Sallie Mae 2009 Annual Report Download - page 242

Download and view the complete annual report

Please find page 242 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

-

254

-

255

-

256

|

|

applicant (and parents in the case of a dependent child) must undergo a financial need analysis. This requires

the applicant (and parents in the case of a dependent child) to submit financial data to a federal processor. The

federal processor evaluates the parents’ and student’s financial condition under federal guidelines and

calculates the amount that the student and the family are expected to contribute towards the student’s cost of

education. After receiving information on the family contribution, the institution then subtracts the family

contribution from the student’s estimated costs of attending to determine the student’s need for financial aid.

Some of this need may be met by grants, scholarships, institutional loans and work assistance. A student’s

“unmet need” is further reduced by the amount of loans for which the borrower is eligible.

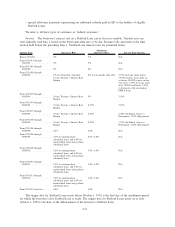

Special Allowance Payments (“SAP”)

The HEA provides for quarterly special allowance payments to be made by ED to holders of student

loans to the extent necessary to ensure that they receive at least specified market interest rates of return. The

rates for special allowance payments depend on formulas that vary according to the type of loan, the date the

loan was made and the type of funds, tax-exempt or taxable, used to finance the loan. ED makes a SAP for

each calendar quarter.

The SAP equals the average unpaid principal balance, including interest which has been capitalized, of

all eligible loans held by a holder during the quarterly period multiplied by the special allowance percentage.

For student loans disbursed before January 1, 2000, the special allowance percentage is computed by:

(1) determining the average of the bond equivalent rates of 91-day Treasury bills auctioned for that

quarter;

(2) subtracting the applicable borrower interest rate;

(3) adding the applicable special allowance margin described in the table below; and

(4) dividing the resultant percentage by 4.

If the result is negative, the SAP is zero.

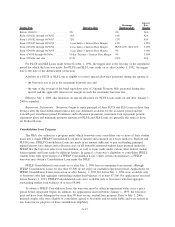

Date of First Disbursement Special Allowance Margin

Before 10/17/86 ............................ 3.50%

From 10/17/86 through 09/30/92 ................ 3.25%

From 10/01/92 through 06/30/95 ................ 3.10%

From 07/01/95 through 06/30/98 ................ 2.50% for Stafford Loans that are in In-School, Grace

or Deferment 3.10% for Stafford Loans that are in

Repayment and all other loans

From 07/01/98 through 12/31/99 ................ 2.20% for Stafford Loans that are in In-School, Grace

or Deferment 2.80% for Stafford Loans that are in

Repayment 3.10% for PLUS, SLS and FFELP

Consolidation Loans

For student loans disbursed on or after January 1, 2000, the special allowance percentage is computed by:

(1) determining the average of the bond equivalent rates of 3-month commercial paper (financial)

rates quoted for that quarter;

(2) subtracting the applicable borrower interest rate;

(3) adding the applicable special allowance margin described in the table below; and

(4) dividing the resultant percentage by 4.

If the result is negative, the SAP is zero.

A-7