Sallie Mae 2009 Annual Report Download - page 187

Download and view the complete annual report

Please find page 187 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

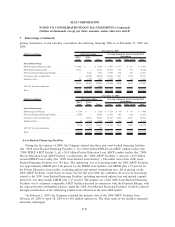

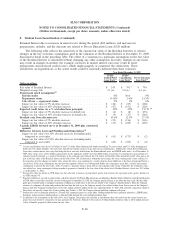

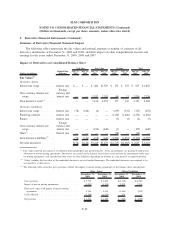

8. Student Loan Securitization (Continued)

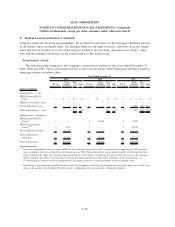

Retained Interest due to increases in interest rates during the period ($24 million), and increases in

prepayments, defaults, and the discount rate related to Private Education Loans ($120 million).

The following table reflects the sensitivity of the current fair value of the Residual Interests to adverse

changes in the key economic assumptions used in the valuation of the Residual Interest at December 31, 2009,

discussed in detail in the preceding table. The effect of a variation in a particular assumption on the fair value

of the Residual Interest is calculated without changing any other assumption. In reality, changes in one factor

may result in changes in another (for example, increases in market interest rates may result in lower

prepayments and increased credit losses), which might magnify or counteract the sensitivities. These

sensitivities are hypothetical, as the actual results could be materially different than these estimates.

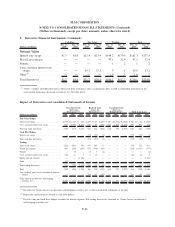

FFELP

Stafford/PLUS

Loan Trusts

(5)

FFELP

Consolidation

Loan Trusts

(5)

Private Education

Loan Trusts

(5)

Year Ended December 31, 2009

(Dollars in millions)

Fair value of Residual Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 243 $ 791

(1)

$ 794

Weighted-average life . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3.3 yrs. 9.0 yrs. 6.3 yrs.

Prepayment speed assumptions

(2)

Interim status .......................................... 0%N/A 0%

Repayment status........................................ 0-14%2-4%2-15%

Life of loan — repayment status ............................. 9%3%6%

Impact on fair value of 5% absolute increase . . . . . . . . . . . . . . . . . . . . . $ (26) $ (85) $ (128)

Impact on fair value of 10% absolute increase . . . . . . . . . . . . . . . . . . . . $ (47) $ (151) $ (229)

Expected credit losses (as a % of student loan principal) ............ .10%.25%5.31%

(3)

Impact on fair value of 5% absolute increase in default rate . . . . . . . . . . . $ (4) $ (8) $ (176)

Impact on fair value of 10% absolute increase in default rate . . . . . . . . . . $ (9) $ (17) $ (346)

Residual cash flows discount rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10.6%12.3%27.5%

Impact on fair value of 5% absolute increase . . . . . . . . . . . . . . . . . . . . . $ (29) $ (136) $ (116)

Impact on fair value of 10% absolute increase . . . . . . . . . . . . . . . . . . . . $ (53) $ (230) $ (205)

3 month LIBOR forward curve at December 31, 2009 plus contracted

spreads

Difference between Asset and Funding underlying indices

(4)

Impact on fair value of 0.25% absolute increase in funding index

compared to asset index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ (41) $ (173) $ (2)

Impact on fair value of 0.50% absolute increase in funding index

compared to asset index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ (82) $ (345) $ (4)

(1)

Certain consolidation trusts have $3.3 billion of non-U.S. dollar (Euro denominated) bonds outstanding. To convert these non-U.S. dollar denominated

bonds into U.S. dollar liabilities, the trusts have entered into foreign-currency swaps with certain counterparties. Additionally, certain Private Education

Loan trusts contain interest rate swaps that hedge the basis and reset risk between the Prime indexed assets and LIBOR index notes. As of December 31,

2009, these swaps are in a $910 million gain position (in the aggregate) and the trusts had $603 million of exposure to counterparties (gain position less

collateral posted) primarily as a result of the decline in the exchange rates between the U.S. dollar and the Euro. This unrealized market value gain is not

part of the fair value of the Residual Interest in the table above. Not all derivatives within the trusts require the swap counterparties to post collateral to

the respective trust for changes in market value, unless the trust’s swap counterparty’s credit rating has been withdrawn or has been downgraded belowa

certain level. If the swap counterparty does not post the required collateral or is downgraded further, the counterparty must find a suitable replacement

counterparty or provide the trust with a letter of credit or a guaranty from an entity that has the required credit ratings. Ultimately, the Company’s expo-

sure related to a swap counterparty failing to make its payments is limited to the fair value of the related trust’s Residual Interest, which was $1.3 billion

as of December 31, 2009.

(2)

See previous table for details on CPR. Impact on fair value due to increase in prepayment speeds only increases the repayment status speeds. Interim sta-

tus CPR remains 0%.

(3)

Expected credit losses are used to project future cash flows related to the Private Education Loan securitization’s Residual Interest. However, until the fourth quarter

of 2008 when it ceased this activity for all trusts settling prior to September 30, 2005, the Company purchased loans at par when the loans reach 180 days delin-

quent prior to default under a contingent call option, resulting in no credit losses at the trust nor related to the Company’s Residual Interest. When the Company

exercises its contingent call option and purchases the loan from the trust at par, the Company records a loss related to these loans that are now on the Company’s

balance sheet. The Company recorded losses of $0, $141 million and $123 million for the years ended December 31, 2009, 2008 and 2007, respectively, related to

this activity and specialty claims. For all trusts settling after October 1, 2005, the Company does not hold this contingent call option.

(4)

Student loan assets are primarily indexed to a Treasury bill, commercial paper or a prime index. Funding within the trust is primarily indexed to a LIBORindex.

Sensitivity analysis increases funding indexes as indicated while keeping the assets underlying indexes fixed.

(5)

In addition to the assumptions in the table above, the Company also projects the reduction in distributions that will result from the various benefit pro-

grams that exist related to consecutive on-time payments by borrowers. Related to the entire $1.8 billion Residual Interest, there is $214 million (present

value) of benefits projected, which reduce the fair value.

F-60

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)