Sallie Mae 2009 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

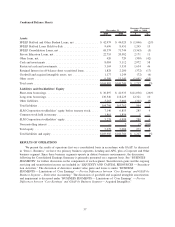

|

|

received are adequate compensation as defined in ASC 860. To the extent such compensation is determined to

be no more or less than adequate compensation, no servicing asset or obligation is recorded.

See discussion that follows on changes to accounting principles associated with transfers of financial

assets and the Variable Interest Entity Consolidation Model that will be effective in 2010.

Transfers of Financial Assets and the Variable Interest Entity (“VIE”) Consolidation Model — Changes

in Accounting Principles effective January 1, 2010

In June 2009, the FASB issued topic updates to ASC 860, “Transfers and Servicing,” and to ASC 810,

“Consolidation.”

The topic update to ASC 860, among other things, (1) eliminates the concept of a Qualifying Special

Purpose Entity (“QSPE”), (2) changes the requirements for derecognizing financial assets, (3) changes the

amount of the recognized gain/loss on a transfer accounted for as a sale when beneficial interests are received

by the transferor, and (4) requires additional disclosure. The topic update to ASC 860 is effective for

transactions which occur in fiscal years beginning after November 15, 2009. The impact of ASC 860 to future

transactions will depend on how such transactions are structured. ASC 860 relates primarily to the Company’s

secured borrowing facilities. All of the Company’s secured borrowing facilities entered into in 2008 and 2009,

including securitization trusts, have been accounted for as on balance sheet financing facilities. These

transactions would have been accounted for in the same manner if ASC 860 had been effective during these

years.

The topic update to ASC 810 significantly changes the consolidation model for Variable Interest Entities

(“VIEs”). The topic update amends ASC 810 and, among other things, (1) eliminates the exemption for

QSPEs, (2) provides a new approach for determining who should consolidate a VIE that is more focused on

control rather than economic interest, (3) changes when it is necessary to reassess who should consolidate a

VIE and (4) requires additional disclosure. The topic update to ASC 810 is effective for the first annual

reporting period beginning after November 15, 2009.

Under ASC 810, if an entity has a Variable Interest in a VIE and that entity is determined to be the

Primary Beneficiary of the VIE then that entity will consolidate the VIE. The Primary Beneficiary is the entity

which has both: (1) the power to direct the activities of the VIE that most significantly impact the VIE’s

economic performance and (2) the obligation to absorb losses or receive benefits of the entity that could

potentially be significant to the VIE. As it relates to the Company’s securitized assets, the Company is the

servicer of the securitized assets and owns the Residual Interest of the securitization trusts. As a result the

Company is the Primary Beneficiary of its securitization trusts and will consolidate those trusts that are off-

balance sheet at their historical cost basis on January 1, 2010. The historical cost basis is the basis that would

exist if these securitization trusts had remained on balance sheet since they settled. ASC 810 did not change

the accounting of any other VIEs the Company has on its balance sheet as of January 1, 2010. These new

accounting rules apply to new transactions entered into from January 1, 2010 forward as well.

On January 1, 2010, upon adopting ASC 810, the Company removed the $1.8 billion of Residual Interests

associated with these trusts from the consolidated balance sheet and the Company consolidated $35.0 billion

of assets ($32.6 billion of which are student loans, net of a $550 million allowance for loan loss) and

$34.4 billion of liabilities (primarily trust debt), which resulted in an approximate $0.7 billion after-tax

reduction of stockholders’ equity (through retained earnings). After adoption of ASC 810, related to the

securitization trusts that were consolidated on January 1, 2010, the Company’s results of operations will no

longer reflect servicing and securitization income related to these securitization trusts, but will instead report

interest income, provisions for loan losses associated with the securitized assets and interest expense associated

with the debt issued from the securitization trusts to third parties. This presentation will be identical to the

Company’s accounting treatment of prior on-balance securitization trusts. The Company has not had a

securitization that was treated as a sale since 2007.

Management allocates capital on a Managed Basis. This change will not impact management’s view of

capital adequacy for the Company. The Company’s unsecured revolving credit facilities contain two principal

32