Sallie Mae 2009 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

the notes will be repaid with funds from the Federal Financing Bank (“FFB”). The FFB will hold the notes for a

short period of time and, if at the end of that time the notes still cannot be paid off, the underlying FFELP loans

that serve as collateral to the ED Conduit will be sold to ED through the Put Agreement at a price of 97 percent of

the face amount of the loans. As of December 31, 2009, approximately $14.6 billion face amount of our Stafford

and PLUS Loans were funded through the ED Conduit Program. For 2009, the average interest rate paid on this

facility was approximately 0.75 percent. As of December 31, 2009, there are approximately $820 million face

amount of additional FFELP Stafford and PLUS Loans (excluding loans currently in the Participation Program)

that can be funded through the ED Conduit Program.

Additional Funding Sources for General Corporate Purposes

In addition to funding FFELP loans through ED’s Participation and Purchase Programs and the ED

Conduit Program, the Company employs other financing sources for general corporate purposes, which include

originating Private Education Loans and repurchases and repayments of unsecured debt obligations.

Secured borrowings, including securitizations, asset-backed commercial paper (“ABCP”) borrowings, ED

financing facilities and indentured trusts, comprised 82 percent of our Managed debt outstanding at

December 31, 2009 versus 78 percent at December 31, 2008.

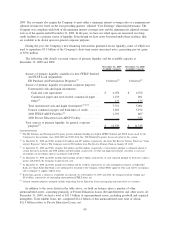

Sallie Mae Bank

During the fourth quarter of 2008, Sallie Mae Bank, our Utah industrial bank subsidiary, began expanding its

deposit base to fund new Private Education Loan originations. Sallie Mae Bank raises deposits primarily through

intermediaries in the retail brokered CD market. As of December 31, 2009, total term bank deposits were

$5.6 billion and cash and liquid investments totaled $2.4 billion. As of December 31, 2009, $4.2 billion of Private

Education Loans were held at Sallie Mae Bank. We ultimately expect to raise additional long-term financing,

through Private Education Loan securitizations or other financings, to fund these loans. In the near term, we expect

Sallie Mae Bank to continue to fund newly originated Private Education Loans through long-term bank deposits.

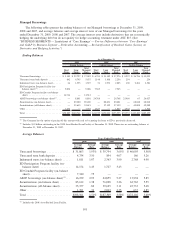

ABS Transactions

On January 6, 2009, we closed a $1.5 billion 12.5 year asset-backed securities (“ABS”) based facility. This

facility is used to provide up to $1.5 billion term financing for Private Education Loans. The fully-utilized cost of

financing obtained under this facility is expected to be LIBOR plus 5.75 percent. In connection with this facility,

we completed one Private Education Loan term ABS transaction totaling $1.5 billion in the first quarter of 2009.

The net funding received under the asset-backed securities based facility for this issuance was $1.1 billion.

In 2009, we completed four FFELP long-term ABS transactions totaling $5.9 billion. The FFELP

transactions were composed primarily of FFELP Consolidation Loans which were not eligible for the ED

Conduit Program or the Term Asset-Backed Securities Loan Facility (“TALF”) discussed below.

During 2009, we completed $7.5 billion of Private Education Loan term ABS transactions, all of which were

private placement transactions. On January 6, 2009, we closed a $1.5 billion 12.5 year asset-backed securities

(“ABS”) based facility. This facility is used to provide up to $1.5 billion term financing for Private Education

Loans. The fully utilized cost of financing obtained under this facility is expected to be LIBOR plus 5.75 percent.

In connection with this facility, we completed one Private Education Loan term ABS transaction totaling $1.5 billion

in the first quarter of 2009. The net funding received under the asset-backed securities based facility for this

issuance was $1.1 billion. In addition, we completed $6.0 billion of Private Education Loan term ABS transactions

which were TALF-eligible. See “Term Asset-Backed Securities Loan Facility (“TALF”)” below for additional

details. Although we have demonstrated our access to the ABS market in 2009 and we expect ABS financing to

remain a primary source of funding over the long term, we expect our transaction volumes to be more limited and

pricing less favorable than prior to the credit market dislocation that began in the summer of 2007, with

significantly reduced opportunities to place subordinated tranches of ABS with investors. At present, while the

markets have demonstrated some signs of recovery, we are unable to predict when market conditions will allow for

more regular, reliable and cost-effective access to the term ABS market.

94