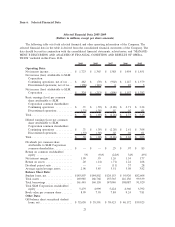

Sallie Mae 2009 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

decision was appealed to the Ninth Circuit Court of Appeals. On January 25, 2010, the Ninth Circuit Court of

Appeals affirmed the summary judgment on all counts on the basis of federal preemption.

On September 17, 2007, the Company became a party to a qui tam whistleblower case, United States ex.

Rel. Rhonda Salmeron v. Sallie Mae, in the U.S. District Court for the Northern District of Illinois. The relator

alleged that various defendants submitted false claims and/or created records to support false claims in

connection with collection activity on federally guaranteed student loans, and specifically that the Company

was negligent in auditing the collection practices of one of the defendants. The relator sought money damages

in excess of $12 million plus treble damages on behalf of the federal government. The District Court dismissed

the case with prejudice in August 2008 and the relator appealed to the Seventh Circuit Court of Appeals in

September 2008. On August 27, 2009, the Seventh Circuit Court of Appeals affirmed the dismissal.

On December 17, 2007, plaintiffs filed a complaint against the Company, Rodriguez v. SLM Corporation

et al., in the U.S. District Court for the District of Connecticut alleging that the Company engaged in

underwriting practices which, among other things, resulted in certain applicants for student loans being

directed into substandard and expensive loans on the basis of race. The plaintiffs have not stated the relief

they seek. The court denied SLM Corporation’s Motion for Summary Judgment without prejudice on June 24,

2009. The Court granted Defendants partial Motion to Dismiss the Truth in Lending Act counts on

November 10, 2009. Discovery is proceeding.

On April 20, 2009, the Company received a letter on behalf of a shareholder, SEIU Pension Plans Master

Trust, demanding, among other things, that the Company’s Board of Directors take action to recover Company

funds it alleges were “unjustly paid to certain current and former employees and executive officers of the

Company” from 2005 to the present, file civil lawsuits against former and current executives, revise the executive

compensation structure, and offer shareholders an annual nonbinding “say on pay.” Twenty-nine financial services

companies received similar letters that same week. This letter was referred to the Board of Directors. After

investigation and consideration, the Board determined that it was not in the best interest of the Company’s

shareholders for the Company to take any further action with respect to the allegations in the letter. Board counsel

conveyed that decision to counsel for the SEIU Pension Plans Master Trust in a letter dated November 9, 2009.

On July 15, 2009, the U.S. District Court for the District of Columbia unsealed the qui tam False Claims

Act complaint of relator Sheldon Batiste, a former employee of SLM Financial Corporation (U.S. ex rel.

Batiste v. SLM Corporation, et al.). The First Amended Complaint alleges that the Company violated the False

Claims Act by its “systemic failure to service loans and abide by forbearance regulations” and “its receipt of

U.S. subsidies to which it was not entitled” through the federally guaranteed student loan program, FFELP. No

amount in controversy is specified, but the relator seeks treble actual damages, as well as civil monetary

penalties on each of its claims. The U.S. Department of Justice declined intervention. The Company filed its

Motion to Dismiss on September 21, 2009. The Motion remains pending.

On August 3, 2009, the Company received the final audit report of ED’s Office of the Inspector General

(“OIG”) related to the Company’s billing practices for special allowance payments. Among other things, the

OIG recommended that ED instruct the Company to return approximately $22 million in alleged special

allowance overpayments. The Company continues to believe that its practices were consistent with longstand-

ing ED guidance and all applicable rules and regulations and intends to continue disputing these findings. The

Company provided its response to the Secretary on October 2, 2009. The OIG has audited other industry

participants with regard to special allowance payments for loans funded by tax exempt obligations and in

certain cases the Secretary of ED has disagreed with the OIG’s recommendations.

On August 26, 2009, the U.S. District Court for the Eastern District of Virginia unsealed a qui tam False

Claims Act complaint filed on September 21, 2007 by a former ED researcher, Dr. Jon Oberg, against eleven

student loan companies, including two Sallie Mae companies, SLM Corporation and Southwest Student

Services Corporation (Southwest) (U.S. ex rel. Oberg v. Nelnet et al.). The complaint seeks the return of

approximately $1 billion in the aggregate from the eleven companies as a result of alleged improper

“recycling” of 9.5 percent SAP loans. The U.S. Department of Justice declined to intervene. The allegations

against SLM Corporation in the amended complaint appear to be that Southwest allegedly engaged in

wrongful “recycling” of student loans. The Company purchased Southwest in 2004. According to the

17