Capital One 2014 Annual Report Download

Download and view the complete annual report

Please find the complete 2014 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

2014 ANNUAL REPORT

Table of contents

-

Page 1

2014 ANNUAL REPORT -

Page 2

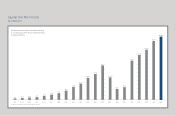

Capital One Net Income ($ in Millions) For two decades we've been committed to pursuing and sustaining long-term value and delivering strong ï¬nancial performance. $4,121 $4,428 ... 2008 2009 2010 2011 2012 2013 2014 * Excludes goodwill impairment charge of $811 million before income taxes -

Page 3

... earn the loyalty of our customers. Guided by these core principles and aided by more than a little good fortune, we've transformed ourselves from a credit card company into a diversiï¬ed bank with a strong and resilient balance sheet. We've achieved relevant scale in our card and auto businesses... -

Page 4

-

Page 5

... willing to invest to be at the forefront of banking. In 2014, Capital One delivered net income of $4.4 billion, a 7% increase from 2013. Our earnings per share were $7.59, up from $6.89 in 2013. Return on average tangible common equity was 15.8%, down from 2013, but still at the higher end of the... -

Page 6

...in 2014, with the net charge-off rate at 1.72%. Our balance sheet is strong. We have ample deposit funding and a great franchise, both in our branches and through Capital One 360 ®, our digital banking platform. Our common equity Tier 1 capital ratio was 12.5% at year-end. Our strong capital levels... -

Page 7

... practices, used vehicle prices, and other market factors. Returns on new originations are lower than returns in the overall auto loan portfolio, but remain resilient and above hurdle. In our retail deposit business, we continue to grow primary banking relationships and manage costs, although... -

Page 8

... and acquiring the digital talent of a great technology company. We are well positioned to succeed as a digital leader. experiences. Digital isn't a channel. It's a way of life. At Capital One, we are deeply embedding technology, data, design, and software development into how we work. Most... -

Page 9

... real time what delights or frustrates customers and to put those insights into action in the products and experiences we deliver. In 2014, we acquired Adaptive Path, a legendary San Francisco-based pioneer in UX design and orchestrating end-to-end service experiences. This acquisition brings world... -

Page 10

... and expanded a number of new features. Partnering with Apple, we were one of only a handful of banks to be included in the launch of Apple Pay â„¢. We also introduced Capital One Wallet and Apple Pay With Apple Pay, our customers can easily and securely use mobile devices to make purchases at many... -

Page 11

... thing to do for our customers, and it's how we are building an enduring customer franchise. We are committed to providing customers with loans and credit lines that ï¬t their ability to pay. Our free payment alerts and automatic payment options help customers manage their money. We make policy... -

Page 12

..., and business owners plan, save, and invest for tomorrow. Our associates are strikingly generous with their talents and their time. In 2014, Capital One associates spent more than 360,000 hours in volunteer service, working in hundreds of community and charitable programs. The company gave $46... -

Page 13

... years, we plan to invest $150 million in community grants and initiatives to train people for the jobs of today and tomorrow, spur small business development, and provide money management resources to prepare people for future economic success. By helping individuals and families access the digital... -

Page 14

... a registered trademark of Cable News Network. A Time Warner Company and is used under license. FORTUNE, CNN and Time Inc. are not afï¬liated with, and do not endorse products or services of, Licensee. Copyright © 2015 Working Mother Media. All rights reserved. Used by permission and protected by... -

Page 15

... work remains and there are no guarantees. But I wouldn't trade places with anyone. Together with the great people of Capital One, I look forward to continuing our quest to change banking for good and along the way build one of America's great companies. Richard D. Fairbank Chair, Chief Executive... -

Page 16

Financial Summary Diluted Earnings Per Share From Continuing Operations $6.64 $6.99 $7.28 $6.49 $7.58 $0.74 2009 2010 2011 2012 2013 2014 Diluted Earnings Per Share $7.59 $6.76 $5.97 $6.11 $6.89 $0.98 2009 2010 2011 2012 2013 2014 Deposits ($ in Billions) $212 $205 $206 $116 $122... -

Page 17

...Average Balances: Loans held for investment Interest-earning assets Total assets Interest-bearing deposits Total deposits Borrowings Common equity Total stockholders' equity $ $ Credit Quality Metrics: Allowance for loan and lease losses Allowance as a % of loans held for investment Net charge-offs... -

Page 18

... Senior Advisor, Managing Director and Vice Chairman for Retail Banking Morgan Stanley & Co. John G. Finneran, Jr. General Counsel and Corporate Secretary Frank G. LaPrade, III Chief Enterprise Services Officer and Chief of Staff to the CEO Pierre E. Leroy R Former Executive Chairman Vigilant... -

Page 19

...) 1680 Capital One Drive, McLean, Virginia (Address of Principal Executive Offices) Registrant's telephone number, including area code: (703) 720-1000 Securities registered pursuant to section 12(b) of the act: Title of Each Class Name of Each Exchange on Which Registered Common Stock (par value... -

Page 20

...Issuer Purchases of Equity Securities ...Summary of Selected Financial Data ...Management's Discussion and Analysis of Financial Condition and Results of Operations ("MD&A") ...Executive Summary and Business Outlook ...Critical Accounting Policies and Estimates ...Accounting Changes and Developments... -

Page 21

... ...Directors, Executive Officers and Corporate Governance ...Executive Compensation ...Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters ...Certain Relationships and Related Transactions and Director Independence ...Principal Accountant Fees and Services... -

Page 22

...8 Commercial Banking Business Results ...68 9 Other Results ...71 10 Investment Securities ...73 11 Non-Agency Investment Securities Credit Ratings ...74 12 Loans Held for Investment ...74 13 Changes in Representation and Warranty Reserve ...76 14 Capital Ratios ...79 15 Estimated Common Equity Tier... -

Page 23

...with the Consolidated Financial Statements included in this Report. As one of the nation's ten largest banks based on deposits as of December 31, 2014, we service banking customer accounts through the internet and branch locations across New York, Louisiana, Texas, Maryland, Virginia, New Jersey and... -

Page 24

... the U.S. Securities and Exchange Commission ("SEC"). OPERATIONS AND BUSINESS SEGMENTS Our consolidated total net revenues are derived primarily from lending to consumer and commercial customers net of funding costs associated with deposits, short-term borrowings and long-term debt. We also earn non... -

Page 25

... fiscal years. Delinquency rates in our Credit Card and Consumer Banking businesses also have historically exhibited seasonal patterns, with delinquency rates generally tending to decrease in the first two quarters of the year as customers use income tax refunds to pay down outstanding loan balances... -

Page 26

... and related changes to Regulation Z, impose a number of restrictions on credit card practices impacting rates and fees, require that a consumer's ability to pay be taken into account before issuing credit or increasing credit limits, and update the disclosures required for open-end credit. Mortgage... -

Page 27

... fee rules and our debit card business. Bank Secrecy Act and USA PATRIOT Act of 2001 The Bank Secrecy Act and the USA PATRIOT Act of 2001 (the "Patriot Act") require financial institutions, among other things, to implement a risk-based program reasonably designed to prevent money laundering... -

Page 28

... sales and trading practices, public offerings, publication of research reports, use and safekeeping of client funds and securities, capital structure, record-keeping and the conduct of directors, officers and employees. Capital One Asset Management LLC, which provides investment advice to customers... -

Page 29

... 2014, the Basel Committee made changes to the leverage ratio rules to account for differences in national accounting frameworks. The Federal Banking Agencies issued a rule in July 2013 implementing the Basel III capital framework developed by the Basel Committee as well as certain Dodd-Frank Act... -

