SunTrust 2013 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2013 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

68

settlement contract, GSE owned loans serviced by third party servicers, loans sold to private investors, and future

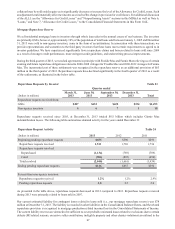

indemnifications.

Various factors could potentially impact the accuracy of the assumptions underlying our mortgage repurchase reserve estimate.

As previously discussed, the level of repurchase requests we receive is dependent upon the actions of third parties and could

differ from the assumptions that we have made. Delinquency levels, delinquency roll rates, and our loss severity assumptions

are all highly dependent upon economic factors including changes in real estate values and unemployment levels which are,

by nature, difficult to predict. Loss severity assumptions could also be negatively impacted by delays in the foreclosure process,

which is a heightened risk in some of the states where our loans sold were originated. Moreover, the 2013 agreements with

Fannie Mae and Freddie Mac settling certain aspects of our repurchase obligations preserve their right to require repurchases

arising from certain types of events, and that preservation of rights can impact our future losses. We understand the FHFA’s

Office of Inspector General has commenced an audit of the FHFA’s oversight of Fannie Mae’s and Freddie Mac’s exercise

of their rights under settlement agreements with banks, including Fannie Mae’s and Freddie Mac’s preserved right to require

repurchases when consumer protection laws have been violated. While the repurchase reserve includes the estimated cost of

settling claims related to required repurchases, our estimate of losses depends on our assumptions regarding GSE and other

counterparty behavior, loan performance, home prices, and other factors. Approximately 16% of the population of total loans

sold between January 1, 2006 and December 31, 2008 were sold to non-agency investors, some in the form of securitizations.

Due to the nature of these structures and the indirect ownership interests, the potential exists that investors, over time, will

become more successful in forcing additional repurchase demands. While we have used the best information available in

estimating the mortgage repurchase reserve liability, these and other factors, along with the discovery of additional information

in the future could result in changes in our assumptions which could materially impact our results of operations.

See "Noninterest Income" in this MD&A and Note 17, “Guarantees - Loan Sales,” to the Consolidated Financial Statements

in this Form 10-K for further discussion.

Legal and Regulatory Matters

We are parties to numerous claims and lawsuits arising in the course of our normal business activities, some of which involve

claims for substantial amounts, and the outcomes of which are not within our complete control or may not be known for

prolonged periods of time. Management is required to assess the probability of loss and amount of such loss, if any, in preparing

our financial statements.

We evaluate the likelihood of a potential loss from legal or regulatory proceedings to which we are a party. We record a liability

for such claims only when a loss is considered probable and the amount can be reasonably estimated. The liability is recorded

in other liabilities in the Consolidated Balance Sheets and related expense is recorded in the applicable category of noninterest

expense, depending on the nature of the legal matter, in the Consolidated Statements of Income. Significant judgment may

be required in the determination of both probability of loss and whether an exposure is reasonably estimable. Our estimates

are subjective based on the status of the legal or regulatory proceedings, the merits of our defenses, and consultation with in-

house and outside legal counsel. In many such proceedings, it is not possible to determine whether a liability has been incurred

or to estimate the ultimate or minimum amount of that liability until the matter is close to resolution. As additional information

becomes available, we reassess the potential liability related to pending claims and may revise our estimates.

Due to the inherent uncertainties of the legal and regulatory processes in the multiple jurisdictions in which we operate, our

estimates may be materially different than the actual outcomes, which could have material effects on our business, financial

condition, and results of operations. See Note 19, “Contingencies,” to the Consolidated Financial Statements in this Form 10-

K for further discussion.

Estimates of Fair Value

Fair value is the price that could be received to sell an asset or paid to transfer a liability in an orderly transaction between

market participants. Certain of our assets and liabilities are measured at fair value on a recurring basis. Examples of recurring

uses of fair value include derivative instruments, AFS and trading securities, certain LHFI and LHFS, certain issuances of

long term debt and brokered CDs, and MSRs. We also measure certain assets at fair value on a non-recurring basis either

when such assets are carried at the LOCOM, to evaluate assets for impairment, or for disclosure purposes. Examples of these

non-recurring uses of fair value include certain LHFS, OREO, goodwill, intangible assets, nonmarketable equity securities,

certain partnership investments, and long-lived assets. Depending on the nature of the asset or liability, we use various valuation

techniques and assumptions when estimating fair value.

The objective of fair value is to use market-based inputs or assumptions, when available, to estimate the price that would be

received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement