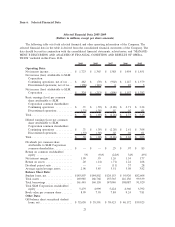

Sallie Mae 2009 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

See the “LENDING BUSINESS SEGMENT,” “APG BUSINESS SEGMENT” and “CORPORATE AND

OTHER BUSINESS SEGMENT” discussions for greater detail on the nature and extent of our income and

operations related to these areas.

On January 14, 2010, President Obama announced his intention to propose a Financial Crisis Responsi-

bility Fee that would require certain institutions which own insured depository institutions to pay a tax equal

to 15 basis points (0.15 percent) of certain liabilities. This tax is intended to raise up to $117 billion to

reimburse the federal government for the projected cost of the Troubled Asset Relief Program (“TARP”).

Congress has not yet taken up any legislation and no legislative language has been proposed. As such, the

Company cannot say whether it will be subject to this new tax, if enacted. Additionally, since the Company

did not receive any money from the TARP, the Company’s position is that the Company should not be subject

to the tax. Moreover, the majority of loans held by the Company were originated under the FFELP, with

program terms and interest rates determined by Congress, and subjecting those assets to this new tax would

not be consistent with the behavior the tax is intended to penalize.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Management’s Discussion and Analysis of Financial Condition and Results of Operations addresses our

consolidated financial statements, which have been prepared in accordance with generally accepted accounting

principles in the United States of America (“GAAP”). Note 2 to the consolidated financial statements,

“Significant Accounting Policies,” includes a summary of the significant accounting policies and methods used

in the preparation of our consolidated financial statements. The preparation of these financial statements

requires management to make estimates and assumptions that affect the reported amounts of assets and

liabilities and the reported amounts of income and expenses during the reporting periods. Actual results may

differ from these estimates under varying assumptions or conditions. On a quarterly basis, management

evaluates its estimates, particularly those that include the most difficult, subjective or complex judgments and

are often about matters that are inherently uncertain. The most significant judgments, estimates and assump-

tions relate to the following critical accounting policies that are discussed in more detail below.

Allowance for Loan Losses

We maintain an allowance for loan losses at an amount sufficient to absorb losses incurred in our FFELP

loan and Private Education Loan portfolios at the reporting date based on a projection of estimated probable

credit losses incurred in the portfolio. We analyze those portfolios to determine the effects that the various

stages of delinquency and forbearance have on borrower default behavior and ultimate charge-off. We estimate

the allowance for loan losses for our loan portfolio using a migration analysis of delinquent and current

accounts. A migration analysis is a technique used to estimate the likelihood that a loan receivable may

progress through the various delinquency stages and ultimately charge off and is a widely used reserving

methodology in the consumer finance industry. We also use the migration analysis to estimate the amount of

uncollectible accrued interest on Private Education Loans and reserve for that amount against current period

interest income. The evaluation of the allowance for loan losses is inherently subjective, as it requires material

estimates that may be susceptible to significant changes. Our default estimates are based on a loss

confirmation period of generally two years (i.e., our allowance for loan loss covers the next two years of

expected losses). The two-year estimate of the allowance for loan losses is subject to a number of assumptions.

If actual future performance in delinquency, charge-offs and recoveries are significantly different than

estimated, this could materially affect our estimate of the allowance for loan losses and the related provision

for loan losses on our income statement. We believe that the Private Education Loan and FFELP allowance for

loan losses are appropriate to cover probable losses incurred in the student loan portfolio.

When calculating the allowance for loan losses on Private Education Loans, we divide the portfolio into

categories of similar risk characteristics based on loan program type, loan status (in-school, grace, forbearance,

repayment and delinquency), underwriting criteria (FICO scores), and existence or absence of a cosigner. As noted

above, we use historical experience of borrower default behavior and charge-offs to estimate the probable credit

losses incurred in the loan portfolio at the reporting date. Also, we use historical borrower payment behavior to

estimate the timing and amount of future recoveries on charged-off loans. We then apply the default and collection

26