Page 30

... to calculate total leverage exposure using daily averages for on-balance sheet items and the average of three month-end calculations for off-balance sheet items. The supplementary leverage ratio will become effective January 1, 2018. For information regarding our expectations of how the Final Rule... -

Page 31

... regarding resolution planning applicable to the Banks. In addition, in October 2012, the Federal Reserve issued a rule that implements the requirement in the Dodd-Frank Act that the Federal Reserve conduct annual stress tests on the capacity of our capital to absorb losses as a result of adverse... -

Page 32

...bank and nonbank acquisitions and mergers and affiliate transactions. The Dodd-Frank Act also includes provisions related to corporate governance and executive compensation and new fees and assessments, among others. The federal agencies have significant discretion in drafting the implementing rules... -

Page 33

..., the Virginia Bureau of Financial Institutions. Dividends, Stock Repurchases and Transfers of Funds In November 2011, the Federal Reserve finalized capital planning rules applicable to large bank holding companies like us (commonly referred to as Comprehensive Capital Analysis and Review or "CCAR... -

Page 34

... dividends on our stock, make payments on corporate debt securities and meet our other obligations. There are various federal law limitations on the extent to which the Banks can finance or otherwise supply funds to us through dividends and loans. These limitations include minimum regulatory capital... -

Page 35

... Ombudsman Service. COEP continues to deliver on its remediation plan in relation to PPI complaints. COEP is a party to the Card Protection Plan Limited ("CPP") redress scheme which enables customers who bought card protection insurance with CPP to seek compensation. In January 2014 the redress... -

Page 36

... limit, reward programs and other product features. Our Consumer Banking and Commercial Banking businesses compete with national and state banks and direct banks for deposits, commercial and auto loans, mortgages and trust accounts and with savings and loan associations and credit unions for loans... -

Page 37

... to): Total System Services Inc. ("TSYS") for processing services for our North American and U.K. portfolios of consumer and small business credit card accounts, and Fidelity Information Services ("FIS") for the Capital One banking systems. To protect our systems and technologies, we employ security... -

Page 38

...and reporting standards; developments, changes or actions relating to any litigation matter involving us; the inability to sustain revenue and earnings growth; increases or decreases in interest rates; our ability to access the capital markets at attractive rates and terms to capitalize and fund our... -

Page 39

... looking statements include: Changes In The Macroeconomic Environment May Adversely Affect Our Industry, Business, Results Of Operations And Financial Condition. We offer a broad array of financial products and services to consumers, small businesses and commercial clients. We market our credit card... -

Page 40

... our access to funding. The interest rates that we pay on the securities we have issued are also influenced by, among other things, applicable credit ratings from recognized rating agencies. A downgrade to any of these credit ratings could affect our ability to access the capital markets, increase... -

Page 41

... capital, liquidity, risk management, single-counterparty credit exposure limits, early remediation, and resolution planning), enhanced supervision (including stress testing), prohibitions on proprietary trading and investments in covered funds (referred to as the "Volcker Rule") and increased... -

Page 42

... several years, state and federal regulators have focused on compliance with the Bank Secrecy Act and anti-money laundering laws, data integrity and security, use of service providers, fair lending and other consumer protection issues. Any future changes to our business practices, including our debt... -

Page 43

... the remaining balance from our customers. Decreases in real estate values adversely affect the collateral value for our commercial lending and Home Loan activities, while the auto business is similarly exposed to collateral risks arising from the auction markets that determine used car prices... -

Page 44

...current financial plans. These new requirements could have a negative impact on our ability to lend, grow deposit balances or make acquisitions and limit our ability to make capital distributions in the form of dividends or share repurchases. Higher capital levels also lower our return on equity. In... -

Page 45

... management standards, conduct internal liquidity stress tests, and maintain a 30-day buffer of highly liquid assets to cover cash-flow needs under stressed conditions, in each case consistent with the requirements of the rule. Under the Federal Reserve's Capital Plan Rule, bank holding companies... -

Page 46

...a final rule regarding the Capital Plan and Stress Test Rules that, among other things, limits the ability of a bank holding company with $50 billion or more in total consolidated assets to make capital distributions under the capital plan rule if the bank holding company's net capital issuances are... -

Page 47

...our expenses. Further, as our business develops, changes or expands, additional expenses can arise as a result of a reevaluation of business strategies, management of outsourced services, asset purchases or other acquisitions, structural reorganization, compliance with new laws or regulations or the... -

Page 48

... credit card and other loan portfolios. Any merger, acquisition or strategic partnership we undertake will entail certain risks, which may materially and adversely affect our results of operations. If we experience greater than anticipated costs to integrate acquired businesses into our 26 Capital... -

Page 49

... amount of future loan losses in any target or partner company's portfolio; the amount of goodwill and intangibles that will result from any merger, acquisition or strategic partnership; certain purchase accounting adjustments that we expect will be recorded in our financial statements in connection... -

Page 50

... both in making loans and attracting deposits. We compete on the basis of the rates we pay on deposits and the rates and other terms we charge on the loans we originate or purchase, as well as the quality of our customer service and experience. Price competition for loans might result in origination... -

Page 51

... access to banking services at reduced costs, it also presents significant risks and we face strong competition in the direct banking market. Aggressive pricing throughout the industry may adversely affect the retention of existing balances and the cost-efficient acquisition of new deposit funds... -

Page 52

... of the capital markets. Changes in interest rates or in valuations in the debt or equity markets could directly impact us. For example, we borrow money from other institutions and depositors, which we use to make loans to customers and invest in debt securities and other earning assets. We... -

Page 53

... common stock, make payments on corporate debt securities and meet other obligations. There are various federal law limitations on the extent to which the Banks can finance or otherwise supply funds to us through dividends and loans. These limitations include minimum regulatory capital requirements... -

Page 54

...rating agency downgrade or default risk. In addition, we routinely execute transactions with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks, mutual and hedge funds and other institutional clients, resulting in a significant credit... -

Page 55

... I-Item 1. Business- Supervision and Regulation-Dividends, Stock Repurchases and Transfers of Funds," "MD&A-Capital Management-Dividend Policy and Stock Purchases," and "Note 12-Regulatory and Capital Adequacy." Securities Authorized for Issuance Under Equity Compensation Plans Information relating... -

Page 56

.... Comparison of 5-Year Cummulative Total Return (Capital One, S&P 500 Index and S&P Financial Index) $250 $225 $200 $185 $172 $150 $100 $50 $0 2009 2010 Capital One 2011 S&P 500 Index 2012 2013 S&P Financial Index December 31, 2009 2010 2011 2012 2013 2014 2014 Capital One ...S&P 500 Index... -

Page 57

... date. • • We use the term "Acquired Loans" to refer to the substantial majority of consumer and commercial loans acquired in the ING Direct and CCB acquisitions, and a limited portion of the credit card loans acquired in the 2012 U.S. card acquisition, which were recorded at fair value... -

Page 58

Five-Year Summary of Selected Financial Data(1) Change Year Ended December 31, (Dollars in millions, except per share data and as noted) 2014 2013 2012 2011 2010 2014 vs. 2013 vs. 2013 2012 Income statement Interest income ...Interest expense ...Net interest income ...Non-interest income(2) ... -

Page 59

... per share data as noted) 2014 2013 2012 2011 2010 2014 vs. 2013 vs. 2013 2012 Balance sheet (period end) Loans held for investment ...Interest-earning assets ...Total assets ...Interest-bearing deposits ...Total deposits ...Borrowings ...Common equity ...Total stockholders' equity ... $ 208... -

