Sallie Mae 2009 Annual Report Download - page 25

Download and view the complete annual report

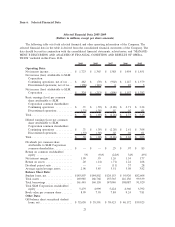

Please find page 25 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

loans with cosigners have increased. The Company expects to maintain its high quality underwriting standards.

The impact of this initiative and the overall economy may impact future Private Education Loan asset growth.

“Core Earnings” net interest income was $2.3 billion in 2009 compared to $2.4 billion in 2008. “Core

Earnings” net interest income was negatively impacted in 2009 compared to 2008 primarily as a result of an

18 basis point widening of the CP/LIBOR spread and higher credit spreads on the Company’s ABS debt issued

in 2008 and 2009 due to the current credit environment. Partially offsetting these decreases to net interest

income were lower cost of funds related to the ED Conduit Program, lower borrowing costs associated with

our ABCP facility, higher asset spreads earned on Private Education Loans originated during 2009 compared

to prior years, and a $12 billion increase in the average balance of Managed student loans.

Fee Income

“Core Earnings” fee income from our contingency business declined $44 million from $340 million in

2008 to $296 million in 2009. This decline was primarily a result of significantly less guarantor collections

revenue associated with rehabilitating delinquent FFELP loans. Loans are considered rehabilitated after a

certain number of on-time payments have been collected. The Company earns a rehabilitation fee only when

the Guarantor sells the rehabilitated loan. The disruption in the credit markets has limited the sale of

rehabilitated loans.

“Core Earnings” fee income from our Guarantor Servicing business was $136 million for the year, a

$15 million increase from last year. This increase primarily relates to an increase in guarantor issuance fees

earned as a result of a significant increase in FFELP loan guarantees (consistent with the significant increase

in the Company’s FFELP loan originations) over the prior year as well as an increase in account maintenance

fees earned which are a function of the size of the FFELP portfolio.

A source of additional fee income for 2010 will be third-party servicing revenue. As previously discussed,

the Company began servicing 2 million accounts in the fourth quarter of 2009 under the ED Servicing

Contract. The Company earned $9 million of servicing revenue in the fourth quarter of 2009 related to this

contract and expects this to grow significantly as this third-party serviced portfolio increases over time.

Purchased Paper Business

In 2008, we decided to exit the debt purchased paper business (see “ASSET PERFORMANCE GROUP

BUSINESS SEGMENT”).

The Company sold its international Purchased Paper — Non-Mortgage business in the first quarter of

2009. The Company sold all of the assets in its Purchased Paper — Mortgage/Properties business in the fourth

quarter of 2009. With the sale of GRP, the Purchased Paper — Mortgage/Properties business is required to be

presented separately as discontinued operations for all periods presented. This sale of assets in the fourth

quarter of 2009 resulted in an after-tax loss of $95 million. As of December 31, 2009, the portfolio of assets

related to the Purchased Paper business was $285 million.

Operating Expenses

For 2009, operating expenses on a “Core Earnings” basis were $1.18 billion, compared to $1.23 billion in

2008. The $50 million decrease in operating expenses was primarily due to the Company’s cost reduction

efforts, offset by an increase in collection costs for delinquent and defaulted loans as well as higher expenses

incurred to reconfigure the Company’s servicing system to meet the requirements of the ED Servicing Contract

awarded in 2009.

Capital Adequacy

At year-end, the Company’s tangible capital ratio was 2.0 percent of Managed assets, compared to

1.8 percent at 2008 year-end. With 80 percent of our Managed loans carrying an explicit federal government

guarantee and 85 percent of our Managed loans funded for the life of the loan, we currently believe that our

24