Sallie Mae 2009 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

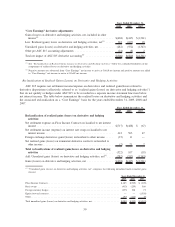

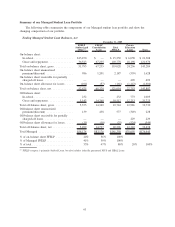

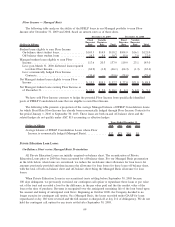

Student Loan Spread — On-Balance Sheet

The student loan spread is impacted by changes in its various components, as reflected in footnote (2) to

the “Net Interest Margin — On-Balance Sheet” table above. Gross Floor Income is impacted by interest rates

and the percentage of the FFELP portfolio earning Floor Income. Floor Income Contracts used to economi-

cally hedge Gross Floor Income do not qualify as ASC 815 hedges and as a result the net settlements on such

contracts are not recorded in net interest margin but rather in “gains (losses) on derivative and hedging

activities, net” line in the consolidated statements of income. The spread impact from Consolidation Loan

Rebate Fees fluctuates as a function of the percentage of FFELP Consolidation Loans on our balance sheet.

Repayment Borrower Benefits are generally impacted by the terms of the Repayment Borrower Benefits being

offered as well as the payment behavior of the underlying loans. Premium and discount amortization is

generally impacted by the prices previously paid for loans and amounts capitalized related to such purchases

or originations. Premium and discount amortization is also impacted by prepayment behavior of the underlying

loans.

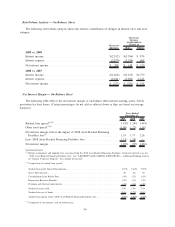

The student loan spread, before 2008 Asset-Backed Financing Facilities fees, for the year ended

December 31, 2009, increased 14 basis points from the prior year. The student loan spread was positively

impacted by lower cost of funds related to the ED Conduit Program (See “LIQUIDITY AND CAPITAL

RESOURCES — ED Funding Programs”), higher asset spreads earned on Private Education Loans originated

during 2009 compared to prior years, an increase in Gross Floor Income and a lower cost of funds due to the

impact of ASC 815 (discussed below). Partially offsetting these improvements to the student loan spread was a

18 basis point widening of the CP/LIBOR spread, higher credit spreads on the Company’s ABS debt issued in

2008 and 2009 due to the current credit environment and lower spreads earned on FFELP loans funded

through the ED Participation Program.

The student loan spread for 2008, before 2008 Asset-Backed Financing Facilities fees, decreased 16 basis

points from 2007. The decrease was primarily due to an increase in our cost of funds, which is the result of

both an increase in the credit spread on the Company’s debt issued in the previous year as a result of the

credit environment as well as due to the impact of ASC 815 (discussed below). This was partially offset by an

increase in Floor Income due to a decrease in interest rates in 2008 compared to 2007.

The cost of funds for on-balance sheet student loans excludes the impact of basis swaps that are intended

to economically hedge the re-pricing and basis mismatch between our funding and student loan asset indices,

but do not receive hedge accounting treatment under ASC 815. We use basis swaps to manage the basis risk

associated with our interest rate sensitive assets and liabilities. These swaps generally do not qualify as

accounting hedges and, as a result, are required to be accounted for in the “gains (losses) on derivatives and

hedging activities, net” line on the income statement, as opposed to being accounted for in interest expense.

As a result, these basis swaps are not considered in the calculation of the cost of funds in the table above.

Therefore, in times of volatile movements of interest rates like those experienced in 2008 and 2009, the

student loan spread can be volatile. See the “ ‘Core Earnings’ Net Interest Margin” table below, which

reflects these basis swaps in interest expense and demonstrates the economic hedge effectiveness of these basis

swaps.

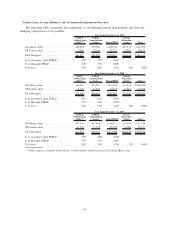

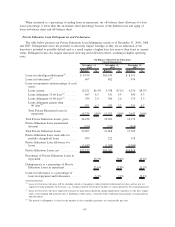

Other Asset Spread — On-Balance Sheet

The other asset spread is generated from cash and investments (both restricted and unrestricted) primarily

in our liquidity portfolio and other loans. The Company invests its liquidity portfolio primarily in short-term

securities with maturities of one week or less in order to manage counterparty credit risk and maintain

available cash balances. The other asset spread decreased 169 basis points from 2008 to 2009, and decreased

11 basis points from 2007 to 2008. Changes in the other asset spread primarily relate to differences in the

index basis and reset frequency between the asset indices and funding indices. A portion of this risk is hedged

with derivatives that do not receive hedge accounting treatment under ASC 815 and will impact the other asset

spread in a similar fashion as the impact to the on-balance sheet student loan spread as discussed above. In

volatile interest rate environments, these spreads may move significantly from period to period and differ from

the “Core Earnings” basis other asset spread discussed below.

57