Sallie Mae 2009 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

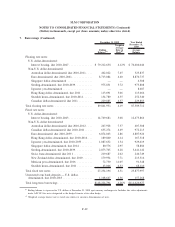

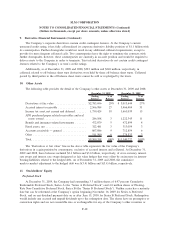

8. Student Loan Securitization (Continued)

Servicing and securitization revenue is primarily driven by the average balance of off-balance sheet

student loans, the amount of and the difference in the timing of Embedded Floor Income recognition for off-

balance sheet student loans, and the fair value adjustment related to those Residual Interests where the

Company has elected to carry such Residual Interests at fair value through earnings under ASC 825.

The Company recorded net unrealized mark-to-market losses of $330 million, $425 million and $24 million

in the years ended December 31, 2009, 2008 and 2007, respectively, related to the Residual Interest.

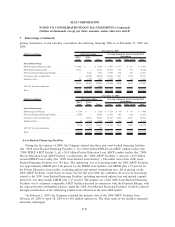

As of December 31, 2009, the Company changed the following significant assumptions compared to

those used as of December 31, 2008, to determine the fair value of the Residual Interests:

• Prepayment speed assumptions on FFELP Stafford and Consolidation Loans were decreased. This change

reflects the significant decrease in prepayment activity experienced since 2008. This decrease in

prepayment activity, which the Company expects will continue into the foreseeable future, was primarily

due to a reduction in third-party consolidation activity as a result of the CCRAA and the current

U.S. economic and credit environment. This resulted in a $61 million unrealized mark-to-market gain.

• Life of loan default rate assumptions for Private Education Loans were increased from 9.1 percent to

12.2 percent as a result of the continued weakening of the U.S. economy. This resulted in a $426 million

unrealized mark-to-market loss.

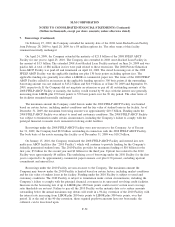

As of December 31, 2008, the Company had changed the following significant assumptions compared to

those used as of December 31, 2007, to determine the fair value of the Residual Interests:

• Prepayment speed assumptions were decreased for all three asset types primarily as a result of a

significant reduction in prepayment activity experienced, which is expected to continue into the

foreseeable future. The decrease in prepayment speeds was primarily due to a reduction in third-party

consolidation activity as a result of the CCRAA (for FFELP only) and the current U.S. economic and

credit environment. This resulted in a $114 million unrealized mark-to-market gain.

• Life of loan default rate assumptions for Private Education Loans were increased as a result of the

continued weakening of the U.S. economy. This resulted in a $79 million unrealized mark-to-market loss.

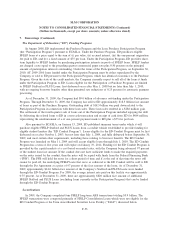

• Cost of funds assumptions related to the underlying auction rate securities bonds ($2.3 billion face

amount of bonds) within FFELP loan ($1.7 billion face amount of bonds) and Private Education Loan

($0.6 billion face amount of bonds) trusts were increased to take into account the expectations these

auction rate securities would continue to reset at higher rates for an extended period of time. This

resulted in a $116 million unrealized mark-to-market loss.

• The discount rate assumption related to the Private Education Loan and FFELP Residual Interests was

increased. The Company assessed the appropriateness of the current risk premium, which was added to the

risk free rate for the purpose of arriving at a discount rate, in light of the current economic and credit

uncertainty that existed in the market as of December 31, 2008. This discount rate was applied to the

projected cash flows to arrive at a fair value representative of the then current economic conditions. The

Company increased the risk premium by 1,550 basis points and 390 basis points for Private Education Loans

and FFELP loans, respectively, to take into account the then current level of cash flow uncertainty and lack

of liquidity that existed with the Residual Interests. This resulted in a $904 million unrealized mark-to-market

loss.

The Company recorded impairments to the Retained Interests of $254 million for the year ended

December 31, 2007. The impairment charges were the result of FFELP loans prepaying faster than projected

through loan consolidations ($110 million), impairment to the Floor Income component of the Company’s

F-59

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)