Capital One 2014 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

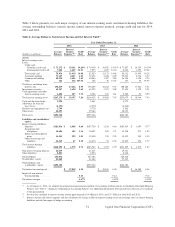

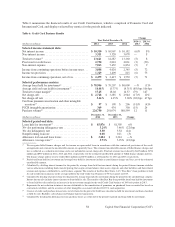

subsidiaries will depend on, among other things, actual future mortgage loan performance, the actual level of future

repurchase and indemnification requests, the actual success rates of claimants, developments in litigation, actual

recoveries on the collateral and macroeconomic conditions (including unemployment levels and housing prices).

As part of our business planning processes, we have considered various outcomes relating to the potential future

representation and warranty liabilities of our subsidiaries that are possible but do not rise to the level of being both

probable and reasonably estimable outcomes justifying an incremental accrual under applicable accounting standards.

Our current best estimate of reasonably possible future losses from representation and warranty claims beyond what

was in our reserve as of December 31, 2014 is approximately $2.1 billion, a decline from our estimate of $2.6 billion

as of December 31, 2013. Notwithstanding our ongoing attempts to estimate a reasonably possible amount of future

losses beyond our current accrual levels based on current information, it is possible that actual future losses will

exceed both the current accrual level and our current estimate of the amount of reasonably possible losses. This

estimate involves considerable judgment, and reflects that there is still significant uncertainty regarding the numerous

factors that may impact the ultimate loss levels, including, but not limited to, anticipated litigation outcomes, future

repurchase and indemnification claim levels, ultimate repurchase and indemnification rates, future mortgage loan

performance levels, actual recoveries on the collateral and macroeconomic conditions (including unemployment

levels and housing prices). In light of the significant uncertainty as to the ultimate liability our subsidiaries may

incur from these matters, an adverse outcome in one or more of these matters could be material to our results of

operations or cash flows for any particular reporting period. See “Note 20—Commitments, Contingencies,

Guarantees and Others” for additional information.

Customer Rewards Reserve

We offer products, primarily credit cards, which provide reward program members with various rewards, such as

cash, statement credits, gift cards, airline tickets or merchandise. The majority of our rewards do not expire and

there is no limit on the number of reward points an eligible card member can earn. Customer rewards costs, which

we generally record as an offset to interchange income, are driven by various factors, such as card member charge

volume, customer participation in the rewards program and contractual arrangements with redemption partners. We

establish a customer rewards reserve that reflects management’s judgment regarding rewards earned that are expected

to be redeemed and the estimated redemption cost.

We use financial models to estimate ultimate redemption rates of rewards earned to date by current card members

based on historical redemption trends, current enrollee redemption behavior, card product type, year of program

enrollment, enrollment tenure and card spend levels. Our current assumption is that the vast majority of all rewards

earned will eventually be redeemed. We use a weighted-average cost per reward redeemed during the previous twelve

months, adjusted as appropriate for recent changes in redemption costs, including mix of rewards redeemed, to

estimate future redemption costs. We continually evaluate our reserve and assumptions based on developments in

redemption patterns, cost per point redeemed, contract changes and other factors. Changes in the ultimate redemption

rate and weighted-average cost per point have the effect of either increasing or decreasing the reserve through the

current period provision by an amount estimated to cover the cost of all points previously earned but not yet

redeemed by card members as of the end of the reporting period. We recognized customer rewards expense of

$2.0 billion, $1.6 billion and $1.3 billion in 2014, 2013 and 2012, respectively. Our customer rewards liability, which

is included in other liabilities on our consolidated balance sheets, totaled $2.7 billion and $2.3 billion as of

December 31, 2014 and 2013, respectively.

49 Capital One Financial Corporation (COF)