Page 60

... excess of the fair value of the net assets acquired from ING Direct as of the acquisition date over the consideration transferred. (3) Total net revenue was reduced by $645 million, $796 million, $937 million, $371 million and $950 million in 2014, 2013, 2012, 2011, and 2010, respectively, for the... -

Page 61

... audited consolidated financial statements as of and for the year ended December 31, 2014 and accompanying notes. MD&A is organized in the following sections Executive Summary and Business Outlook Critical Accounting Policies and Estimates Accounting Changes and Developments Consolidated Results of... -

Page 62

... credit card and commercial loan portfolios, and continued strong auto loan originations outpacing the run-off of the acquired home loan portfolio in our Consumer Banking business. Net Charge-off and Delinquency Statistics: Our net charge-off rate decreased by 32 basis points to 1.72% in 2014 from... -

Page 63

... to compression in deposit spreads in retail banking, declining home loan portfolio balances and margin compression in our auto loan portfolio. The decrease was partially offset by higher net interest income generated by growth in our auto loan portfolio. Period-end loans held for investment in our... -

Page 64

... 2014 Stock Repurchase Program does not include specific price targets, may be executed through open market purchases or privately negotiated transactions, including utilizing Rule 10b5-1 programs, and may be suspended at any time. See "MD&A- Capital Management-Capital Planning and Regulatory Stress... -

Page 65

... of our commercial loan portfolio growth to be slower in 2015, we expect our Commercial Banking business to continue to deliver solid results. • CRITICAL ACCOUNTING POLICIES AND ESTIMATES The preparation of financial statements in accordance with U.S. GAAP requires management to make a number of... -

Page 66

... value of collateral underlying secured loans, account seasoning, changes in our credit evaluation, underwriting and collection management policies, seasonality, general economic conditions, changes in the legal and regulatory environment and uncertainties in forecasting and modeling techniques used... -

Page 67

... value of the net assets acquired and liabilities assumed as of the acquisition date. Goodwill totaled $14.0 billion as of both December 31, 2014 and 2013. Intangible assets, which we report on our consolidated balance sheets as a component of other assets, consist primarily of purchased credit card... -

Page 68

.... Cash flows are adjusted, as necessary, in order to maintain each reporting unit's equity capital requirements. Our discounted cash flow analysis requires management to make judgments about future loan and deposit growth, revenue growth, credit losses, and capital rates. Discount rates used in 2014... -

Page 69

...to estimate fair value. Changes in market conditions, such as reduced liquidity in the capital markets or changes in secondary market activities, may reduce the availability and reliability of quoted prices or observable data used to determine fair value. We have developed policies and procedures to... -

Page 70

... and warranties about, among other things, the ownership of the loan, the validity of the lien securing the loan, the loan's compliance with any applicable loan criteria established by the purchaser, including underwriting guidelines and the ongoing existence of mortgage insurance, and the loan... -

Page 71

... a customer rewards reserve that reflects management's judgment regarding rewards earned that are expected to be redeemed and the estimated redemption cost. We use financial models to estimate ultimate redemption rates of rewards earned to date by current card members based on historical redemption... -

Page 72

... under the equity method and the passive losses related to the investments were recognized within non-interest expense. We adopted this guidance as of January 1, 2014 with retrospective application. See "Note 1-Summary of Significant Accounting Policies" for more information. CONSOLIDATED RESULTS OF... -

Page 73

... Yield/ Rate (Dollars in millions) Assets: Interest-earning assets: Loans: Credit card: Domestic credit card ...International credit card . Total credit card ...Consumer banking ...Commercial banking ...Other ...Total loans, including loans held for sale ...Investment securities ...Cash equivalents... -

Page 74

... investment securities from the ING Direct acquisition and the addition of loans from the 2012 U.S. card acquisition. Growth in average interest-earning assets was also driven by continued strong growth in commercial and auto loans, which was partially offset by the run-off of our acquired home loan... -

Page 75

... Income(1) 2014 vs. 2013 (Dollars in millions) Total Variance Volume Rate 2013 vs. 2012 Total Variance Volume Rate Interest income: Loans: Credit card ...Consumer banking ...Commercial banking ...Other ...Total loans, including loans held for sale ...Investment securities ...Cash equivalents and... -

Page 76

... impact of increased customer related fees and interchange fees from purchase volume growth, due in part to the acquisitions, fee based products and services revenue, a change to a benefit from a provision for mortgage representation and warranty losses and a reduction in fair value losses on... -

Page 77

...of non-interest expense for 2014, 2013 and 2012. Table 5: Non-Interest Expense(1)(2) Year Ended December 31, (Dollars in millions) 2014 2013 2012 Salaries and associate benefits ...Occupancy and equipment ...Marketing ...Professional services ...Communications and data processing ...Amortization of... -

Page 78

... for the non-taxable bargain purchase gain of $594 million related to the acquisition of ING Direct, a deferred tax benefit for changes in our state tax position resulting from the 2012 U.S. card acquisition and consolidation of ING Bank, fsb with our existing banking operations, and the resolution... -

Page 79

...on a matched maturity method that takes into consideration market rates. Our funds transfer pricing process provides a funds credit for sources of funds, such as deposits generated by our Consumer Banking and Commercial Banking businesses, and a funds charge for the use of funds by each segment. The... -

Page 80

... comprised of Domestic Card and International Card, and displays selected key metrics for the periods indicated. Table 6: Credit Card Business Results Change Year Ended December 31, (Dollars in millions) 2014 2013 2012 2014 vs. 2013 vs. 2013 2012 Selected income statement data: Net interest income... -

Page 81

...the second quarter of 2012 to establish the finance charge and fee reserve for the loans acquired in the 2012 U.S card acquisition. The higher average yield on loans held for investment was driven largely by the transfer of the Best Buy loan portfolio to the loans held for sale category in the first... -

Page 82

... run-off of our installment loan portfolio and certain other credit card loans acquired in the 2012 U.S. card acquisition, partially offset by growth in certain other credit card segments. Net Charge-off and Delinquency Statistics: Our net charge-off rate increased to 4.15% in 2013, compared... -

Page 83

... indicated. Table 6.1: Domestic Card Business Results Change Year Ended December 31, (Dollars in millions) 2014 2013 2012 2014 vs. 2013 vs. 2013 2012 Selected income statement data: Net interest income ...Non-interest income ...Total net revenue(1) ...Provision for credit losses ...Non-interest... -

Page 84

...for investment driven largely by the transfer of the Best Buy loan portfolio to the held for sale category in the first quarter of 2013, as well as the absence of the charge recorded in the second quarter of 2012 to establish the finance charge and fee reserve for the acquired credit card loans; (ii... -

Page 85

... indicated. Table 6.2: International Card Business Results Change Year Ended December 31, (Dollars in millions) 2014 2013 2012 2014 vs. 2013 vs. 2013 2012 Selected income statement data: Net interest income ...Non-interest income ...Total net revenue ...Provision for credit losses ...Non-interest... -

Page 86

... indicated. Table 7: Consumer Banking Business Results Change Year Ended December 31, (Dollars in millions) 2014 2013 2012 2014 vs. 2013 vs. 2013 2012 Selected income statement data: Net interest income ...Non-interest income ...Total net revenue ...Provision for credit losses ...Non-interest... -

Page 87

...Loans in our consumer banking loan portfolio with carrying values of $23.3 billion and $28.2 billion as of December 31, 2014 and 2013, respectively. Calculation of ratio adjusted to exclude the impact from Acquired Loans. See Credit Risk Profile and "Note 1-Summary of Significant Accounting Policies... -

Page 88

... in 2013. The decrease was largely due to the absence of ING Direct acquisition-related costs and other one-time items incurred in 2012, which were partially offset by increased expenses related to the growth in our auto loan portfolio. • • • 66 Capital One Financial Corporation (COF) -

