Capital One 2014 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

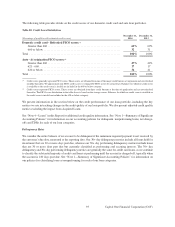

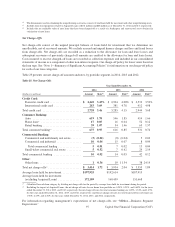

We operate our Commercial Banking business primarily in geographic regions where we maintain retail bank

branches. Accordingly, the portfolio is concentrated in New York, Louisiana and Texas, which represent our largest

retail banking markets. Our small ticket commercial real estate portfolio, which was originated on a national basis

through a broker network, is in a run-off mode.

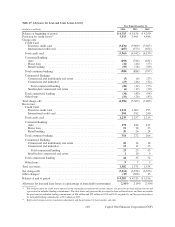

We provide additional information on the geographic concentration, by loan category, of our loan portfolio in

“Note 4—Loans.”

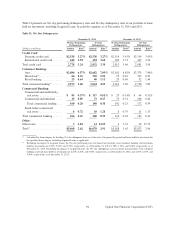

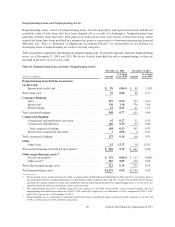

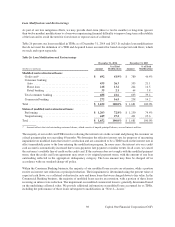

Acquired Loans

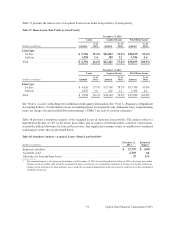

Our portfolio of loans held for investment includes loans acquired in the ING Direct, CCB and 2012 U.S. card

acquisitions. These loans were recorded at fair value at the date of each acquisition. Acquired Loans accounted for

based on expected cash flows to be collected was $23.5 billion as of December 31, 2014, compared to $28.6 billion

as of December 31, 2013.

The difference between the fair value at acquisition and expected cash flows represents the accretable yield, which

is recognized in interest income over the life of the loans. The difference between the contractual payments on the

loans and expected cash flows represents the nonaccretable difference or the amount of principal and interest not

considered collectible, which incorporates future expected credit losses over the life of the loans. We regularly update

our estimate of expected principal and interest to be collected from these loans and evaluate the results for each

accounting pool that was established at acquisition based on loans with common risk characteristics. Probable

decreases in expected cash flows would trigger the recognition of an allowance for loan and lease losses through

our provision for credit losses. Probable and significant increases in expected cash flows would first reverse any

previously recorded allowance for loan and lease losses established subsequent to acquisition, with any remaining

increase in expected cash flows recognized prospectively in interest income over the remaining estimated life of the

underlying loans. See “Note 1—Summary of Significant Accounting Policies” for additional information on Acquired

Loans.

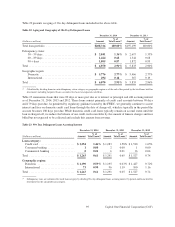

Home Loans

The substantial majority of our home loan portfolio was acquired in the ING Direct and CCB acquisitions, and they

accounted for 98.9% and 98.7% of our total Acquired Loans as of December 31, 2014 and 2013, respectively. The

expected cash flows for our acquired home loan portfolio are significantly impacted by future expectations of home

prices and interest rates. Decreases in expected cash flows that result from declining conditions, particularly

associated with these variables, could result in an increase in the allowance for loan and lease losses and reduction

in accretable yield.

Charge-offs on these loans are not recorded until the expected credit losses within the nonaccretable difference is

depleted. In addition, Acquired Loans are not initially classified as delinquent or nonperforming as we expect to

collect our net investment in these loans and the nonaccretable difference is expected to absorb the majority of the

losses associated with these loans. The period-end carrying value of Acquired Loans in our home loan portfolio was

$23.2 billion and $28.2 billion as of December 31, 2014 and 2013, respectively.

90 Capital One Financial Corporation (COF)