Sallie Mae 2009 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

6. Goodwill and Acquired Intangible Assets (Continued)

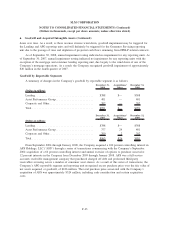

additional cash flows for the Lending reporting unit but no material change in cash flows for the APG or

Guarantor Servicing reporting units.

Under the Company’s guidance, the appraisal firm developed both an asset rate of return and an equity

rate of return (or discount rate) for each reporting unit incorporating such factors as a risk free rate, a market

rate of return, a measure of volatility (Beta) and a company specific and capital markets risk premium, as

appropriate, to adjust for volatility and uncertainty in the economy and to capture specific risk related to the

respective reporting units. The Company considered whether an asset sale or an equity sale would be the most

likely sale structure for each reporting unit and valued each reporting unit based on the more likely

hypothetical scenario. Resulting discount rates and growth rates used as of September 30, 2009, for the

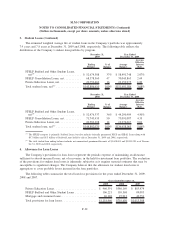

Lending, APG, Guarantor Servicing, and Upromise reporting units were:

Discount Rate Growth Rate

Lending

(1)

.............................................. 11% 3%

APG

(2)

................................................. 10% 4%

Guarantor Servicing

(2)

..................................... 10% 0%

Upromise

(2)

............................................. 15% 4%

(1)

Assumes an equity sale; therefore, the discount rate is used to value the entire reporting unit.

(2)

Assumes an asset sale; therefore, the discount rate is used to value the assets of the reporting unit.

The discount rates reflect market based estimates of capital costs and are adjusted for management’s

assessment of a market participant’s view with respect to execution, concentration and other risks associated

with the projected cash flows of individual reporting units. Accordingly, these discount rates are reflective of

the long standing contractual relationships associated with these cash flows as well as the wind down nature

of the cash flows for certain components of the Lending and APG reporting units and the Guarantor Servicing

reporting unit as a whole. Management reviewed and approved these discount rates, including the factors

incorporated to develop the discount rates for each reporting unit. For the valuation of the Lending reporting

unit, which assumed an equity sale, the discount rate was applied to the reporting unit’s projected net cash

flows and the residual or terminal value yielding the fair value of equity for the reporting unit. For valuations

assuming an asset sale, the discount rates applicable to the individual reporting units were applied to the

respective reporting units’ projected asset cash flows and residual or terminal values, as applicable, yielding

the fair value of the assets for the respective reporting units. The estimated proceeds from the hypothetical

asset sale were then used to payoff any liabilities of the reporting unit with the remaining cash equaling the

fair value of the reporting unit’s equity.

The guideline company or market approach, as well as the publicly traded stock approach, were also

considered for the Company’s reporting units, as applicable. The market approach generally measures the

value of a reporting unit as compared to recent sales or offerings of comparable companies. The secondary

market approach indicates value based on multiples calculated using the market value of minority interests in

publicly traded comparable companies or guideline companies. Whether analyzing comparable transactions or

the market value of minority interests in publicly traded guideline companies, consideration is given to the

line of business and the operating performance of the comparable companies versus the reporting unit being

tested. Given current market conditions, the lack of recent sales or offerings in the market and the low

correlation between the operations of identified guideline companies to the Company’s reporting units, less

emphasis was placed on the market approach for the APG, Guarantor Servicing and Upromise reporting units.

The Company acknowledges that its stock price (as well as that of its peers) is a consideration in

determining the value of its reporting units and the Company as a whole. However, management believes the

F-41

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)