Page 89

... Banking business are net interest income from loans and deposits and non-interest income from customer fees and related transactions. Because we have some investments that generate tax-exempt income or tax credits, we make certain reclassifications to our Commercial Banking business results... -

Page 90

.... Table 8: Commercial Banking Business Results(1) Change Year Ended December 31, (Dollars in millions) 2014 2013 2012 2014 vs. 2013 2013 vs. 2012 Selected income statement data: Net interest income ...Non-interest income ...Total net revenue(2) ...Provision (benefit) for credit losses ...Non... -

Page 91

... by period-end loans held for investment. (7) Represents our portfolio of loans serviced for third parties related to the Beech Street business. Key factors affecting the results of our Commercial Banking business for 2014, compared to 2013, and changes in financial condition and credit performance... -

Page 92

..., gains and losses on our investment securities portfolio and certain trading activities. Other also includes foreign exchange-rate fluctuations on foreign currency-denominated transactions; certain gains and losses on the sale and securitization of loans; unallocated corporate expenses that do not... -

Page 93

... indicated. Table 9: Other Results(1) Change Year Ended December 31, (Dollars in millions) 2014 2013 2012 2014 vs. 2013 2013 vs. 2012 Selected income statement data: Net interest income (expense)(2) ...Non-interest income ...Total net revenue (loss) ...Benefit for credit losses ...Non-interest... -

Page 94

...31, 2014, $206 million was related to securities that had been in a loss position for more than 12 months. We provide information on OTTI recognized in earnings on our investment securities above in "Consolidated Results of Operations-Non-Interest Income." 72 Capital One Financial Corporation (COF... -

Page 95

... as of December 31, 2014, and 2013, respectively. Includes foreign government bonds, corporate securities, municipal securities and equity investments primarily related to activities under the Community Reinvestment Act ("CRA"). Credit Ratings Our portfolio of investment securities continues to be... -

Page 96

...Credit Card business, and strong auto loan originations outpacing the run-off of our acquired home loan portfolio in our Consumer Banking business. We provide additional information on the composition of our loan portfolio and credit quality below in "Credit Risk Profile," "MD&A-Consolidated Results... -

Page 97

... result of our continued focus on deepening deposit relationships with existing customers and our continued marketing strategy to attract new business. We provide information on the composition of our deposits, average outstanding balances, interest expense and yield below in "Liquidity Risk Profile... -

Page 98

... ...Representation and warranty reserve, end of period ...$ (1) $ 899 (24) 333 309 (36) (33) (408) 731 $ 1,172 Reported on our consolidated balance sheets as a component of other liabilities. As part of our business planning processes, we have considered various outcomes relating to the future... -

Page 99

... internal risk-based capital assessments such as internal stress testing and economic capital. The level and composition of our capital may also be influenced by rating agency guidelines, subsidiary capital requirements, the business environment, conditions in the financial markets and assessments... -

Page 100

...II-Item 6. Summary of Selected Financial Data." While the TCE ratio is a capital measure widely used by investors, analysts, rating agencies, and bank regulatory agencies to assess the capital position of financial services companies, it may not be comparable to similarly titled measures reported by... -

Page 101

... the proportional amortization method of accounting for Investments in Qualified Affordable Housing Projects. See "Note 1-Summary of Significant Accounting Policies" for additional information. Prior periods have been recast to conform to this presentation. Capital ratios are calculated based on the... -

Page 102

... investment securities included in AOCI and adjustments related to intangibles. The inclusion of AOCI and the adjustments related to intangibles are phased-in at 20% for 2014, 40% for 2015, 60% for 2016, 80% for 2017 and 100% for 2018. The following table compares our common equity Tier 1 capital... -

Page 103

... our minimum required regulatory capital ratios. Capital Planning and Regulatory Stress Testing In November 2011, the Federal Reserve finalized capital planning rules applicable to large bank holding companies like us. Under these rules, bank holding companies with consolidated assets of $50 billion... -

Page 104

..., may be executed through open market purchases or privately negotiated transactions, including utilizing Rule 10b5-1 programs, and may be suspended at any time. For additional information on dividends and stock repurchases, see "Part I-Item 1. Business-Supervision and Regulation-Dividends, Stock... -

Page 105

... risks facing the organization and to enable Board of Directors engagement when needed. Calculate and Allocate Capital in Alignment with Risk Management and Measurement Processes (including Stress Testing) Capital is held to protect the Company from unforeseen risks or unexpected risk severity. As... -

Page 106

... in pursuit of our corporate business objectives. The Board of Directors approves our risk appetite including specific risk limits where applicable. While first line executives manage risk on a day-to-day basis, the Chief Risk Officer provides effective challenge and independent oversight to ensure... -

Page 107

...compliance reporting to senior business leaders, the executive committee and the Board of Directors. The Chief Compliance Officer is responsible for establishing and overseeing our Compliance Risk Management Program. Business areas incorporate compliance requirements and controls into their business... -

Page 108

... monitor market and economic conditions to evaluate emerging stress conditions with assessment and appropriate action plans in accordance with our Contingency Funding Plan. Market Risk Management We recognize that interest rate and foreign exchange risk is inherent in the business of banking due... -

Page 109

... by balance sheet interest rate risk, centrally and establish quantitative limits to control our exposure. Market risk is inherent in the financial instruments associated with our business operations and activities, including loans, deposits, securities, short-term borrowings, long-term debt and... -

Page 110

...sell charged-off credit card loans. Auto: We originate both prime and subprime auto loans. Customers are acquired through a network of auto dealers and direct marketing. Our auto loans generally have fixed interest rates and loan terms of 72 months or less. Loan size limits are customized by program... -

Page 111

... of the ING Direct portfolio that comprises the majority of our home loans. Retail banking includes small business loans and other consumer lending products originated through our branch network with a concentration in Louisiana, New York, Texas, New Jersey, Maryland, Virginia and California... -

Page 112

...our loan portfolio in "Note 4-Loans." Acquired Loans Our portfolio of loans held for investment includes loans acquired in the ING Direct, CCB and 2012 U.S. card acquisitions. These loans were recorded at fair value at the date of each acquisition. Acquired Loans accounted for based on expected cash... -

Page 113

... 18: Sensitivity Analysis-Acquired Loans-Home Loan Portfolio(1) (Dollars in millions) December 31, 2014 Estimated Impact Expected cash flows ...$ Accretable yield ...Allowance for loan and lease losses ...(1) 27,797 4,583 27 $ (109) 66 176 The estimated impact is the change in the balance as of... -

Page 114

...on credit bureau data, including borrower credit scores, along with application information and, where applicable, collateral, and deal structure data. We continuously adjust our management of credit lines and collection strategies based on customer behavior and risk profile changes. We use borrower... -

Page 115

... we use in tracking changes in the credit quality of our loan portfolio. We also present adjusted credit quality metrics excluding the impact from Acquired Loans. See "Note 4-Loans" in this Report for additional credit quality information. See "Note 1-Summary of Significant Accounting Policies" for... -

Page 116

... Rate(1) (Dollars in millions) Amount Rate(1) Credit Card: Domestic credit card ...International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan(2) ...Retail banking ...Total consumer banking(2) ...Commercial Banking: Commercial and multifamily real estate ...Commercial... -

Page 117

... 5,833 100.00% 1.33% 0.68 0.95 2.96% 2.77% 0.19 2.96% $ $ $ $ $ $ Calculated by dividing loans in each delinquency status category or geographic region as of the end of the period by the total loans held for investment, including Acquired Loans accounted for based on expected cash flows. Table... -

