SunTrust 2013 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2013 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

Notes to Consolidated Financial Statements, continued

173

connection with these transactions. Under the derivative, the Visa Counterparty is compensated by the Company for any decline

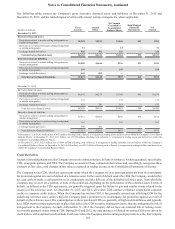

in the conversion factor as a result of the outcome of the Litigation. Conversely, the Company is compensated by the Visa

Counterparty for any increase in the conversion factor. The amount of payments made or received under the derivative is a

function of the 3.2 million shares sold to the Visa Counterparty, the change in conversion rate, and Visa’s share price. The Visa

Counterparty, as a result of its ownership of the Class B shares, is impacted by dilutive adjustments to the conversion factor

of the Class B shares caused by the Litigation losses. The conversion factor at the inception of the derivative in May 2009 was

0.6296 and at December 31, 2013 the conversion factor was 0.4206 due to Visa’s funding of the litigation escrow account since

2009. Decreases in the conversion factor triggered payments by the Company to the Visa Counterparty of $0, $26 million and

$8 million for the years ended December 31, 2013, 2012, and 2011, respectively.

During 2012, the Card Associations and defendants signed a memorandum of understanding to enter into a settlement agreement

to resolve the plaintiffs' claims in the Litigation. Visa's share of the claims represents approximately $4.4 billion, which was

paid from the escrow account into a settlement fund during 2012. During 2013, various members of the putative class elected

to opt out of the settlement. This will result in a proportional decrease in the amount of the settlement. While the estimated

fair value of the derivative liability was immaterial at December 31, 2013 and 2012, the ultimate impact to the Company could

be significantly different if the settlement is not approved and/or based on the ultimate resolution with the plaintiffs that opted

out of the settlement.

Tax Credit Investments Sold

SunTrust Community Capital, one of the Company's subsidiaries, previously obtained state and federal tax credits through the

construction and development of affordable housing properties and continues to obtain state and federal tax credits through

investments in affordable housing developments. SunTrust Community Capital or its subsidiaries are limited and/or general

partners in various partnerships established for the properties. Some of the investments that generate state tax credits may be

sold to outside investors. At December 31, 2013, SunTrust Community Capital has completed six sales containing guarantee

provisions stating that SunTrust Community Capital will make payment to the outside investors if the tax credits become

ineligible. SunTrust Community Capital also guarantees that the general partner under the transaction will perform on the

delivery of the credits. The guarantees are expected to expire within a fifteen year period from inception. At December 31,

2013, the maximum potential amount that SunTrust Community Capital could be obligated to pay under these guarantees is

$37 million; however, SunTrust Community Capital can seek recourse against the general partner. Additionally, SunTrust

Community Capital can seek reimbursement from cash flow and residual values of the underlying affordable housing properties

provided that the properties retain value. At December 31, 2013 and 2012, $1 million and $3 million, respectively, was accrued,

representing the remainder of tax credits to be delivered, and were recorded in other liabilities in the Consolidated Balance

Sheets.

Public Deposits

The Company holds public deposits from various states in which it does business. Individual state laws require banks to

collateralize public deposits, typically as a percentage of their public deposit balance in excess of FDIC insurance and may

also require a cross-guarantee among all banks holding public deposits of the individual state. The amount of collateral required

varies by state and may also vary by institution within each state, depending on the individual state's risk assessment of

depository institutions. Certain of the states in which the Company holds public deposits use a pooled collateral method,

whereby in the event of default of a bank holding public deposits, the collateral of the defaulting bank is liquidated to the extent

necessary to recover the loss of public deposits of the defaulting bank. To the extent the collateral is insufficient, the remaining

public deposit balances of the defaulting bank are recovered through an assessment of the other banks holding public deposits

in that state. The maximum potential amount of future payments the Company could be required to make is dependent on a

variety of factors, including the amount of public funds held by banks in the states in which the Company also holds public

deposits and the amount of collateral coverage associated with any defaulting bank. Individual states appear to be monitoring

this risk relative to the current economic environment and evaluating collateral requirements; therefore, the likelihood that the

Company would have to perform under this guarantee is dependent on whether any banks holding public funds default as well

as the adequacy of collateral coverage.

Other

In the normal course of business, the Company enters into indemnification agreements and provides standard representations

and warranties in connection with numerous transactions. These transactions include those arising from securitization activities,

underwriting agreements, merger and acquisition agreements, swap clearing agreements, loan sales, contractual commitments,

payment processing, sponsorship agreements, and various other business transactions or arrangements. The extent of the

Company's obligations under these indemnification agreements depends upon the occurrence of future events; therefore, the

Company's potential future liability under these arrangements is not determinable.