Sallie Mae 2009 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

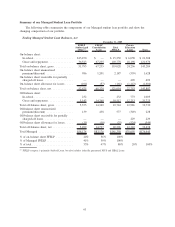

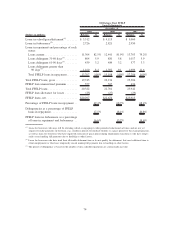

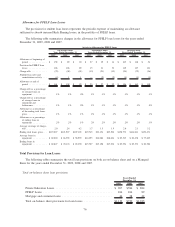

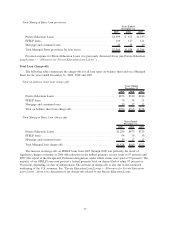

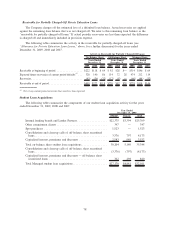

Managed provision expense decreased to $874 million in 2008 from $1.2 billion in 2007. In the fourth

quarter of 2007, the Company recorded provision expense of $667 million for the Managed Private Education

Loan portfolio. This significant level of provision expense, compared to prior and subsequent quarters,

primarily related to the non-traditional portion of the Company’s Private Education Loan portfolio which the

Company had been expanding over the past few years. The Company has terminated these non-traditional loan

programs because the performance of these loans was found to be materially different from original

expectations. The non-traditional portfolio is particularly impacted by the weakening U.S. economy and an

underlying borrower’s ability to repay.

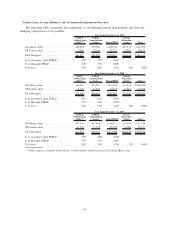

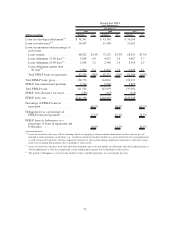

Forbearance involves granting the borrower a temporary cessation of payments (or temporary acceptance

of smaller than scheduled payments) for a specified period of time. Using forbearance in this manner

effectively extends the original term of the loan. Forbearance does not grant any reduction in the total

repayment obligation (principal or interest). While a loan is in forbearance status, interest continues to accrue

and is capitalized to principal when the loan re-enters repayment status. Our forbearance policies include

limits on the number of forbearance months granted consecutively and the total number of forbearance months

granted over the life of the loan. In some instances, we require good-faith payments before granting

forbearance. Exceptions to forbearance policies are permitted when such exceptions are judged to increase the

likelihood of ultimate collection of the loan. Forbearance as a collection tool is used most effectively when

applied based on a borrower’s unique situation, including historical information and judgments. We combine

borrower information with a risk-based segmentation model to assist in our decision making as to who will be

granted forbearance based on our expectation as to a borrower’s ability and willingness to repay their

obligation. This strategy is aimed at mitigating the overall risk of the portfolio as well as encouraging cash

resolution of delinquent loans.

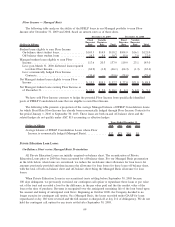

Forbearance may be granted to borrowers who are exiting their grace period to provide additional time to

obtain employment and income to support their obligations, or to current borrowers who are faced with a

hardship and request forbearance time to provide temporary payment relief. In these circumstances, a

borrower’s loan is placed into a forbearance status in limited monthly increments and is reflected in the

forbearance status at month-end during this time. At the end of their granted forbearance period, the borrower

will enter repayment status as current and is expected to begin making their scheduled monthly payments on a

go-forward basis.

Forbearance may also be granted to borrowers who are delinquent in their payments. In these

circumstances, the forbearance cures the delinquency and the borrower is returned to a current repayment

status. In more limited instances, delinquent borrowers will also be granted additional forbearance time. As we

have obtained further experience about the effectiveness of forbearance, we have reduced the amount of time a

loan will spend in forbearance, thereby increasing our ongoing contact with the borrower to encourage

consistent repayment behavior once the loan is returned to a current repayment status. As a result, the balance

of loans in a forbearance status as of month-end has decreased over the course of 2008 and 2009. In addition,

the monthly average amount of loans granted forbearance as a percentage of loans in repayment and

forbearance declined to 5.6 percent in the fourth quarter of 2009 compared to the year-ago quarter of

6.5 percent. As of December 31, 2009, 1.9 percent of loans in current status were delinquent as of the end of

the prior month, but were granted a forbearance that made them current during December.

70