Page 118

... 31, 2014 % of Total Amount Loans HFI December 31, 2013 % of Total Amount Loans HFI (Dollars in millions) Nonperforming loans held for investment: Credit Card: International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan(2) ...Retail banking ...Total consumer banking... -

Page 119

... 2014, 2013 and 2012. Table 25: Net Charge-Offs Year Ended December 31, 2014 (Dollars in millions) Amount Rate(1) 2013 Amount Rate(1) 2012 Amount Rate(1) Credit Card: Domestic credit card ...$ International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan(2) ...Retail banking... -

Page 120

... 31, 2014 % of Total Amount Modifications December 31, 2013 % of Total Amount Modifications (Dollars in millions) Modified and restructured loans: Credit card(1) ...Consumer banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial banking ...Total ...Status of modified... -

Page 121

... card portfolio. Table 27 presents changes in our allowance for loan and lease losses for 2014, 2013 and 2012, and details the provision for credit losses recognized in our consolidated statements of income, and charge-offs and recoveries by portfolio segment. 99 Capital One Financial Corporation... -

Page 122

... Activity Year Ended December 31, (Dollars in millions) 2014 2013 2012 Balance at beginning of period ...Provision for credit losses(1) ...Charge-offs: Credit Card: Domestic credit card ...International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking... -

Page 123

...31, 2014 (Dollars in millions) Amount % of Total Loans HFI December 31, 2013 Amount % of Total Loans HFI Credit Card: Domestic credit card ...International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan(1) ...Retail banking ...Total consumer banking(1) ...Commercial Banking... -

Page 124

...Reserves (Dollars in millions) December 31, 2014 December 31, 2013 Cash and cash equivalents ...Investment securities available for sale, at fair value ...Investment securities held to maturity, at fair value ...Total investment securities portfolio(1)(2) ...FHLB borrowing capacity secured by loans... -

Page 125

... 2012. Table 30: Deposit Composition and Average Deposit Rates December 31, 2014 Period End Balance Average Balance Interest Expense % of Average Deposit Average Deposits Rate (Dollars in millions) Non-interest bearing accounts ...Interest-bearing checking accounts(1) ...Saving deposits(2) ...Time... -

Page 126

... maturity of one year or less and do not include the current portion of long-term debt. The short-term borrowings, which consist of federal funds purchased and securities loaned or sold under agreements to repurchase, and short-term FHLB advances, increased by $865 million in 2014, to $17.1 billion... -

Page 127

...32: Short-Term Borrowings Year Ended December 31, 2014 Average Balance Average Interest Rate 2013 Average Balance Average Interest Rate 2012 Average Balance Average Interest Rate (Dollars in millions) Federal funds purchased and repurchase agreements ...FHLB advances ...Total short-term borrowings... -

Page 128

... debt securities, preferred stock, depositary shares, common stock, purchase contracts, warrants and units. There is no limit under this shelf registration statement to the amount or number of such securities that we may offer and sell, subject to market conditions. We expect to file a new... -

Page 129

... programs. Table 34 provides a summary of the credit ratings for the senior unsecured debt of Capital One Financial Corporation, COBNA and CONA as of December 31, 2014 and 2013. Table 34: Senior Unsecured Debt Credit Ratings December 31, 2014 Capital One Financial Corporation Capital One Bank (USA... -

Page 130

... the values of current holdings and future cash flows denominated in other currencies. Our primary exposure is related to the funding of and non-dollar net investments in our International Card business in the U.K and Canada. Our intercompany funding exposes our income statement to foreign exchange... -

Page 131

..., we use various industry standard market risk measurement techniques and analysis to measure, assess and manage the impact of changes in interest rates on our net interest income and our economic value of equity and foreign exchange rates on our non-dollar denominated earnings and non-dollar equity... -

Page 132

... Banking business. Our new deposit model was developed based on account-level data and incorporates lagged responses in both repricing and customer behavior as external market rates change. The modeling changes had a small impact on our economic value of equity sensitivity measure, but resulted... -

Page 133

... used to estimate the exposure to changes in market interest rates. The above sensitivity analysis contemplates only certain movements in interest rates and is performed at a particular point in time based on the existing balance sheet and, in some cases, expected future business growth and funding... -

Page 134

... 31, (Dollars in millions) 2014 2013 2012 2011 2010 Loans held for investment: Credit Card: Domestic credit card(1) ...$ 77,704 $ 73,255 $ 83,141 $ 56,609 $ 53,849 International credit card ...8,172 8,050 8,614 8,466 7,522 Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking... -

Page 135

... accordance with our expectations as of the purchase date, as we recorded these loans at estimated fair value when we acquired them. As of December 31, 2014, 2013, 2012, 2011 and 2010 the acquired loan portfolio's contractual 30 to 89 day delinquencies total $152 million, $223 million, $369 million... -

Page 136

... 31, (Dollars in millions) 2014 2013 2012 2011 2010 Nonperforming loans held for investment:(1) Credit Card: International Credit Card ...$ Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer banking ...Commercial Banking: Commercial and multifamily... -

Page 137

.... The average balance of Acquired Loans, which are included in the total average loans held for investment used in calculating the net chargeoff rates, was $25.8 billion, $32.2 billion, $36.2 billion, $5.0 billion and $6.3 billion, in 2014, 2013, 2012, 2011 and 2010, respectively. 115 Capital One... -

Page 138

... from January 1, 2010 adoption of new consolidation accounting standards ...Balance at beginning of period, as adjusted ...Provision for credit losses(1) ...Charge-offs: Domestic credit card ...International credit card ...Consumer banking ...Commercial banking ...Other loans ...Total charge-offs... -

Page 139

... and Calculation of Regulatory Capital Measures(1) December 31, 2012 (Dollars in millions) 2014 2013 2011 2010 Average Tangible Common Equity Average stockholders' equity ...Adjustments: Average goodwill and intangible assets(2) ...Average noncumulative perpetual preferred stock(3) . . Average... -

Page 140

... 31, 2012 2011 2010 Regulatory Capital Ratios Under Basel I(5) Total stockholders' equity ...$ 41,632 Adjustments: Net unrealized losses on investment securities available for sale recorded in AOCI(12) ...791 Net losses on cash flow hedges recorded in AOCI(12) ...136 Disallowed goodwill and... -

Page 141

...of consumer and commercial loans acquired in the ING Direct and Chevy Chase Bank acquisitions, and a limited portion of the credit card loans acquired in the 2012 U.S. card acquisition, which were recorded at fair value at acquisition and subsequently accounted for based on expected cash flows to be... -

Page 142

... value upon acquisition adjusted for subsequent cash collections and yield accreted to date. CCB: Chevy Chase Bank, F.S.B., which was acquired by the Company on February 27, 2009. COBNA: Capital One Bank (USA), National Association, one of our fully owned subsidiaries, which offers credit and debit... -

Page 143

... to exchange payments on a specified future date, based on a market change in interest rates from trade date to contract settlement date. GreenPoint: Refers to our wholesale mortgage banking unit, GreenPoint Mortgage Funding, Inc. ("GreenPoint"), which was closed in 2007. GSE or Agency: A government... -

Page 144

... Capital One invests in private investment funds that make equity investments in multifamily affordable housing properties that provide affordable housing tax credits for these investments. The activities of these entities are financed with a combination of invested equity capital and debt. Investor... -

Page 145

...Statement: Capital One's Proxy Statement for the 2014 Annual Stockholders Meeting. Public Fund deposits: Deposits that are derived from a variety of political subdivisions such as school districts and municipalities. Purchase volume: Dollar amount of customer purchases, net of returns. Rating Agency... -

