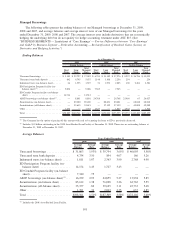

Sallie Mae 2009 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2009 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

attention and resources from management and designated for the appropriate management committee and/or

committee of the Board for oversight.

Management risk committees and their primary responsibility are as follows:

Consumer Products and Services Assessment Committee — reviews new products and services,

including operational implications;

Credit Committee: establishes, approves and enforces credit lending policies and practices;

Compliance Committee: advises on and reviews regulatory compliance;

Asset/Liability Committee: manages market, interest rate and balance sheet risk, and investments;

Disclosure Committee: manages risk of compliance with SEC disclosure obligations;

Critical Accounting Assumptions Committee: reviews key critical accounting assumptions, judgments

and estimates and manages risk of compliance with financial reporting requirements;

Information Technology Steering Committee: manages security and confidentiality of information

and effectiveness of IT infrastructure;

Business Continuity Steering Committee: manages risk of emergency loss of IT and other infrastruc-

ture resources;

Allowance for Loan Loss Steering Committee — approves the loan loss reserve based upon review

of assumptions and estimates involved in the calculation;

Internal Controls Excellence Steering Committee: monitors internal controls and compliance with the

Sarbanes-Oxley Act; and

Regulation Dissemination and Implementation Committee: monitors and disseminates changes in

regulations affecting the business lines and advises on implementation of changes where applicable.

The formal risk management process represents only one portion of our overall risk management

framework. Our Code of Business Conduct and the on-going training our employees receive in many

compliance areas provide a framework for employees to conduct themselves with the highest integrity. We

instill a risk-conscious culture through communications, training, policies and procedures and organizational

roles and responsibilities. We have strengthened the linkage between the management performance process

and individual compensation to encourage employees to work toward corporate-wide compliance goals.

Liquidity Risk Management

Liquidity is the ongoing ability to accommodate liability maturities and deposit withdrawals, fund asset

growth and business operations, and meet contractual obligations at reasonable market rates. Liquidity

management involves forecasting funding requirements and maintaining sufficient capacity to meet the needs

and accommodate fluctuations in asset and liability levels due to changes in our business operations or

unanticipated events. Sources of liquidity include wholesale market-based funding, temporary federal govern-

ment programs and deposits at Sallie Mae Bank.

The Finance Committee of the Board of Directors is responsible for approving the Company’s Asset and

Liability Management Policy. The Finance Committee of the Board and, in some cases, the full Board,

monitor the Company’s liquidity on an ongoing basis. The Corporate Finance Department is responsible for

planning and executing our funding activities and strategy.

In order to ensure adequate liquidity through the full range of potential operating environments and

market conditions, we conduct our liquidity management and business activities in a manner that will preserve

and enhance funding stability, flexibility and diversity. Key components of this operating strategy include

maintaining direct relationships with wholesale market funding providers and maintaining the ability to

liquidate unencumbered assets if necessary. For a further discussion of our liquidity and capital resources and

109