Sallie Mae 2009 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

BUSINESS SEGMENTS

We provide credit products and related services to the higher education and consumer credit communities

and others through two primary business segments: our Lending business segment and our Asset Performance

Group (“APG”) business segment. In addition, within our Corporate and Other business segment, we provide a

number of products and services that are managed within smaller operating segments, the most prominent

being our Guarantor Servicing and Loan Servicing businesses. As discussed above, some of our businesses are

expected to go into run-off as a result of pending legislation. Each of these segments is summarized below.

The accounting treatment for the segments is explained in “MANAGEMENT’S DISCUSSION AND ANAL-

YSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.”

LENDING BUSINESS SEGMENT

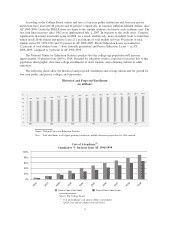

In the Lending business segment, we originate and acquire both federally guaranteed student loans, and

Private Education Loans, which are not federally guaranteed. We manage the largest portfolio of FFELP and

Private Education Loans in the student loan industry, and have 10 million student and parent customers

through our ownership and management of $176.4 billion in Managed student loans as of December 31, 2009,

of which $141.4 billion or 80 percent are federally insured. We serve over 6,000 clients, including educational

and financial institutions and non-profit state agencies. We are the largest servicer and collector of student

loans, servicing $194.2 billion in assets, including $26.3 billion for third parties, of which $19.2 billion is

serviced for ED as of December 31, 2009.

Sallie Mae’s Lending Business

Our primary marketing point-of-contact is the school’s financial aid office. We deliver flexible and cost-

effective products to the school and its students. The focus of our sales force is to market Sallie Mae’s suite of

education finance products to colleges. These include FFELP and Private Education Loans and through our

Web-based loan origination and servicing platform OpenNet». As a result of the changes taking place in the

student loan marketplace, we are broadening our marketing activities to include Direct to Consumer initiatives

and referral lending relationships. We also intend to drive loan volume through our Planning, Paying and

Saving for college activities.

In 2009, we originated $24.9 billion in student loans. FFELP originations for the year ended December 31,

2009 totaled $21.7 billion, an increase of 21 percent from the year ended December 31, 2008. The increase in

FFELP loan origination growth was due to higher loan limits and an increase in market share. Given the

legislative uncertainty around FFELP and the ongoing transition of certain schools to Direct Lending, FFELP

originations could be substantially lower in the AY 2010–2011. Private Education Loan originations totaled

$3.2 billion, a decrease of 50 percent from the prior year. The decline in Private Education Loan originations

was due to a tightening of our underwriting requirements, an increase in federal student loan limits and the

Company’s withdrawal from certain markets.

Private Education Loans

We bear the full credit risk for Private Education Loans, which are underwritten and priced according to

credit risk based upon customized credit scoring criteria. Due to their higher risk profile, generally Private

Education Loans have higher interest rates than FFELP loans. Despite a decline in the growth rate of Private

Education Loan originations, the portfolio grew 5 percent from the prior year. All new Private Education

Loans are being funded at Sallie Mae Bank through our deposit taking activities.

In 2008 and 2009, the credit environment created significant challenges for funding Private Education

Loans. At the same time, we became more restrictive in our underwriting criteria. In addition, as discussed

above, federal lending limits increased significantly in 2007 and 2008. As a result of these factors, originations

declined in 2008 and 2009. We expect originations to grow once again in 2010 and subsequent years as the

credit markets continue to recover and the impact of the 2007 and 2008 federal loan limit increases is offset

by tuition increases and market share gains.

6