming loan rates, as well as net charge-off rates and our internal risk ratings of larger balance commercial

loans. The table below presents the composition and an aging analysis of our loans held for investment portfolio,

which includes restricted loans for securitization investors, as of December 31, 2014 and 2013. The delinquency

aging includes all past due loans, both performing and nonperforming.

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Capital One Financial Corporation (COF)