Page 146

... funds). Acronyms ABS: Asset-backed security AOCI: Accumulated other comprehensive income ARM: Adjustable rate mortgage ASC: Accounting Standard Codification BHC: Bank holding company bps: Basis points CAD: Canadian Dollar CCAR: Comprehensive Capital Analysis and Review CDE: Community development... -

Page 147

...: Home Equity Lines of Credit HFI: Held for Investment HSBC: HSBC Finance Corporation, HSBC USA Inc. and HSBC Technology and Services (USA) Inc. LCR: Liquidity Coverage Ratio LIBOR: London Interbank Offered Rate Moody's: Moody's Investors Service MSR: Mortgage servicing rights NOW: Negotiable order... -

Page 148

...Compensation Plans ...Note 16 - Employee Benefit Plans ...Note 17 - Income Taxes ...Note 18 - Fair Value Measurement ...Note 19 - Business Segments ...Note 20 - Commitments, Contingencies, Guarantees and Others ...Note 21 - Capital One Financial Corporation (Parent Company Only) ...Note 22 - Related... -

Page 149

...may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. Management completed an assessment of the effectiveness of the Company's internal control over financial reporting as of December 31, 2014, based on the framework... -

Page 150

... balance sheets of Capital One Financial Corporation as of December 31, 2014 and 2013, and the related consolidated statements of income, comprehensive income, changes in stockholders' equity and cash flows for each of the three years in the period ended December 31, 2014, and our report dated... -

Page 151

...consolidated balance sheets of Capital One Financial Corporation (the "Company") as of December 31, 2014 and 2013, and the related consolidated statements of income, comprehensive income, changes in stockholders' equity and cash flows for each of the three years in the period ended December 31, 2014... -

Page 152

CAPITAL ONE FINANCIAL CORPORATION CONSOLIDATED STATEMENTS OF INCOME (Dollars in millions, except per share-related data) Year Ended December 31, 2014 2013 2012 Interest income: Loans, including loans held for sale ...$17,662 Investment securities ...1,628 Other ...107 Total interest income ...19,... -

Page 153

CAPITAL ONE FINANCIAL CORPORATION CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME Year Ended December 31, (Dollars in millions) 2014 2013 2012 Net income ...$4,428 Other comprehensive income (loss) before taxes: Net unrealized gains (losses) on securities available for sale ...482 Net changes in ... -

Page 154

CAPITAL ONE FINANCIAL CORPORATION CONSOLIDATED BALANCE SHEETS (Dollars in millions, except per share data) December 31, 2014 December 31, 2013 Assets: Cash and cash equivalents: Cash and due from banks ...$ Interest-bearing deposits with banks ...Federal funds sold and securities purchased under ... -

Page 155

... stock related to acquisition ...Exercise of stock options, tax benefits of exercises and restricted stock vesting ...Issuance of preferred stock (series B) ...Compensation expense for restricted stock awards and stock options ...Balance as of December 31, 2012 ...Comprehensive income (loss) ...Cash... -

Page 156

...end of the period ...Supplemental cash flow information: Non-cash items: Fair value of common stock issued in business acquisition ...Net transfers from loans held for investment to loans held for sale ...Transfer from securities available for sale to securities held to maturity ...Net debt exchange... -

Page 157

... CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 1-SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The Company Capital One Financial Corporation, a Delaware Corporation established in 1994 and headquartered in McLean, Virginia, is a diversified financial services holding company with banking... -

Page 158

... the "ING Direct Sellers"). The ING Direct acquisition resulted in the addition of loans of $40.4 billion, other assets of $53.9 billion and deposits of $84.4 billion as of the acquisition date. Basis of Presentation and Use of Estimates The accompanying consolidated financial statements have been... -

Page 159

... corporate bonds, as well as equity securities primarily related to activities under the Community Reinvestment Act ("CRA") programs. The accounting and measurement framework for our investment securities differs depending on the security classification. We classify securities as available for sale... -

Page 160

... life of the security as an adjustment to the accretable yield. See "Loans Acquired" in this Note for further discussion of accounting guidance for purchased credit-impaired loans and debt securities. Loans Our total loan portfolio consists of credit card, consumer banking and commercial banking... -

Page 161

... used the term "Acquired Loans" to refer to the substantial majority of consumer and commercial loans acquired in the Chevy Chase Bank ("CCB") and ING Direct acquisitions, and a limited portion of the credit card loans acquired in the 2012 U.S. card acquisition, which were recorded at fair value at... -

Page 162

... CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) loan sales as the difference between the proceeds received and the carrying value of the loans sold, net of the fair value of any retained servicing rights. Loans Acquired Loans Acquired and Accounted for Based on Expected Cash... -

Page 163

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) Loans Acquired and Accounted for Based on Contractual Cash Flows The substantial majority of the loans purchased in the 2012 U. S. card acquisition had existing revolving privileges at acquisition. Therefore, ... -

Page 164

... method for measuring impairment in accordance with applicable accounting guidance. Loans held for sale are also not reported as impaired, as these loans are recorded at lower of cost or fair value. Impaired loans also exclude Acquired Loans accounted for based on expected cash flows at acquisition... -

Page 165

... the earlier of the date when the account is a specified number of days past due or upon repossession of the underlying collateral. Our charge-off time frame is 180 days for home loans and 120 days for auto and other consumer installment loans. Small business banking loans generally charge off at 90... -

Page 166

...: credit card loans, auto loans, residential home loans and retail banking loans. Each of these portfolios is further divided by our business units into pools based on common risk characteristics, such as origination year, contract type, interest rate and geography, which are collectively evaluated... -

Page 167

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) also considers an evaluation of overall portfolio credit quality based on indicators such as changes in our credit evaluation, underwriting and collection management policies, the effect of other external ... -

Page 168

...are Domestic Card, International Card, Auto, Other Consumer Banking and Commercial Banking. The annual goodwill impairment test, performed as of October 1 of each year, is a two-step test. The first step identifies whether there is potential impairment by comparing the fair value of a reporting unit... -

Page 169

... market and the right to service these loans is retained for a fee. Subsequently, our consumer MSRs are carried at fair value on our consolidated balance sheets with changes in fair value recognized in non-interest income. Our commercial MSRs are subsequently measured under the amortization method... -

Page 170

... terms of the current rewards programs and card purchase activity. The customer rewards reserve is sensitive to changes in the reward redemption type and redemption rate, which is based on the expectation that the vast majority of all points earned will eventually be redeemed. The customer rewards... -

Page 171

...issue private-label and co-branded credit card loans to these customers over the term of these arrangements, which typically range from two to ten years. Certain partners assist in or perform marketing activities on our behalf and promote our products and services to their customers. As compensation... -

Page 172

... losses primarily from the unauthorized use of credit cards, debit cards and customer bank accounts. Additional fraud losses may be incurred when loans are obtained through fraudulent means. Fraud-related losses and recoveries are recorded in our consolidated statements of income as a component of... -

Page 173

...are excluded from the computation of diluted earnings per share. Derivative Instruments and Hedging Activities All derivative financial instruments, whether designated for hedge accounting or not, are reported at their fair value on our consolidated balance sheets as either assets or liabilities. We... -

Page 174

... the equity method of accounting and the passive losses related to the investments were recognized within non-interest expense. We adopted this guidance as of January 1, 2014 with retrospective application. As a result, as of December 31, 2013, total assets, total liabilities, and retained earnings... -

Page 175

... assessment required to evaluate whether organizations should consolidate certain legal entities such as limited partnerships, limited liability corporations, and securitization structures. The guidance also removed the indefinite deferral of specialized guidance for certain investment funds... -

