SunTrust 2013 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2013 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

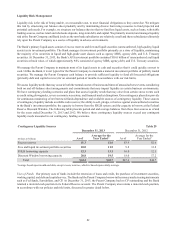

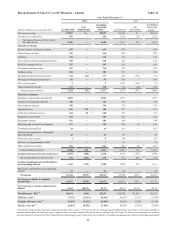

85

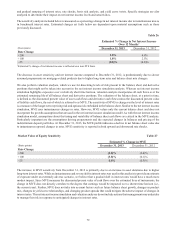

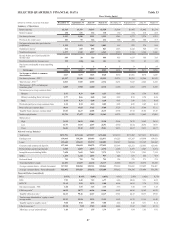

As presented below, we had an aggregate potential obligation of $64.1 billion to our clients in unused lines of credit at

December 31, 2013. Commitments to extend credit are arrangements to lend to clients who have complied with predetermined

contractual obligations. We also had $3.3 billion in letters of credit at December 31, 2013, most of which are standby letters

of credit, which require that we provide funding if certain future events occur. Approximately $1.4 billion of these letters

supported variable rate demand obligations at December 31, 2013. Unused commercial lines of credit have increased since

December 31, 2012, as we continued to provide credit availability to our clients, while mortgage commitments have decreased

significantly due to a decline in IRLC contracts as a result of rising interest rates during the year.

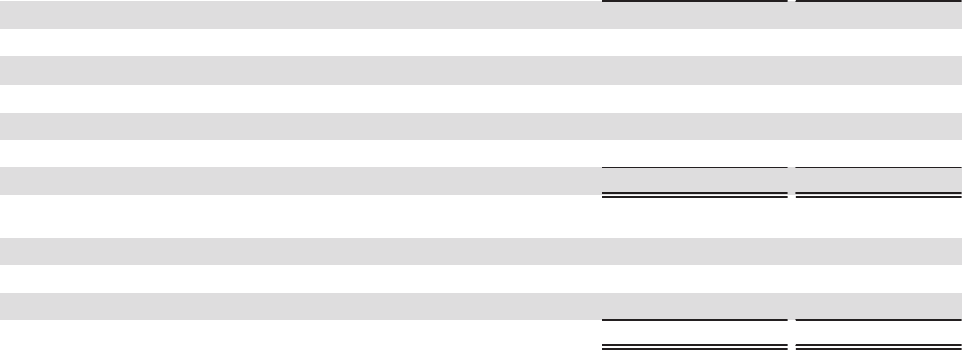

Unfunded Lending Commitments Table 31

(Dollars in millions) December 31, 2013 December 31, 2012

Unused lines of credit:

Commercial $43,444 $36,902

Mortgage commitments 12,722 9,152

Home equity lines 11,157 11,739

CRE 2,078 1,684

Credit card 4,708 4,075

Total unused lines of credit $64,109 $63,552

Letters of credit:

Financial standby $3,256 $3,993

Performance standby 57 49

Commercial 28 56

Total letters of credit $3,341 $4,098

1 Includes IRLC contracts with notional balances of $1.8 billion and $6.8 billion at December 31, 2013 and 2012, respectively.

Other Market Risk

Other sources of market risk include the risk associated with holding residential and commercial mortgage loans prior to

selling them into the secondary market, commitments to clients to make mortgage loans that will be sold to the secondary

market, and our investment in MSRs. We manage the risks associated with the residential and commercial mortgage LHFS

(i.e., the warehouse) and our IRLCs on residential loans intended for sale. The warehouses and IRLCs consist primarily of

fixed and adjustable rate single family residential and CRE loans. The risk associated with the warehouses and IRLCs is the

potential change in interest rates between the time the customer locks the rate on the anticipated loan and the time the loan

is sold on the secondary market, which is typically 60-150 days.

We manage interest rate risk predominantly with interest rate swaps, futures, and forward sale agreements, where the changes

in value of the instruments substantially offset the changes in value of the warehouse and the IRLCs. The IRLCs on residential

mortgage loans intended for sale are classified as derivative financial instruments and are not designated as hedge accounting

relationships.

MSRs are the present value of future net cash flows that are expected to be received from the mortgage servicing portfolio.

The value of MSRs is highly dependent upon the assumed prepayment speed of the mortgage servicing portfolio, which is

driven by the level of certain key interest rates, primarily the 30-year current coupon par mortgage rate. Future expected net

cash flows from servicing a loan in the mortgage servicing portfolio would not be realized if the loan pays off earlier than

anticipated.

MSRs, which are carried at fair value, totaled $1.3 billion and $899 million at December 31, 2013 and 2012, respectively, are

managed within established risk limits, and are monitored as part of various governance processes. We originated MSRs with

fair values at the time of origination of $352 million and $336 million during 2013 and 2012, respectively, and recognized a

mark-to-market increase of $50 million and a decrease of $353 million in the fair value of our MSRs in 2013 and 2012,

respectively. Increases or decreases in fair value include the decay resulting from the realization of expected monthly net

servicing cash flows. We recorded $233 million and $69 million of net losses during 2013 and 2012, respectively, inclusive

of decay and related hedges. The increase in net losses related to MSRs during 2013 compared to 2012 was driven by a decline

in net hedge performance as a result of decreased carry income and an increase in market interest rate volatility, as well as a

modest increase in decay.