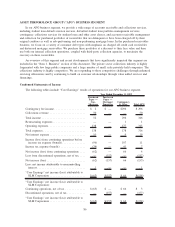

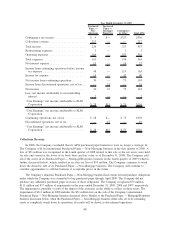

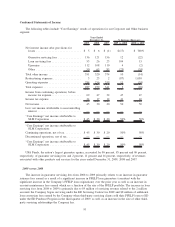

Sallie Mae 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

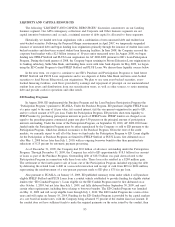

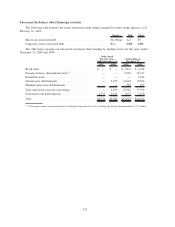

Borrowings under the 2010 Facility are non-recourse to the Company. The maximum amount the Company

may borrow under the 2010 Facility is limited based on certain factors, including market conditions and the fair

value of student loans in the facility. Funding under the 2010 Facility is subject to usual and customary conditions.

The 2010 Facility is subject to termination under certain circumstances, including the Company’s failure to comply

with the principal financial covenants in its unsecured revolving credit facilities. Increases in the borrowing rate of

up to LIBOR plus 450 basis points could occur if certain asset coverage ratio thresholds are not met. Failure to pay

off the 2010 Facility on the maturity date or to reduce amounts outstanding below the annual maximum step downs

will result in a 90-day extension of the 2010 Facility with the interest rate increasing from LIBOR plus 200 basis

points to LIBOR plus 300 basis points over that period. If, at the end of the 90-day extension, these required

paydown amounts have not been made, the collateral can be foreclosed upon.

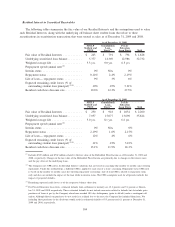

Term Asset-Backed Securities Loan Facility (“TALF”)

On February 6, 2009, the Federal Reserve Bank of New York published proposed terms for a program

designed to facilitate renewed issuance of consumer and small business ABS at lower interest rate spreads. TALF

was initiated on March 17, 2009 and currently provides investors who purchase eligible ABS with funding of up to

five years. Eligible ABS include ‘AAA’ rated student loan ABS backed by FFELP and Private Education Loans

first disbursed since May 1, 2007. As of December 31, 2009, we had approximately $9.4 billion book basis of

student loans (including $6.9 billion book basis of Private Education Loans and $2.5 billion book basis of

Consolidation Loans) eligible to serve as collateral for ABS funded under TALF; this amount does not include

loans eligible for ECASLA financing programs. For student loan collateral, TALF is scheduled to expire on

March 31, 2010.

On May 5, 2009, we priced a $2.6 billion Private Education Loan securitization which closed on May 12,

2009. The issue bears a coupon of 1-month LIBOR plus 6.0 percent and is callable at the issuer’s option at

93 percent of the outstanding balance of the ABS between November 15, 2011 and April 16, 2012. If the

issue is called on November 15, 2011, we expect the effective cost of the financing will be approximately

1-month LIBOR plus 3.7 percent. This transaction was TALF-eligible.

On July 2, 2009, we priced a $1.1 billion Private Education Loan securitization which closed on July 14,

2009. The issue bears a coupon of Prime plus 1.25 percent and is callable at the issuer’s option at 94 percent

of the outstanding balance of the ABS between January 16, 2012 and June 15, 2012. If the issue is called on

January 16, 2012, we expect the effective cost of the financing will be approximately Prime minus

0.71 percent. This transaction was TALF-eligible.

On August 5, 2009, we priced a $1.7 billion Private Education Loan securitization which closed on

August 13, 2009. The issue bears a coupon of Prime plus 0.25 percent and is callable at the issuer’s option at

94 percent of the outstanding balance of the ABS between August 15, 2013 and July 15, 2014. If the issue is

called on August 15, 2013, we expect the effective cost of the financing will be approximately Prime minus

0.55 percent. This transaction was TALF-eligible.

On December 2, 2009, we priced a $590 million Private Education Career Training Loan securitization

which closed on December 10, 2009. The issue includes one tranche that bears a coupon of Prime minus

0.90 percent and a second tranche that bears a coupon of 1-month LIBOR plus 1.85 percent. This transaction

was TALF-eligible.

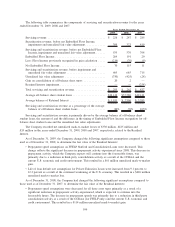

Federal Home Loan Bank in Des Moines

On January 15, 2010, HICA Education Loan Corporation, a subsidiary of the Company, entered into a

lending agreement with the Federal Home Loan Bank of Des Moines (the “FHLB”). Under the agreement, the

FHLB will provide advances backed by Federal Housing Finance Agency approved collateral which includes

federally-guaranteed student loans. The initial borrowing of $25 million at a rate of .23 percent under this

facility occurred on January 15, 2010 and matured on January 22, 2010. The amount, price and tenor of future

advances will vary and will be determined at the time of each borrowing. The maximum amount that can be

borrowed, as of January 15, 2010, subject to available collateral, is approximately $11 billion. The Company

has provided a guarantee to the FHLB for the performance and payment of HICA’s obligations.

96