Page 176

...-specific revenue recognition rules with a more principles-based recognition model. Most revenue associated with financial instruments, including interest and loan origination fees, is outside the scope of the guidance. Gains and losses on investment securities, derivatives and sales of financial... -

Page 177

... Fork Bancorporation, Inc. ("North Fork") acquisition. The results of the wholesale banking unit have been accounted for as a discontinued operation and are therefore not included in our results from continuing operations for the years ended December 31, 2014, 2013 and 2012. We have no significant... -

Page 178

... of Investment Portfolio (Dollars in millions) Securities available for sale, at fair value ...Securities held to maturity, at carrying value ...Total investments ...December 31, 2014 $ $ 39,508 22,500 62,008 December 31, 2013 $ $ 41,800 19,132 60,932 156 Capital One Financial Corporation (COF... -

Page 179

... by auto dealer floor plan inventory loans and leases constituted approximately 16% and 15% of the other ABS portfolio as of December 31, 2014 and 2013, respectively. Includes foreign government bonds, corporate bonds, municipal securities and equity investments primarily related to activities under... -

Page 180

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) The table below presents the carrying value, gross unrealized gains and losses, and fair value of securities held to maturity at December 31, 2014 and 2013. Table 3.3: Investment Securities Held to Maturity ... -

Page 181

...31, 2014 12 Months or Longer Gross Unrealized Losses Less than 12 Months Gross Unrealized Losses Total Gross Unrealized Losses (Dollars in millions) Fair Value Fair Value Fair Value Investment securities available for sale: U.S. Treasury and agency debt obligations . Corporate debt securities... -

Page 182

...CONSOLIDATED FINANCIAL STATEMENTS-(Continued) December 31, 2013 12 Months or Longer Gross Unrealized Losses Less than 12 Months Gross Unrealized Losses Total Gross Unrealized Losses (Dollars in millions) Fair Value Fair Value Fair Value Investment securities available for sale: Corporate debt... -

Page 183

... 3.6: Contractual Maturities of Securities Held to Maturity December 31, 2014 (Dollars in millions) Carrying Value Fair Value Due after 5 years through 10 years ...$ 1,144 $ 1,221 Due after 10 years ...21,356 22,413 Total ...$ 22,500 $23,634 Because borrowers may have the right to call or prepay... -

Page 184

... Yields of Securities December 31, 2014 (Dollars in millions) Due > 1 Year Due > 5 Years Due in 1 Year through through or Less 5 Years 10 Years Due > 10 Years Total Fair value of securities available for sale: U.S. Treasury and agency debt obligations . . Corporate debt securities guaranteed by... -

Page 185

... amortized cost basis and the present value of its expected cash flows, discounted based on the effective yield. The table below presents a rollforward of the credit related OTTI recognized in earnings for the years ended December 31, 2014, 2013 and 2012 on investment securities for which we had no... -

Page 186

... in Earnings Year Ended December 31, 2014 2013 2012 (Dollars in millions) Realized gains (losses): Gross realized gains ...Gross realized losses ...Net realized gains ...OTTI recognized in earnings: Credit-related OTTI ...Intent-to-sell OTTI ...Total OTTI recognized in earnings ...Net securities... -

Page 187

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) Changes in Accretable Yield of Acquired Securities The following table presents changes in the accretable yield related to the acquired credit-impaired debt securities: Table 3.11: Changes in Accretable Yield of... -

Page 188

...industrial and small-ticket commercial real estate loans. Our portfolio of loans held for investment also includes loans acquired in the ING Direct, CCB and 2012 U.S. card acquisitions. These loans were recorded at fair value at the date of each acquisition and are referred to as Acquired Loans. The... -

Page 189

..., 2014 30-59 Days 60-89 Days ≥ 90 Days Total Delinquent Loans Acquired Loans Total Loans (Dollars in millions) Current Credit Card: Domestic credit card(1) ...$ 75,143 International credit card ...7,878 Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer... -

Page 190

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) On February 19, 2013, we announced the Portfolio Sale of loans that we acquired in the 2012 U.S. card acquisition. We reclassified the assets subject to the sale agreement, which included loans of approximately ... -

Page 191

...net charge-offs for the years ended December 31, 2014 and 2013. Table 4.3: Credit Card: Risk Profile by Geographic Region and Delinquency Status December 31, 2014 % of Amount Total(1) December 31, 2013 % of Amount Total(1) (Dollars in millions) Domestic credit card: California ...New York ...Texas... -

Page 192

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) Table 4.4: Credit Card: Net Charge-offs Year Ended December 31, 2014 2013 Amount Rate(1) Amount Rate(1) (Dollars in millions) Net charge-offs: Domestic credit card ...International credit card ...Total credit ... -

Page 193

... Other ...18,677 Total auto ...Home loan: California ...New York ...Illinois ...Maryland ...Virginia ...New Jersey ...Florida ...Other ...Total home loan ...Retail banking: Louisiana ...New York ...Texas ...New Jersey ...Maryland ...Virginia ...California ...Other ...Total retail banking ...37,824... -

Page 194

... Charge-offs Year Ended December 31, 2014 2013 (Dollars in millions) Amount Rate(1) Amount Rate(1) Net charge-offs: Auto ...$ 619 1.78% $ 546 1.85% Home loan ...17 0.05 16 0.04 Retail banking ...39 1.07 54 1.46 Total consumer banking ...$ 675 0.95 (1) $ 616 0.85 Calculated for each loan category... -

Page 195

...Total(1) Loans (Dollars in millions) Amount % of Total(1) Total Home Loans % of Amount Total(1) Origination year:(2) < = 2005 ...2006 ...2007 ...2008 ...2009 ...2010 ...2011 ...2012 ...2013 ...2014 ...Total ...Geographic concentration:(3) California ...New York ...Illinois ...Maryland ...Virginia... -

Page 196

... total home loans held for investment. The Acquired Loans origination balances in the years subsequent to 2012 are related to refinancing of previously acquired home loans. Represents the ten states in which we have the highest concentration of home loans. Commercial Banking We evaluate the credit... -

Page 197

... corrected and are generally placed on nonaccrual status. • We use our internal risk-rating system for regulatory reporting, determining the frequency of credit exposure reviews, and evaluating and determining the allowance for loan and lease losses for commercial loans. Loans of $1 million or... -

Page 198

... 20,750 100.0% $ 23,309 100.0% $ (1) (2) (3) Percentages calculated based on total held-for-investment commercial loans in each respective loan category as of the end of the reported period. Northeast consists of CT, ME, MA, NH, NJ, NY, PA and VT. Mid-Atlantic consists of DE, DC, MD, VA and WV... -

Page 199

... Related Recorded Principal Allowance Allowance Investment Allowance Investment Balance (Dollars in millions) Credit Card: Domestic credit card ...$ 546 $ International credit card ...146 (2) Total credit card ...692 Consumer Banking: Auto(3) ...230 Home loan ...218 Retail banking ...45 Total... -

Page 200

...) Year Ended December 31, 2014 2013 Average Interest Average Interest Recorded Income Recorded Income Investment Recognized Investment Recognized (Dollars in millions) Credit Card: Domestic credit card ...$ International credit card ...Total credit card(2) ...Consumer Banking: Auto(3) ...Home loan... -

Page 201

... Balance (1) (2)(3) (4) (3)(5) (6) (3)(7) Modified Activity Reduction Activity (Months) Activity Reduction(8) (Dollars in millions) Credit Card: Domestic credit card ...International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer banking... -

Page 202

... Balance (1) (2)(3) (4) (3)(5) (6) (3)(7) Modified Activity Reduction Activity (Months) Activity Reduction(8) (Dollars in millions) Credit Card: Domestic credit card ...International credit card ...Total credit card ...Consumer Banking: Auto ...Home loan ...Retail banking ...Total consumer banking... -

Page 203

... Year Ended December 31, 2013 Total Loans Number of Contracts Total Loans 2014 (Dollars in millions) Number of Contracts 2012 Number of Contracts Total Loans Credit Card: Domestic credit card ...International credit card(1) ...Total credit card ...Consumer Banking: Auto ...Home loan ...Retail... -

Page 204

... Value of Acquired Loans The table below presents the outstanding balance and the carrying value of loans from the ING Direct, CCB and 2012 U.S. card acquisitions accounted for based on expected cash flows as of December 31, 2014 and 2013. The table separately displays loans considered credit... -

Page 205

... termination dates and specified interest rates and purposes. These commitments generally require customers to maintain certain credit standards. Collateral requirements and loan-tovalue ratios are the same as those for funded transactions and are established based on management's credit assessment... -

Page 206

... Banking Credit Card Auto Home Loan Total Retail Consumer Commercial Banking Banking Banking Other(1) Combined Unfunded Allowance Lending & Total Commitments Unfunded Allowance Reserve Reserve (Dollars in millions) Balance as of December 31, 2012 ...Provision (benefit) for credit losses ...Charge... -

Page 207

..., 2014 Consumer Banking Total Home Retail Consumer Commercial Loan Banking Banking Banking Other (Dollars in millions) Credit Card Auto Total Allowance for loan and lease losses by impairment methodology: Collectively evaluated(1) ...$ 2,985 Asset-specific(2) ...219 Acquired Loans(3) ...0 Total... -

Page 208

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) December 31, 2013 Consumer Banking Total Home Retail Consumer Commercial Loan Banking Banking Banking (Dollars in millions) Credit Card Auto Other Total Allowance for loan and lease losses by impairment ... -

Page 209

...balance sheet to securitization trusts. We have primarily securitized credit card loans and home loans, which have provided a source of funding for us and enabled us to transfer a certain portion of the economic risk of the loans or debt securities to third parties. The entity that has a controlling... -

Page 210

... Loss (Dollars in millions) Securitization-related VIEs: Credit card loan securitizations(2) ...Home loan securitizations(3) ...Total securitization-related VIEs ...Other VIEs: Affordable housing entities ...Entities that provide capital to low-income and rural communities ...Other ...Total other... -

Page 211

...Related VIEs Non-Mortgage Credit Card Option ARM Mortgage GreenPoint HELOCs GreenPoint Housing Manufactured (Dollars in millions) December 31, 2014: Securities held by third-party investors ...Receivables in the trust ...Cash balance of spread or reserve accounts ...Retained interests ...Servicing... -

Page 212

...consolidated statements of income. See "Note 10-Derivative Instruments and Hedging Activities" for further details on these derivatives. GreenPoint Mortgage Home Equity Lines of Credit ("HELOCs") Our discontinued wholesale mortgage banking unit, GreenPoint, previously sold HELOCs in whole loan sales... -

Page 213

... invest in private investment funds that make equity investments in multi-family affordable housing properties. We receive affordable housing tax credits for these investments. The activities of these entities are financed with a combination of invested equity capital and debt. For those investment... -

Page 214

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) Other Other VIEs primarily includes a variable interest that we hold in a trust that has a royalty interest in certain oil and gas properties. The activities of the trust are financed solely with debt. The total... -

Page 215

... as of December 31, 2014 and 2013. Table 7.2: Goodwill Attributable to Business Segments (Dollars in millions) Credit Card Consumer Commercial Banking Banking Total Balance as of December 31, 2012 ...$5,003 $ 4,583 $ Acquisitions ...0 3 Other adjustments ...2 (1) Balance as of December 31, 2013... -

Page 216

.... Cash flows are adjusted, as necessary, in order to maintain each reporting unit's equity capital requirements. Our discounted cash flow analysis requires management to make judgments about future loan and deposit growth, revenue growth, credit losses, and capital rates. Discount rates used in 2014... -

Page 217

... Actual for the year ended December 31, 2012 ...$ 2013 ...2014 ...Estimated future amounts for the year ended December 31, 2015 ...2016 ...2017 ...2018 ...2019 ...Thereafter ...Total estimated future amounts ...$ 609 671 532 432 335 238 153 81 73 1,312 195 Capital One Financial Corporation (COF) -

Page 218

... taxes, insurance premiums, cost of maintenance and other costs. In some cases, rentals are subject to increases in relation to a cost of living index. Total rent expenses amounted to approximately $265 million, $245 million and $216 million for the years ended December 31, 2014, 2013 and 2012... -

Page 219

... advances, which are secured by certain portions of our loan and investment securities portfolios, for our funding needs. The securitization debt obligations are separately presented on our consolidated balance sheets, while federal funds purchased and securities loaned or sold under agreements to... -

Page 220

...fair value hedge accounting adjustments. Table 9.1: Components of Deposits, Short-Term Borrowings and Long-Term Debt December 31, 2014 2013 (Dollars in millions) Deposits: Non-interest bearing deposits ...Interest-bearing deposits ...Total deposits ...Short-term borrowings: Federal funds purchased... -

Page 221

... December 31, 2014 mature as follows: Table 9.2: Maturity Profile of Borrowings and Debt (Dollars in millions) 2015 (1) 2016 2017 2018 2019 Thereafter Total Interest-bearing time deposits ...Securitized debt obligations ...Federal funds purchased and securities loaned or sold under agreements... -

Page 222

... long-term debt for the years ended December 31, 2014, 2013 and 2012: Table 9.3: Components of Interest Expense on Short-Term Borrowings and Long-Term Debt Year Ended December 31, (Dollars in millions) 2014 2013 2012 Short-term borrowings: Federal funds purchased and securities loaned or sold under... -

Page 223

...and liabilities by using interest rate derivatives. Our current asset and liability management policy also includes the use of derivatives to hedge foreign currency denominated transactions to limit our earnings and capital ratio exposure to foreign exchange risk. We execute our derivative contracts... -

Page 224

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) • Free-Standing Derivatives: We use free-standing derivatives to hedge the risk of changes in the fair value of residential MSRs, mortgage loan origination and purchase commitments and other interests held. We... -

Page 225

... by the associated commercial loans and we do not require additional collateral on these transactions. Credit Risk-Related Contingency Features and Collateral Certain of our derivatives contracts include provisions requiring that our debt maintain a credit rating of investment grade or above... -

Page 226

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) collateralization on such derivatives instruments in a net liability position. We posted $87 million and $371 million of cash collateral as of December 31, 2014 and 2013, respectively. If our debt credit rating ... -

Page 227

... Derivatives Year Ended December 31, (Dollars in millions) 2014 (1) 2013 2012 Derivatives designated as accounting hedges: Fair value interest rate contracts: Gains (losses) recognized in earnings on derivatives ...(Losses) gains recognized in earnings on hedged items ...Net fair value hedge... -

Page 228

CAPITAL ONE FINANCIAL CORPORATION NOTES TO CONSOLIDATED FINANCIAL STATEMENTS-(Continued) Cash Flow and Net Investment Hedges The table below shows the net gains (losses) related to derivatives designated as cash flow hedges and net investment hedges for the years ended December 31, 2014, 2013 and ... -

Page 229

...31, 2014 and 2013. Table 11.1: Preferred Stock Issued and Outstanding Redeemable by Issuer Beginning September 1, 2017 September 1, 2019 December 1, 2019 Carrying Value (in millions) Non-cumulative Redemption Price Number of Fixed Dividend per Depositary Depositary December 31, December 31, Rate per... -

Page 230